Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Applied Materials Inc<br />

Technology Hardware<br />

We remain cautious about the likelihood of a 2-4% share gain<br />

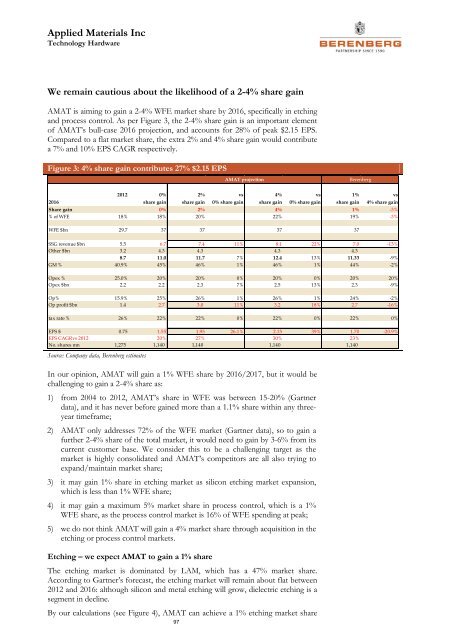

AMAT is aiming to gain a 2-4% WFE market share by 2016, specifically in etching<br />

and process control. As per Figure 3, the 2-4% share gain is an important element<br />

of AMAT’s bull-case 2016 projection, and accounts for 28% of peak $2.15 EPS.<br />

Compared to a flat market share, the extra 2% and 4% share gain would contribute<br />

a 7% and 10% EPS CAGR respectively.<br />

Figure 3: 4% share gain contributes 27% $2.15 EPS<br />

AMAT projection<br />

<strong>Berenberg</strong><br />

2012 0%<br />

2%<br />

vs<br />

4%<br />

vs<br />

1%<br />

vs<br />

2016<br />

share gain share gain 0% share gain share gain 0% share gain share gain 4% share gain<br />

Share gain 0% 2% 4% 1% -3%<br />

% of WFE 18% 18% 20% 22% 19% -3%<br />

WFE $bn 29.7 37 37 37 37<br />

SSG revenue $bn 5.5 6.7 7.4 11% 8.1 22% 7.0 -13%<br />

Other $bn 3.2 4.3 4.3 4.3 4.3<br />

8.7 11.0 11.7 7% 12.4 13% 11.33 -9%<br />

GM % 40.9% 45% 46% 1% 46% 1% 44% -2%<br />

Opex % 25.0% 20% 20% 0% 20% 0% 20% 20%<br />

Opex $bn 2.2 2.2 2.3 7% 2.5 13% 2.3 -9%<br />

Op% 15.9% 25% 26% 1% 26% 1% 24% -2%<br />

Op profit $bn 1.4 2.7 3.0 11% 3.2 18% 2.7 -16%<br />

tax rate % 26% 22% 22% 0% 22% 0% 22% 0%<br />

EPS $ 0.75 1.55 1.95 26.1% 2.15 39% 1.70 -20.9%<br />

EPS CAGRvs 2012 20% 27% 30% 23%<br />

No. shares mn 1,275 1,140 1,140 1,140 1,140<br />

Source: Company data, <strong>Berenberg</strong> estimates<br />

In our opinion, AMAT will gain a 1% WFE share by 2016/2017, but it would be<br />

challenging to gain a 2-4% share as:<br />

1) from 2004 to 2012, AMAT’s share in WFE was between 15-20% (Gartner<br />

data), and it has never before gained more than a 1.1% share within any threeyear<br />

timeframe;<br />

2) AMAT only addresses 72% of the WFE market (Gartner data), so to gain a<br />

further 2-4% share of the total market, it would need to gain by 3-6% from its<br />

current customer base. We consider this to be a challenging target as the<br />

market is highly consolidated and AMAT’s competitors are all also trying to<br />

expand/maintain market share;<br />

3) it may gain 1% share in etching market as silicon etching market expansion,<br />

which is less than 1% WFE share;<br />

4) it may gain a maximum 5% market share in process control, which is a 1%<br />

WFE share, as the process control market is 16% of WFE spending at peak;<br />

5) we do not think AMAT will gain a 4% market share through acquisition in the<br />

etching or process control markets.<br />

Etching – we expect AMAT to gain a 1% share<br />

The etching market is dominated by LAM, which has a 47% market share.<br />

According to Gartner’s forecast, the etching market will remain about flat between<br />

2012 and 2016: although silicon and metal etching will grow, dielectric etching is a<br />

segment in decline.<br />

By our calculations (see Figure 4), AMAT can achieve a 1% etching market share<br />

97