Notes to the financial statements(Expressed in millions of RMB, unless otherwise stated)63 Risk Management (continued)(1) Credit riskCredit risk managementCredit risk represents the financial loss that arises from the failure of a debtor or counterparty to discharge its contractual obligationsor commitments to the Group.Credit businessThe Risk Management Department, under the supervision of the Chief Risk Officer, is responsible for establishing credit riskmanagement policies and performing credit risk measurement and analysis. The Credit Management Department is responsiblefor monitoring the implementation of credit risk management policies and coordinating credit approval and credit ratings activities.The Credit Management Department works together with the Corporate Banking Department, the SME Business Department, theInstitutional Banking Department, the International Business Department, the Group Clients Department, the Housing Finance &Personal Lending Department, the Credit Card Center, the Special Assets Resolution Department and Legal Affairs Department toimplement credit risk management policies and procedures.With respect to the credit risk management of corporate and institutional business, the Group has sped up the adjustment of itscredit portfolio structure, enhanced post-lending monitoring, and refined the industry-specific guideline and policy baseline for creditapproval. Management also fine-tuned the credit acceptance and exit policies, and optimised its economic capital and credit risk limitmanagement. All these policies have implemented to improve the overall asset quality. The Group manages credit risk throughout theentire credit process including pre-lending evaluations, credit approval and post-lending monitoring. The Group performs pre-lendingevaluations by assessing the entity’s credit ratings based on internal rating criteria and assessing the risk and rewards with respectto the proposed project. Credit approvals are granted by designated Credit Approval Officers. The Group continually monitorsloans, particularly those related to targeted industries, geographical segments, products and clients. Any adverse events that maysignificantly affect a borrower’s repayment ability are reported timely and measures are implemented to prevent and control risks. Thecentralised risk management was also expedited in the cities where the first-tier branches are located, and the Bank will continue toexplore the ways of specifying the operating characteristic for those branches, in addition to develop an intensive management forrisk, reallocation of resource, and improving the quality and efficiency.With respect to the personal credit business, the Group relies on credit assessment of applicants as the basis for loan approval.Customer relationship managers are required to assess the income level, credit history, and repayment ability of the applicant. Thecustomer relationship managers then forward the application and recommendations to the loan-approval departments for consent.The Group monitors borrowers’ repayment ability, the status of collateral and any changes to collateral value. Once a loan becomesoverdue, the Group starts the recovery process according to standard personal loan recovery procedures.To mitigate risks, the Group requests the customers to provide collateral and guarantees where appropriate. A fine managementsystem and operating workflow for collateral was developed, and there is a guideline to specify the suitability of accepting specifictypes of collateral, as well as determining evaluation parameters. Collateral values, structures and legal covenants are regularlyreviewed to ensure that they still serve their intended purposes and conform to market practices.Credit grading classificationThe Group adopts a loan risk classification approach to manage the loan portfolio risk. Loans are generally classified as normal,special mention, substandard, doubtful and loss according to their level of risk. Substandard, doubtful and loss loans are consideredas impaired loans and advances when one or more events demonstrate there is objective evidence of a loss event which triggersimpairment. The allowance for impairment loss on impaired loans and advances is collectively or individually assessed as appropriate.China Construction Bank Corporation annual report <strong>2012</strong>169

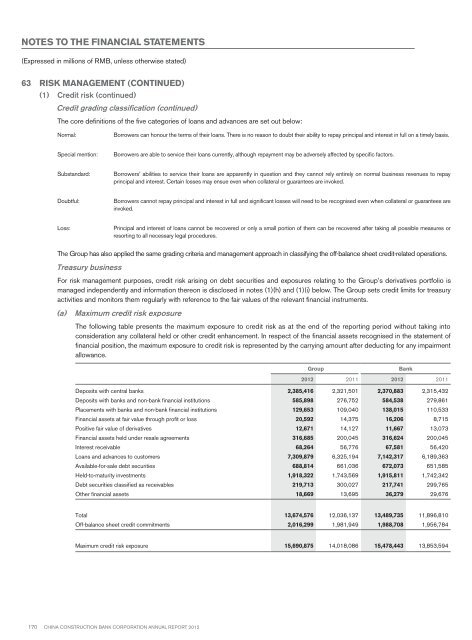

Notes to the financial statements(Expressed in millions of RMB, unless otherwise stated)63 Risk Management (continued)(1) Credit risk (continued)Credit grading classification (continued)The core definitions of the five categories of loans and advances are set out below:Normal:Borrowers can honour the terms of their loans. There is no reason to doubt their ability to repay principal and interest in full on a timely basis.Special mention:Borrowers are able to service their loans currently, although repayment may be adversely affected by specific factors.Substandard:Borrowers’ abilities to service their loans are apparently in question and they cannot rely entirely on normal business revenues to repayprincipal and interest. Certain losses may ensue even when collateral or guarantees are invoked.Doubtful:Borrowers cannot repay principal and interest in full and significant losses will need to be recognised even when collateral or guarantees areinvoked.Loss:Principal and interest of loans cannot be recovered or only a small portion of them can be recovered after taking all possible measures orresorting to all necessary legal procedures.The Group has also applied the same grading criteria and management approach in classifying the off-balance sheet credit-related operations.Treasury businessFor risk management purposes, credit risk arising on debt securities and exposures relating to the Group’s derivatives portfolio ismanaged independently and information thereon is disclosed in notes (1)(h) and (1)(i) below. The Group sets credit limits for treasuryactivities and monitors them regularly with reference to the fair values of the relevant financial instruments.(a)Maximum credit risk exposureThe following table presents the maximum exposure to credit risk as at the end of the reporting period without taking intoconsideration any collateral held or other credit enhancement. In respect of the financial assets recognised in the statement offinancial position, the maximum exposure to credit risk is represented by the carrying amount after deducting for any impairmentallowance.GroupBank<strong>2012</strong> 2011 <strong>2012</strong> 2011Deposits with central banks 2,385,416 2,321,501 2,370,883 2,315,432Deposits with banks and non-bank financial institutions 585,898 276,752 584,538 279,861Placements with banks and non-bank financial institutions 129,653 109,040 138,015 110,533Financial assets at fair value through profit or loss 20,592 14,375 16,206 8,715Positive fair value of derivatives 12,671 14,127 11,667 13,073Financial assets held under resale agreements 316,685 200,045 316,624 200,045Interest receivable 68,264 56,776 67,581 56,420Loans and advances to customers 7,309,879 6,325,194 7,142,317 6,189,363Available-for-sale debt securities 688,814 661,036 672,073 651,585Held-to-maturity investments 1,918,322 1,743,569 1,915,811 1,742,342Debt securities classified as receivables 219,713 300,027 217,741 299,765Other financial assets 18,669 13,695 36,279 29,676Total 13,674,576 12,036,137 13,489,735 11,896,810Off-balance sheet credit commitments 2,016,299 1,981,949 1,988,708 1,956,784Maximum credit risk exposure 15,690,875 14,018,086 15,478,443 13,853,594170 China Construction Bank Corporation annual report <strong>2012</strong>