Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

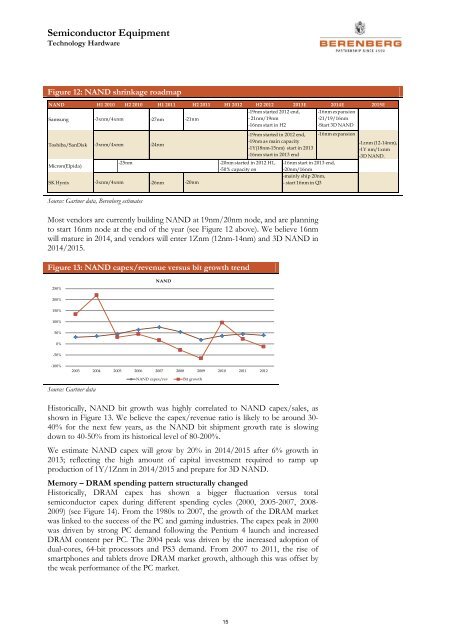

Figure 12: NAND shrinkage roadmap<br />

NAND H1 2010 H2 2010 H1 2011 H2 2011 H1 2012 H2 2012 2013E 2014E 2015E<br />

Samsung<br />

Toshiba/SanDisk<br />

Micron(Elpida)<br />

-3xnm/4xnm<br />

-3xnm/4xnm<br />

-27nm<br />

-24nm<br />

-21nm<br />

SK Hynix -3xnm/4xnm<br />

-26nm -20nm<br />

-19nm started 2012 end,<br />

- 21nm/19nm<br />

-16nm start in H2<br />

-25nm -20nm started in 2012 H1,<br />

-50% capacity on<br />

-19nm started in 2012 end,<br />

-19nm as main capacity<br />

-1Y(18nm-15nm) start in 2013<br />

-16nm start in 2013 end<br />

-16nm expansion<br />

-21/19/16nm<br />

-Start 3D NAND<br />

-16nm expansion<br />

-16nm start in 2013 end,<br />

-20nm/16nm<br />

-mainly ship 20nm,<br />

- start 16nm in Q3<br />

-1znm (12-14nm),<br />

-1Y nm/1xnm<br />

-3D NAND.<br />

Source: Gartner data, <strong>Berenberg</strong> estimates<br />

Most vendors are currently building NAND at 19nm/20nm node, and are planning<br />

to start 16nm node at the end of the year (see Figure 12 above). We believe 16nm<br />

will mature in 2014, and vendors will enter 1Znm (12nm-14nm) and 3D NAND in<br />

2014/2015.<br />

Figure 13: NAND capex/revenue versus bit growth trend<br />

250%<br />

NAND<br />

200%<br />

150%<br />

100%<br />

50%<br />

0%<br />

-50%<br />

-100%<br />

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012<br />

Source: Gartner data<br />

NAND capex/rev<br />

Bit growth<br />

Historically, NAND bit growth was highly correlated to NAND capex/sales, as<br />

shown in Figure 13. We believe the capex/revenue ratio is likely to be around 30-<br />

40% for the next few years, as the NAND bit shipment growth rate is slowing<br />

down to 40-50% from its historical level of 80-200%.<br />

We estimate NAND capex will grow by 20% in 2014/2015 after 6% growth in<br />

2013; reflecting the high amount of capital investment required to ramp up<br />

production of 1Y/1Znm in 2014/2015 and prepare for 3D NAND.<br />

Memory – DRAM spending pattern structurally changed<br />

Historically, DRAM capex has shown a bigger fluctuation versus total<br />

semiconductor capex during different spending cycles (2000, 2005-2007, 2008-<br />

2009) (see Figure 14). From the 1980s to 2007, the growth of the DRAM market<br />

was linked to the success of the PC and gaming industries. The capex peak in 2000<br />

was driven by strong PC demand following the Pentium 4 launch and increased<br />

DRAM content per PC. The 2004 peak was driven by the increased adoption of<br />

dual-cores, 64-bit processors and PS3 demand. From 2007 to 2011, the rise of<br />

smartphones and tablets drove DRAM market growth, although this was offset by<br />

the weak performance of the PC market.<br />

15