Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ASML Holding NV<br />

Technology Hardware<br />

Lithography market to double in size by 2016<br />

Consumer electronics will be the main driver of semiconductor growth in the next<br />

few years, in our opinion. Chip-makers are actively scaling their chip sizes down to<br />

facilitate the new generation of device designs, which are smaller, lighter, more<br />

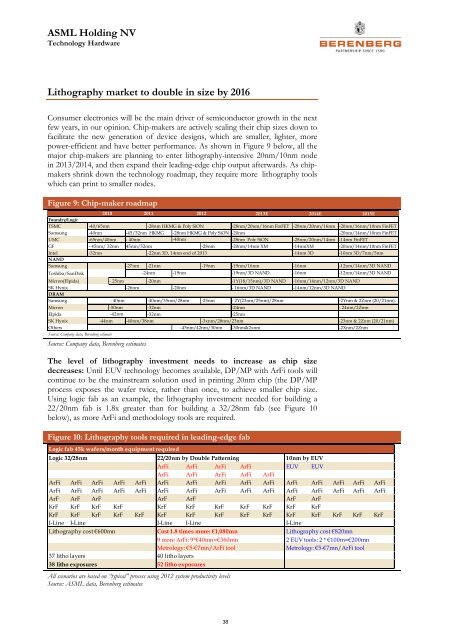

power-efficient and have better performance. As shown in Figure 9 below, all the<br />

major chip-makers are planning to enter lithography-intensive 20nm/10nm node<br />

in 2013/2014, and then expand their leading-edge chip output afterwards. As chipmakers<br />

shrink down the technology roadmap, they require more lithography tools<br />

which can print to smaller nodes.<br />

Figure 9: Chip-maker roadmap<br />

2010 2011 2012<br />

2013E 2014E 2015E<br />

Foundry/Logic<br />

TSMC<br />

-40/65nm<br />

-28nm HKMG & Poly SiON<br />

-28nm/20nm/16nm FinFET -28nm/20nm/16nm -20nm/16nm/10nm FinFET<br />

Samsung -40nm -45/32nm HKMG -28nm HKMG & Poly SiON -20nm<br />

-20nm/14nm/10nm FinFET<br />

UMC -65nm/40nm - 40nm -40nm<br />

-28nm Poly SiON -28nm/20nm/14nm -14nm FinFET<br />

GF - 45nm/ 32nm 45nm/32nm<br />

-28nm -20nm/14nm XM -14nmXM -20nm/14nm/10nm FinFET<br />

Intel -32nm -22nm 3D, 14nm end of 2013<br />

-14nm 3D -10nm 3D/7nm/5nm<br />

NAND<br />

Samsung -27nm -21nm<br />

-19nm -19nm/16nm -16nm -12nm/14nm/3D NAND<br />

Toshiba/SanDisk -24nm -19nm<br />

-19nm/3D NAND. -16nm -12nm/14nm/3D NAND<br />

Micron(Elpida)<br />

- 25nm -20nm -1Y(18/15nm)/3D NAND -16nm/14nm/12nm/3D NAND<br />

SK Hynix<br />

-26nm -20nm - 16nm/3D NAND -14nm/12nm/3D NAND<br />

DRAM<br />

Samsung - 40nm -40nm/35nm/28nm -25nm - 2Y(23nm/25nm)/28nm<br />

-2Ynm & 2Znm (20/21nm).<br />

Micron -50nm -32nm<br />

-24nm<br />

- 24nm/2Znm<br />

Elpida<br />

SK Hynix<br />

-42nm<br />

-44nm<br />

-32nm<br />

-40nm/38nm<br />

-25nm<br />

-3xnm/28nm/23nm<br />

Others<br />

-45nm/42nm/30nm -30nm&2xnm<br />

Source: Company data, <strong>Berenberg</strong> estimate<br />

Source: Company data, <strong>Berenberg</strong> estimates<br />

The level of lithography investment needs to increase as chip size<br />

decreases: Until EUV technology becomes available, DP/MP with ArFi tools will<br />

continue to be the mainstream solution used in printing 20nm chip (the DP/MP<br />

process exposes the wafer twice, rather than once, to achieve smaller chip size.<br />

Using logic fab as an example, the lithography investment needed for building a<br />

22/20nm fab is 1.8x greater than for building a 32/28nm fab (see Figure 10<br />

below), as more ArFi and methodology tools are required.<br />

Figure 10: Lithography tools required in leading-edge fab<br />

All scenarios are based on “typical” process using 2012 system productivity levels<br />

Source: ASML data, <strong>Berenberg</strong> estimates<br />

-23nm & 2Znm (20/21nm)<br />

-2Xnm/2Znm<br />

Logic fab 45k wafers/month equipment required<br />

Logic 32/28nm 22/20nm by Double Patterning 10nm by EUV<br />

ArFi ArFi ArFi ArFi EUV EUV<br />

ArFi ArFi ArFi ArFi ArFi<br />

ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi<br />

ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi ArFi<br />

ArF ArF ArF ArF ArF ArF ArF<br />

KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF<br />

KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF KrF<br />

I-Line I-Line I-Line I-Line I-Line<br />

Lithography cost €600mn Cost 1.8 times more: €1,080mn Lithography cost €820mn<br />

9 more ArFi: 9*€40mn=€360mn 2 EUV tools: 2 * €100m=€200mn<br />

Metrology: €5-€7mn/ArFi tool<br />

Metrology: €5-€7mn/ArFi tool<br />

37 litho layers 40 litho layers<br />

38 litho exposures 52 litho exposures<br />

38