Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

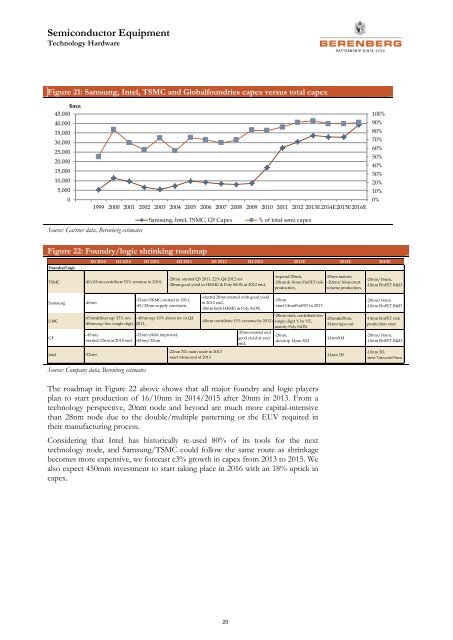

Figure 21: Samsung, Intel, TSMC and Globalfoundries capex versus total capex<br />

$mn<br />

45,000<br />

40,000<br />

35,000<br />

30,000<br />

25,000<br />

20,000<br />

15,000<br />

10,000<br />

5,000<br />

0<br />

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E2014E2015E2016E<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Source: Gartner data, <strong>Berenberg</strong> estimates<br />

Samsung, Intel, TSMC, GF Capex<br />

% of total semi capex<br />

Figure 22: Foundry/logic shrinking roadmap<br />

Foundry/Logic<br />

H1 2010 H2 2010 H1 2011 H2 2011 H1 2012 H2 2012 2013E 2014E 2015E<br />

TSMC<br />

-40/65nm contribute 53% revenue in 2010,<br />

-28nm started Q3 2011, 22% Q4 2012 rev<br />

-28nm good yield in HKMG & Poly SiON at 2012 end,<br />

-expand 28nm,<br />

-28nm mature,<br />

-20nm & 16nm FinFET risk - 20nm/16nm start<br />

production,<br />

volume production,<br />

-20nm/16nm,<br />

-10nm FInFET R&D.<br />

Samsung<br />

UMC<br />

GF<br />

Intel<br />

-40nm<br />

-65nm&finer eqv 35% rev, - 40nm eqv 10% above rev in Q4<br />

-40nm eqv low single digit. 2011,<br />

- 45nm,<br />

-started 32nm at 2010 end.<br />

-32nm<br />

-32nm HKMG started in 2011,<br />

-45/32nm supply constrain,<br />

-32nm yileld improved,<br />

-45nm/32nm<br />

-22nm 3D, main node in 2013<br />

-start 14nm end of 2013<br />

-started 28nm started with good yield<br />

in 2012 end,<br />

-28nm both HKMG & Poly SiON<br />

-28nm start, contribute low<br />

-28nm&20nm,<br />

-40nm contribute 15% revenue by 2012 esingle digit % by YE,<br />

-14nm tape out.<br />

mainly Poly SiON<br />

-28nm started and<br />

good yield at year<br />

end,<br />

-20nm<br />

-start 14nmFinFET in 2013<br />

-20nm,<br />

-develop 14nm XM<br />

-14nmXM<br />

-14nm 3D<br />

-20nm/14nm<br />

-10nm FInFET R&D<br />

-14nm FinFET risk<br />

production start<br />

-20nm/14nm,<br />

-10nm FInFET R&D.<br />

-10nm 3D,<br />

-next 7nm and 5nm<br />

Source: Company data, <strong>Berenberg</strong> estimates<br />

The roadmap in Figure 22 above shows that all major foundry and logic players<br />

plan to start production of 16/10nm in 2014/2015 after 20nm in 2013. From a<br />

technology perspective, 20nm node and beyond are much more capital-intensive<br />

than 28nm node due to the double/multiple patterning or the EUV required in<br />

their manufacturing process.<br />

Considering that Intel has historically re-used 80% of its tools for the next<br />

technology node, and Samsung/TSMC could follow the same route as shrinkage<br />

becomes more expensive, we forecast c3% growth in capex from 2013 to 2015. We<br />

also expect 450mm investment to start taking place in 2016 with an 18% uptick in<br />

capex.<br />

20