Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

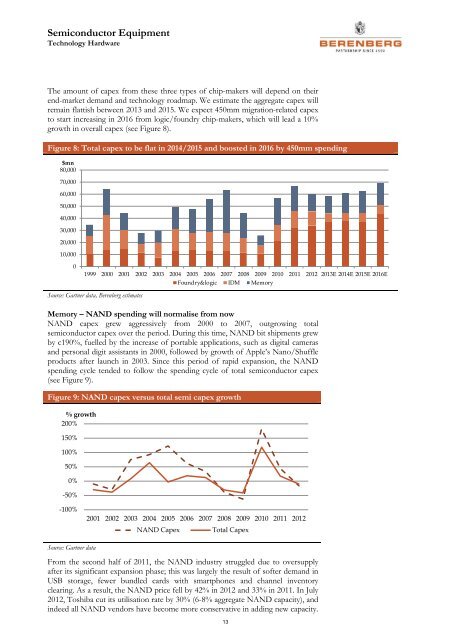

The amount of capex from these three types of chip-makers will depend on their<br />

end-market demand and technology roadmap. We estimate the aggregate capex will<br />

remain flattish between 2013 and 2015. We expect 450mm migration-related capex<br />

to start increasing in 2016 from logic/foundry chip-makers, which will lead a 10%<br />

growth in overall capex (see Figure 8).<br />

Figure 8: Total capex to be flat in 2014/2015 and boosted in 2016 by 450mm spending<br />

$mn<br />

80,000<br />

70,000<br />

60,000<br />

50,000<br />

40,000<br />

30,000<br />

20,000<br />

10,000<br />

0<br />

Source: Gartner data, <strong>Berenberg</strong> estimates<br />

Memory – NAND spending will normalise from now<br />

NAND capex grew aggressively from 2000 to 2007, outgrowing total<br />

semiconductor capex over the period. During this time, NAND bit shipments grew<br />

by c190%, fuelled by the increase of portable applications, such as digital cameras<br />

and personal digit assistants in 2000, followed by growth of Apple’s Nano/Shuffle<br />

products after launch in 2003. Since this period of rapid expansion, the NAND<br />

spending cycle tended to follow the spending cycle of total semiconductor capex<br />

(see Figure 9).<br />

Figure 9: NAND capex versus total semi capex growth<br />

% growth<br />

200%<br />

150%<br />

100%<br />

50%<br />

0%<br />

-50%<br />

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E<br />

Foundry&logic IDM Memory<br />

-100%<br />

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012<br />

NAND Capex<br />

Total Capex<br />

Source: Gartner data<br />

From the second half of 2011, the NAND industry struggled due to oversupply<br />

after its significant expansion phase; this was largely the result of softer demand in<br />

USB storage, fewer bundled cards with smartphones and channel inventory<br />

clearing. As a result, the NAND price fell by 42% in 2012 and 33% in 2011. In July<br />

2012, Toshiba cut its utilisation rate by 30% (6-8% aggregate NAND capacity), and<br />

indeed all NAND vendors have become more conservative in adding new capacity.<br />

13