Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Tokyo Electron Ltd<br />

Technology Hardware<br />

tools is likely to grow at a slower pace. Gartner forecasts the photoresist<br />

processing market will grow by c1.4% between 2012 and 2017, versus growth in<br />

semiconductor capex of c4.1%.<br />

In 2015-16, when extreme ultraviolet lithography (EUV) starts to ship in volume,<br />

we may potentially see a higher top-line growth rate. The photoresist used for<br />

EUV is different from conventional lithography tools and requires a different type<br />

of photoresist equipment which may carry a high ASP. However, there is little<br />

visibility on revenue upside.<br />

Etching<br />

TEL generates 27% of its revenue from etching equipment, with a 29% market<br />

share globally in 2012. Some 85% of TEL’s etching revenue comes from shipping<br />

dielectric etching equipment, with the remainder from silicon etching equipment. It<br />

holds a dominant 63% share in the dielectric etching market, and a 9% share in<br />

silicon etching (LAM leads this market with a 59% share).<br />

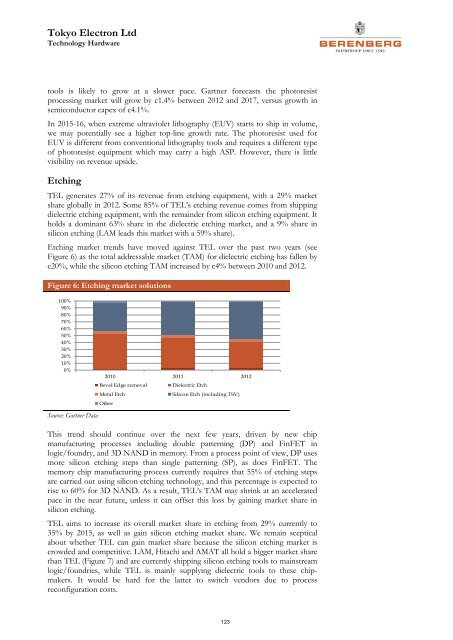

Etching market trends have moved against TEL over the past two years (see<br />

Figure 6) as the total addressable market (TAM) for dielectric etching has fallen by<br />

c20%, while the silicon etching TAM increased by c4% between 2010 and 2012.<br />

Figure 6: Etching market solutions<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Source: Gartner Data<br />

2010 2011 2012<br />

Bevel Edge removal Dielectric Etch<br />

Metal Etch<br />

Other<br />

Silicon Etch (including TSV)<br />

This trend should continue over the next few years, driven by new chip<br />

manufacturing processes including double patterning (DP) and FinFET in<br />

logic/foundry, and 3D NAND in memory. From a process point of view, DP uses<br />

more silicon etching steps than single patterning (SP), as does FinFET. The<br />

memory chip manufacturing process currently requires that 55% of etching steps<br />

are carried out using silicon etching technology, and this percentage is expected to<br />

rise to 60% for 3D NAND. As a result, TEL’s TAM may shrink at an accelerated<br />

pace in the near future, unless it can offset this loss by gaining market share in<br />

silicon etching.<br />

TEL aims to increase its overall market share in etching from 29% currently to<br />

35% by 2015, as well as gain silicon etching market share. We remain sceptical<br />

about whether TEL can gain market share because the silicon etching market is<br />

crowded and competitive. LAM, Hitachi and AMAT all hold a bigger market share<br />

than TEL (Figure 7) and are currently shipping silicon etching tools to mainstream<br />

logic/foundries, while TEL is mainly supplying dielectric tools to these chipmakers.<br />

It would be hard for the latter to switch vendors due to process<br />

reconfiguration costs.<br />

123