- Page 1 and 2:

Renewable Energy Renewable TECHNOLO

- Page 3 and 4:

Renewable Energy Technologies Solar

- Page 5 and 6:

INTERNATIONAL ENERGY AGENCY The Int

- Page 7 and 8:

Foreword Foreword Solar energy tech

- Page 9 and 10:

Acknowledgements Acknowledgements T

- Page 11 and 12:

Table of contents Table of Contents

- Page 13 and 14:

Table of contents Chapter 7 Solar h

- Page 15 and 16:

Table of contents Chapter 3 Chapter

- Page 17 and 18:

Table of contents Chapter 4 Figure

- Page 19 and 20:

Table of contents Figure 10.4 • N

- Page 21 and 22:

Executive Summary Executive Summary

- Page 23 and 24:

Executive Summary A possible vision

- Page 25 and 26:

Chapter 1: Rationale for harnessing

- Page 27 and 28:

Chapter 1: Rationale for harnessing

- Page 29 and 30:

Chapter 1: Rationale for harnessing

- Page 31 and 32:

PART A MARKETS AND OUTLOOK Chapter

- Page 33 and 34:

Chapter 2: The solar resource and i

- Page 35 and 36:

Chapter 2: The solar resource and i

- Page 37 and 38:

Chapter 2: The solar resource and i

- Page 39 and 40:

Chapter 2: The solar resource and i

- Page 41 and 42:

Chapter 2: The solar resource and i

- Page 43 and 44:

Chapter 2: The solar resource and i

- Page 45 and 46:

Chapter 2: The solar resource and i

- Page 47 and 48:

Chapter 2: The solar resource and i

- Page 49 and 50:

Chapter 3: Solar electricity Chapte

- Page 51 and 52:

Chapter 3: Solar electricity Versat

- Page 53 and 54:

Chapter 3: Solar electricity Figure

- Page 55 and 56:

Chapter 3: Solar electricity Figure

- Page 57 and 58:

Chapter 3: Solar electricity to a t

- Page 59 and 60:

Chapter 3: Solar electricity New in

- Page 61 and 62:

Chapter 3: Solar electricity Variou

- Page 63 and 64:

Chapter 3: Solar electricity as fro

- Page 65 and 66:

Chapter 3: Solar electricity peak t

- Page 67 and 68:

Chapter 3: Solar electricity Kenya

- Page 69 and 70:

Chapter 3: Solar electricity • Ad

- Page 71 and 72:

Chapter 4: Buildings Chapter 4 Buil

- Page 73 and 74:

Chapter 4: Buildings South Africa,

- Page 75 and 76:

Chapter 4: Buildings Figure 4.3 Bui

- Page 77 and 78:

Chapter 4: Buildings Défense near

- Page 79 and 80:

Chapter 4: Buildings larger the col

- Page 81 and 82:

Chapter 4: Buildings Pumps variant,

- Page 83 and 84:

Chapter 4: Buildings radiators or h

- Page 85 and 86:

Chapter 4: Buildings Most widesprea

- Page 87 and 88:

Chapter 4: Buildings Photo 4.5 Mans

- Page 89 and 90:

Chapter 4: Buildings the overall po

- Page 91 and 92:

Chapter 4: Buildings area is limite

- Page 93 and 94:

Chapter 4: Buildings Figure 4.11 An

- Page 95 and 96:

Chapter 5: Industry and transport C

- Page 97 and 98:

Chapter 5: Industry and transport c

- Page 99 and 100:

Chapter 5: Industry and transport i

- Page 101 and 102:

Chapter 5: Industry and transport a

- Page 103 and 104:

Chapter 5: Industry and transport i

- Page 105 and 106:

Chapter 5: Industry and transport T

- Page 107 and 108:

Chapter 5: Industry and transport h

- Page 109 and 110:

Chapter 5: Industry and transport t

- Page 111 and 112:

PART B TECHNOLOGIES Chapter 6 Solar

- Page 113 and 114:

Chapter 6: Solar photovoltaics Chap

- Page 115 and 116:

Chapter 6: Solar photovoltaics Figu

- Page 117 and 118:

Chapter 6: Solar photovoltaics of t

- Page 119 and 120:

Chapter 6: Solar photovoltaics or a

- Page 121 and 122:

Chapter 6: Solar photovoltaics Anot

- Page 123 and 124:

Chapter 6: Solar photovoltaics sout

- Page 125 and 126:

Chapter 7: Solar heat Chapter 7 Sol

- Page 127 and 128:

Chapter 7: Solar heat incoming radi

- Page 129 and 130:

