Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

We believe the lithography, process control, and wafer level packaging markets<br />

have the biggest growth potential, driven by node shrinkage and 3D packaging<br />

demand, hence ASML, KLA and SUSS are likely to outperform other equipment<br />

suppliers. We do not like the etching, deposition and die level packaging markets<br />

because their growth potential is limited as a result of technology migration.<br />

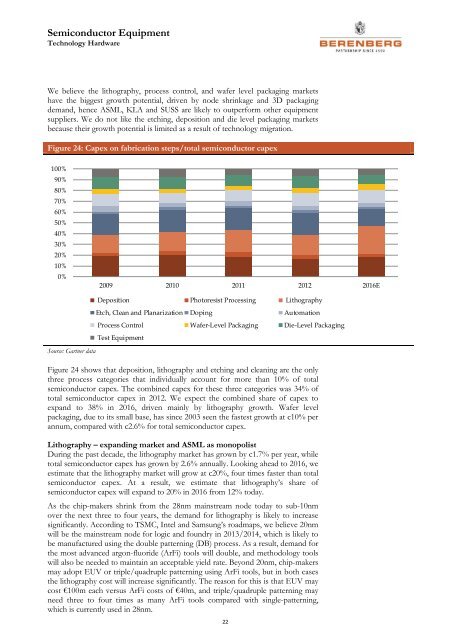

Figure 24: Capex on fabrication steps/total semiconductor capex<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

2009 2010 2011 2012 2016E<br />

Deposition Photoresist Processing Lithography<br />

Etch, Clean and Planarization Doping Automation<br />

Process Control Wafer-Level Packaging Die-Level Packaging<br />

Test <strong>Equipment</strong><br />

Source: Gartner data<br />

Figure 24 shows that deposition, lithography and etching and cleaning are the only<br />

three process categories that individually account for more than 10% of total<br />

semiconductor capex. The combined capex for these three categories was 34% of<br />

total semiconductor capex in 2012. We expect the combined share of capex to<br />

expand to 38% in 2016, driven mainly by lithography growth. Wafer level<br />

packaging, due to its small base, has since 2003 seen the fastest growth at c10% per<br />

annum, compared with c2.6% for total semiconductor capex.<br />

Lithography – expanding market and ASML as monopolist<br />

During the past decade, the lithography market has grown by c1.7% per year, while<br />

total semiconductor capex has grown by 2.6% annually. Looking ahead to 2016, we<br />

estimate that the lithography market will grow at c20%, four times faster than total<br />

semiconductor capex. At a result, we estimate that lithography’s share of<br />

semiconductor capex will expand to 20% in 2016 from 12% today.<br />

As the chip-makers shrink from the 28nm mainstream node today to sub-10nm<br />

over the next three to four years, the demand for lithography is likely to increase<br />

significantly. According to TSMC, Intel and Samsung’s roadmaps, we believe 20nm<br />

will be the mainstream node for logic and foundry in 2013/2014, which is likely to<br />

be manufactured using the double patterning (DB) process. As a result, demand for<br />

the most advanced argon-fluoride (ArFi) tools will double, and methodology tools<br />

will also be needed to maintain an acceptable yield rate. Beyond 20nm, chip-makers<br />

may adopt EUV or triple/quadruple patterning using ArFi tools, but in both cases<br />

the lithography cost will increase significantly. The reason for this is that EUV may<br />

cost €100m each versus ArFi costs of €40m, and triple/quadruple patterning may<br />

need three to four times as many ArFi tools compared with single-patterning,<br />

which is currently used in 28nm.<br />

22