Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Tokyo Electron Ltd<br />

Technology Hardware<br />

o AMAT and LAM are also aiming to gain market share: AMAT is aiming to<br />

gain a 2-4% WFE share by 2016, and LAM is looking to gain a 3-5% share<br />

in the etching market and a 5-10% share in the cleaning market. In our view,<br />

TEL is in a weaker position compared with AMAT and LAM in terms of<br />

gaining share, as it does not have an established market position or<br />

experience in these growing markets.<br />

• Little upside from operating leverage and yen depreciation: TEL’s margin<br />

may improve due to cost savings, but we believe the margin is unlikely to show<br />

significant improvement without top-line growth. We estimate that the gross<br />

margin will stay at the 33% level (34% in 2007) after cost savings are taken into<br />

account. We estimate the operating margin will be 9% in 2015 (compared with<br />

19% in 2007), assuming that the ¥10bn saving planned for 2013 happens each<br />

year thereafter.<br />

• Yen depreciation has had little impact: In our opinion, the yen depreciation<br />

has had little impact on TEL from both an operational and competitiveness<br />

perspective, as: 1) its operations are not heavily exposed to FX movements in<br />

terms of yen contract prices and its manufacturing plants are located in Japan,<br />

meaning that the effect on its operations/cost base is limited; 2) we believe<br />

chip-makers care more about tool performance, reliability and supporting<br />

services than price; and 3) Japan-based Hitachi and Dainippon have the same<br />

FX advantage.<br />

• The FPD/PV segment remain a profit drag: In our opinion, the FPD/PV<br />

segment was always been a profit-dilutive segment for TEL. Between 2004 and<br />

2012, the segment’s margin was 10% at peak, which is lower than the SPE<br />

margin (which averaged 12.5% in 2004-2012). We estimate the segment will be<br />

loss-making in 2013, 2014 and 2015 due to the weak TV and solar markets.<br />

Management is targeting a profit in the solar business in two years’ time, but<br />

expects it to remain sluggish in 2013 and 2014. A weak performance may trigger<br />

impairments on the ¥22bn goodwill related to the Oerlikon Solar acquisition in<br />

2012.<br />

• Valuation: Our price target of ¥4,331 implies an EV/sales of 0.9x, which is the<br />

middle of the historical EV/sales range of 0.7x-1.2x during the semiconductor<br />

recovery cycle. We base our valuation on EV/sales instead of P/E, as TEL<br />

trades at a premium P/E compared to its peers due to its strong cash position.<br />

We believe EV/sales is the valuation methodology to reflect its weaker growth<br />

potential compared with ASML, AMAT and ASMI.<br />

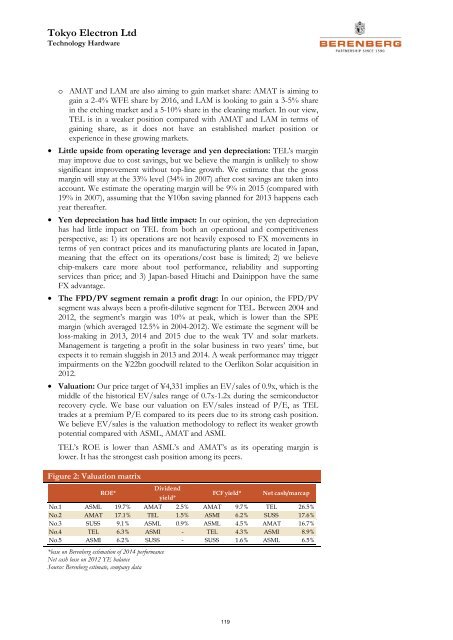

TEL’s ROE is lower than ASML’s and AMAT’s as its operating margin is<br />

lower. It has the strongest cash position among its peers.<br />

Figure 2: Valuation matrix<br />

ROE*<br />

Dividend<br />

yield*<br />

FCF yield* Net cash/marcap<br />

No.1 ASML 19.7% AMAT 2.5% AMAT 9.7% TEL 26.5%<br />

No.2 AMAT 17.1% TEL 1.5% ASMI 6.2% SUSS 17.6%<br />

No.3 SUSS 9.1% ASML 0.9% ASML 4.5% AMAT 16.7%<br />

No.4 TEL 6.3% ASMI - TEL 4.3% ASMI 8.9%<br />

No.5 ASMI 6.2% SUSS - SUSS 1.6% ASML 6.5%<br />

*base on <strong>Berenberg</strong> estimation of 2014 performance<br />

Net cash base on 2012 YE balance<br />

Source: <strong>Berenberg</strong> estimate, company data<br />

119