Solar Energy Perspectives - IEA

Solar Energy Perspectives - IEA

Solar Energy Perspectives - IEA

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Chapter 10: Policies<br />

distinguish perceptions from realities. The gap between the true cost of support (the subsidy<br />

part) and the amount of investment increases at each doubling. The cost of PV support will<br />

peak and then decrease. It disappears after the break-even point is reached. A similar<br />

reasoning would apply to solar thermal electricity.<br />

Ignoring discount (interest) rates, the calculation does not depend on any particular agenda.<br />

Speeding or slowing the diffusion of PV does not modify the bill. Optimising the deployment<br />

agenda would require introducing discounting and selecting hypotheses on the likely<br />

evolution of market electricity prices, competing technologies and environmental benefits,<br />

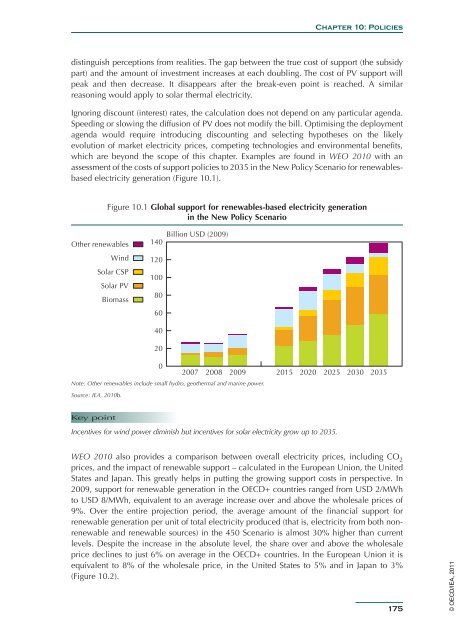

which are beyond the scope of this chapter. Examples are found in WEO 2010 with an<br />

assessment of the costs of support policies to 2035 in the New Policy Scenario for renewablesbased<br />

electricity generation (Figure 10.1).<br />

Figure 10.1 Global support for renewables-based electricity generation<br />

in the New Policy Scenario<br />

Other renewables<br />

Wind<br />

<strong>Solar</strong> CSP<br />

<strong>Solar</strong> PV<br />

Biomass<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

Billion USD (2009)<br />

0<br />

2007 2008 2009 2015 2020 2025 2030 2035<br />

Note: Other renewables include small hydro, geothermal and marine power.<br />

Source: <strong>IEA</strong>, 2010b.<br />

Key point<br />

Incentives for wind power diminish but incentives for solar electricity grow up to 2035.<br />

WEO 2010 also provides a comparison between overall electricity prices, including CO 2<br />

prices, and the impact of renewable support – calculated in the European Union, the United<br />

States and Japan. This greatly helps in putting the growing support costs in perspective. In<br />

2009, support for renewable generation in the OECD+ countries ranged from USD 2/MWh<br />

to USD 8/MWh, equivalent to an average increase over and above the wholesale prices of<br />

9%. Over the entire projection period, the average amount of the financial support for<br />

renewable generation per unit of total electricity produced (that is, electricity from both nonrenewable<br />

and renewable sources) in the 450 Scenario is almost 30% higher than current<br />

levels. Despite the increase in the absolute level, the share over and above the wholesale<br />

price declines to just 6% on average in the OECD+ countries. In the European Union it is<br />

equivalent to 8% of the wholesale price, in the United States to 5% and in Japan to 3%<br />

(Figure 10.2).<br />

175<br />

© OECD/<strong>IEA</strong>, 2011