Solar Energy Perspectives - IEA

Solar Energy Perspectives - IEA

Solar Energy Perspectives - IEA

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Chapter 6: <strong>Solar</strong> photovoltaics<br />

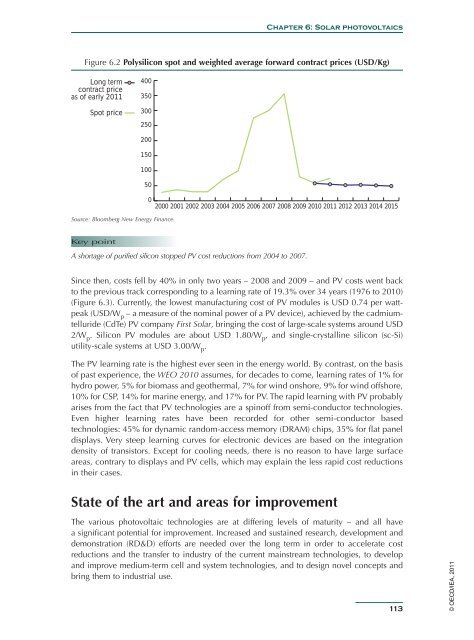

Figure 6.2 Polysilicon spot and weighted average forward contract prices (USD/Kg)<br />

Long term<br />

contract price<br />

as of early 2011<br />

Spot price<br />

400<br />

350<br />

300<br />

250<br />

200<br />

150<br />

100<br />

50<br />

0<br />

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015<br />

Source: Bloomberg New <strong>Energy</strong> Finance.<br />

Key point<br />

Figure 6.2<br />

A shortage of purified silicon stopped PV cost reductions from 2004 to 2007.<br />

Since then, costs fell by 40% in only two years – 2008 and 2009 – and PV costs went back<br />

to the previous track corresponding to a learning rate of 19.3% over 34 years (1976 to 2010)<br />

(Figure 6.3). Currently, the lowest manufacturing cost of PV modules is USD 0.74 per wattpeak<br />

(USD/W p – a measure of the nominal power of a PV device), achieved by the cadmiumtelluride<br />

(CdTe) PV company First <strong>Solar</strong>, bringing the cost of large-scale systems around USD<br />

2/W p . Silicon PV modules are about USD 1.80/W p , and single-crystalline silicon (sc-Si)<br />

utility-scale systems at USD 3.00/W p .<br />

The PV learning rate is the highest ever seen in the energy world. By contrast, on the basis<br />

of past experience, the WEO 2010 assumes, for decades to come, learning rates of 1% for<br />

hydro power, 5% for biomass and geothermal, 7% for wind onshore, 9% for wind offshore,<br />

10% for CSP, 14% for marine energy, and 17% for PV. The rapid learning with PV probably<br />

arises from the fact that PV technologies are a spinoff from semi-conductor technologies.<br />

Even higher learning rates have been recorded for other semi-conductor based<br />

technologies: 45% for dynamic random-access memory (DRAM) chips, 35% for flat panel<br />

displays. Very steep learning curves for electronic devices are based on the integration<br />

density of transistors. Except for cooling needs, there is no reason to have large surface<br />

areas, contrary to displays and PV cells, which may explain the less rapid cost reductions<br />

in their cases.<br />

State of the art and areas for improvement<br />

The various photovoltaic technologies are at differing levels of maturity – and all have<br />

a significant potential for improvement. Increased and sustained research, development and<br />

demonstration (RD&D) efforts are needed over the long term in order to accelerate cost<br />

reductions and the transfer to industry of the current mainstream technologies, to develop<br />

and improve medium-term cell and system technologies, and to design novel concepts and<br />

bring them to industrial use.<br />

113<br />

© OECD/<strong>IEA</strong>, 2011