Solar Energy Perspectives - IEA

Solar Energy Perspectives - IEA

Solar Energy Perspectives - IEA

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Chapter 3: <strong>Solar</strong> electricity<br />

peak times is always costlier than base load electricity generation. In sunny and warm<br />

countries, the sunniest hours of the day usually correspond to the peak or mid-peak demand,<br />

but supply may or may not be priced high enough to reflect the full costs.<br />

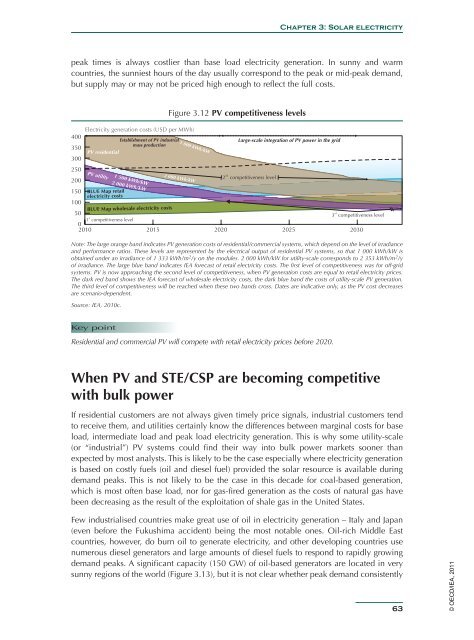

Electricity generation costs (USD per MWh)<br />

400<br />

Establishment of PV industrial<br />

mass production<br />

350<br />

PV residential<br />

300<br />

250<br />

200<br />

150<br />

100<br />

PV utility 2 000 kWh/kW<br />

BLUE Map retail<br />

electricity costs<br />

1 500 kWh/kW<br />

BLUE Map wholesale electricity costs<br />

50<br />

st<br />

1 competitiveness level<br />

0<br />

2010 2015 2020<br />

Figure 3.12 PV competitiveness levels<br />

1 000 kWh/kW<br />

2 000 kWh/kW<br />

Large-scale integration of PV power in the grid<br />

nd<br />

2 competitiveness level<br />

rd<br />

3 competitiveness level<br />

2025 2030<br />

Note: The large orange band indicates PV generation costs of residential/commercial systems, which depend on the level of irradiance<br />

and performance ratios. These levels are represented by the electrical output of residential PV systems, so that 1 000 kWh/kW is<br />

obtained under an irradiance of 1 333 kWh/m 2 /y on the modules. 2 000 kWh/kW for utility-scale corresponds to 2 353 kWh/m 2 /y<br />

of irradiance. The large blue band indicates <strong>IEA</strong> forecast of retail electricity costs. The first level of competitiveness was for off-grid<br />

systems. PV is now approaching the second level of competitiveness, when PV generation costs are equal to retail electricity prices.<br />

The dark red band shows the <strong>IEA</strong> forecast of wholesale electricity costs, the dark blue band the costs of utility-scale PV generation.<br />

The third level of competitiveness will be reached when these two bands cross. Dates are indicative only, as the PV cost decreases<br />

are scenario-dependent.<br />

Source: <strong>IEA</strong>, 2010c.<br />

Key point<br />

Residential and commercial PV will compete with retail electricity prices before 2020.<br />

When PV and STE/CSP are becoming competitive<br />

with bulk power<br />

If residential customers are not always given timely price signals, industrial customers tend<br />

to receive them, and utilities certainly know the differences between marginal costs for base<br />

load, intermediate load and peak load electricity generation. This is why some utility-scale<br />

(or “industrial”) PV systems could find their way into bulk power markets sooner than<br />

expected by most analysts. This is likely to be the case especially where electricity generation<br />

is based on costly fuels (oil and diesel fuel) provided the solar resource is available during<br />

demand peaks. This is not likely to be the case in this decade for coal-based generation,<br />

which is most often base load, nor for gas-fired generation as the costs of natural gas have<br />

been decreasing as the result of the exploitation of shale gas in the United States.<br />

Few industrialised countries make great use of oil in electricity generation – Italy and Japan<br />

(even before the Fukushima accident) being the most notable ones. Oil-rich Middle East<br />

countries, however, do burn oil to generate electricity, and other developing countries use<br />

numerous diesel generators and large amounts of diesel fuels to respond to rapidly growing<br />

demand peaks. A significant capacity (150 GW) of oil-based generators are located in very<br />

sunny regions of the world (Figure 3.13), but it is not clear whether peak demand consistently<br />

63<br />

© OECD/<strong>IEA</strong>, 2011