Rapid Assessment for Resilient Recovery and ... - GFDRR

Rapid Assessment for Resilient Recovery and ... - GFDRR

Rapid Assessment for Resilient Recovery and ... - GFDRR

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

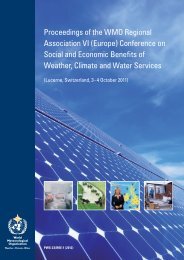

Government<br />

Measure<br />

Loan guarantee<br />

<strong>for</strong> private bank<br />

loans to SMEs<br />

impacted by the<br />

floods<br />

Soft SME loans<br />

<strong>for</strong> flood victims,<br />

offered via<br />

commercial banks<br />

Ability of all banks<br />

to restructure<br />

loans to flood<br />

victims, <strong>and</strong><br />

rapidly re-classify<br />

as current<br />

Decrease in<br />

maximum loan to<br />

value postponed<br />

Minimum credit<br />

card payments<br />

waived<br />

Fees waived on<br />

inter-provincial<br />

ATM transactions<br />

Status<br />

Up to THB 100 billion in new commercial bank loans to<br />

flood-impacted SMEs will be guaranteed by the Thai Credit<br />

Guarantee Corporation (<strong>for</strong>merly SBCGC). These loans have<br />

an interest rate cap of 3 percent <strong>for</strong> the first three years. NPLs<br />

on these loans do not need to be provisioned <strong>for</strong> the guaranteed<br />

part (proportion guaranteed increased gradually, 7 percent by<br />

end of year 1 to 30 percent by year seven, maximum duration of<br />

the guarantee). The guarantee is free <strong>for</strong> the first three years –<br />

but the government will reimburse TCGC <strong>for</strong> the lost fees (of<br />

1.75 percent) <strong>for</strong> those three years. The maximum cost to the<br />

TCGC is reportedly THB 23 billion.<br />

THB 20 billion being made available from GSB to commercial<br />

banks <strong>for</strong> loans to SMEs impacted by the floods. Cost of funds<br />

0.01 percent, but must be matched 50:50 with private bank’s<br />

funds (i.e. total of 40 billion in new loans). Three percent interest<br />

cap <strong>for</strong> first three years of the loan. NPLs must be provisioned<br />

<strong>for</strong> normally. 66<br />

All banks may restructure loans to viable, flood-impacted<br />

borrowers. These restructured borrowers can be taken off the<br />

NPL list after merely one payment under the new schedule, as<br />

opposed to three payments previously. Unclear if there are<br />

tenors limits. Possible cost, if all the 0.5% of total loan portfolio<br />

loses six months of 7% interest rate, would be THB 1.3 billion,<br />

borne by the private banks.<br />

The BOT has postponed a planned measure to reduce the<br />

maximum loan to value in effect <strong>for</strong> mortgages. Unclear what<br />

the impact will be.<br />

The usual minimum payment of 10% of credit card balances<br />

has temporarily been waived, in order to help the cash flow of<br />

flood victims. This measure expires in June 2012.<br />

Banks were told to waive their fees on inter-provincial ATM<br />

transactions, but only <strong>for</strong> the period from November 4–30, 2011.<br />

Unclear what the cost to the banks of this measure will be.<br />

Details<br />

Approved by<br />

Cabinet<br />

Approved by<br />

Cabinet<br />

Already put in<br />

place by BOT<br />

Already put in<br />

place by BOT<br />

Measure in<br />

place<br />

Measure in<br />

place<br />

Insurance Sector<br />

The insurance sector will have financing needs to return to their pre-flood position. As<br />

noted in the previous section, losses to the insurance sector are estimated to be around<br />

THB 9 billion, after reimbursement from re-insurance companies, <strong>and</strong> assuming that the<br />

OIC is correct when stating that around 95 percent of claims <strong>for</strong> these floods were reinsured<br />

abroad.<br />

Given the size <strong>and</strong> scope of this catastrophic event <strong>and</strong> the number of policyholders affected,<br />

the loss adjustment <strong>and</strong> the claims h<strong>and</strong>ling will require a large number of loss<br />

adjusters <strong>and</strong> insurance experts, beyond the apparent capacity of the domestic insurance<br />

market. Japanese reinsurers, who reinsure many of the firms located in the industrial<br />

estates, have already sent Japanese loss assessors. In addition, it is understood that the<br />

domestic insurance companies have agreed to conduct joint loss assessment; a loss assessor<br />

sent in a given area will assess the damage of all insured properties located in this<br />

area on behalf of all the insurance companies.<br />

66 There was a report that soft loans to SMEs are hard to obtain, due to too many requirements, including in terms of<br />

collateral – as per “Red Tape Cut Urged <strong>for</strong> <strong>Recovery</strong>”, Bangkok Post, October 27, 2011.<br />

68 THAI FLOOD 2011 RAPID ASSESSMENT FOR RESILIENT RECOVERY AND RECONSTRUCTION PLANNING