Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

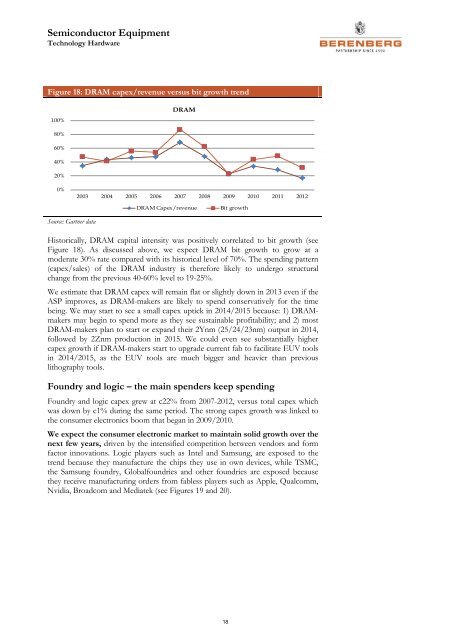

Figure 18: DRAM capex/revenue versus bit growth trend<br />

DRAM<br />

100%<br />

80%<br />

60%<br />

40%<br />

20%<br />

0%<br />

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012<br />

DRAM Capex/revenue<br />

Bit growth<br />

Source: Gartner data<br />

Historically, DRAM capital intensity was positively correlated to bit growth (see<br />

Figure 18). As discussed above, we expect DRAM bit growth to grow at a<br />

moderate 30% rate compared with its historical level of 70%. The spending pattern<br />

(capex/sales) of the DRAM industry is therefore likely to undergo structural<br />

change from the previous 40-60% level to 19-25%.<br />

We estimate that DRAM capex will remain flat or slightly down in 2013 even if the<br />

ASP improves, as DRAM-makers are likely to spend conservatively for the time<br />

being. We may start to see a small capex uptick in 2014/2015 because: 1) DRAMmakers<br />

may begin to spend more as they see sustainable profitability; and 2) most<br />

DRAM-makers plan to start or expand their 2Ynm (25/24/23nm) output in 2014,<br />

followed by 2Znm production in 2015. We could even see substantially higher<br />

capex growth if DRAM-makers start to upgrade current fab to facilitate EUV tools<br />

in 2014/2015, as the EUV tools are much bigger and heavier than previous<br />

lithography tools.<br />

Foundry and logic – the main spenders keep spending<br />

Foundry and logic capex grew at c22% from 2007-2012, versus total capex which<br />

was down by c1% during the same period. The strong capex growth was linked to<br />

the consumer electronics boom that began in 2009/2010.<br />

We expect the consumer electronic market to maintain solid growth over the<br />

next few years, driven by the intensified competition between vendors and form<br />

factor innovations. Logic players such as Intel and Samsung, are exposed to the<br />

trend because they manufacture the chips they use in own devices, while TSMC,<br />

the Samsung foundry, Globalfoundries and other foundries are exposed because<br />

they receive manufacturing orders from fabless players such as Apple, Qualcomm,<br />

Nvidia, Broadcom and Mediatek (see Figures 19 and 20).<br />

18