Chapter 7: Solar heat Evacuated tub

- Page 131 and 132:

Chapter 7: Solar heat Photo 7.2 Che

- Page 133 and 134:

Chapter 7: Solar heat with the temp

- Page 135 and 136: Chapter 7: Solar heat Photo 7.6 Pos

- Page 137 and 138: Chapter 7: Solar heat Figure 7.8 Sc

- Page 139 and 140: Chapter 7: Solar heat Figure 7.10 B

- Page 141 and 142: Chapter 7: Solar heat inert materia

- Page 143 and 144: Chapter 8: Solar thermal electricit

- Page 145 and 146: Chapter 8: Solar thermal electricit

- Page 147 and 148: Chapter 8: Solar thermal electricit

- Page 149 and 150: Chapter 8: Solar thermal electricit

- Page 151 and 152: Chapter 8: Solar thermal electricit

- Page 153 and 154: Chapter 8: Solar thermal electricit

- Page 155 and 156: Chapter 8: Solar thermal electricit

- Page 157 and 158: Chapter 8: Solar thermal electricit

- Page 159 and 160: Chapter 8: Solar thermal electricit

- Page 161 and 162: Chapter 8: Solar thermal electricit

- Page 163 and 164: Chapter 9: Solar fuels Chapter 9 So

- Page 165 and 166: Chapter 9: Solar fuels “Solar fue

- Page 167 and 168: Chapter 9: Solar fuels in line-focu

- Page 169 and 170: Chapter 9: Solar fuels back to wate

- Page 171 and 172: Chapter 9: Solar fuels Solar gasifi

- Page 173 and 174: PART C THE WAY FORWARD Chapter 10 P

- Page 175 and 176: Chapter 10: Policies Chapter 10 Pol

- Page 177 and 178: Chapter 10: Policies distinguish pe

- Page 179 and 180: Chapter 10: Policies Photo 10.1 Chi

- Page 181 and 182: Chapter 10: Policies In Morocco, se

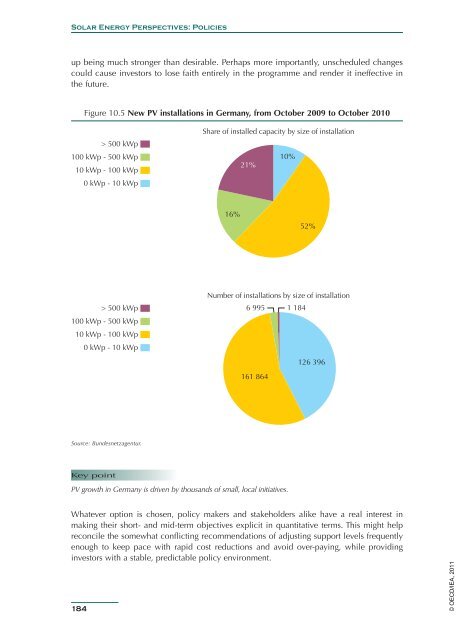

- Page 183 and 184: Chapter 10: Policies and linked to

- Page 185: Chapter 10: Policies ambition of th

- Page 189 and 190: Chapter 10: Policies and can hardly

- Page 191 and 192: Chapter 10: Policies fossil-fuel pl

- Page 193 and 194: Chapter 10: Policies It would make

- Page 195 and 196: Chapter 10: Policies In the retail

- Page 197 and 198: Chapter 11: Testing the limits Chap

- Page 199 and 200: Chapter 11: Testing the limits grow

- Page 201 and 202: Chapter 11: Testing the limits betw

- Page 203 and 204: Chapter 11: Testing the limits Figu

- Page 205 and 206: Chapter 11: Testing the limits The

- Page 207 and 208: Chapter 11: Testing the limits esti

- Page 209 and 210: Chapter 11: Testing the limits Phot

- Page 211 and 212: Water availability is unlikely to b

- Page 213 and 214: Chapter 11: Testing the limits 10 0

- Page 215 and 216: Chapter 11: Testing the limits tran

- Page 217 and 218: Chapter 12: Conclusions and recomme

- Page 219 and 220: Chapter 12: Conclusions and recomme

- Page 221 and 222: Annex A Annex A Definitions, abbrev

- Page 223 and 224: Annex A REC RPS SACP sc-Si SEI SEII

- Page 225 and 226: Annex B Annex B References A.T. Kea

- Page 227 and 228: Annex B Greenpeace International, S

- Page 229 and 230: Annex B Malbranche, Ph. et C. Phili

- Page 233: IEA Publications, 9, rue de la Féd