Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

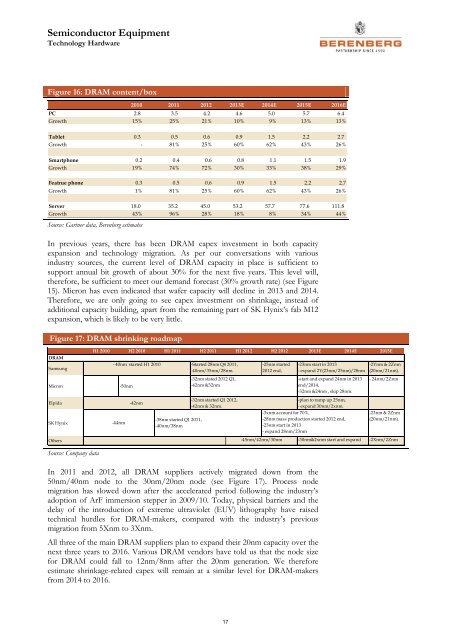

Figure 16: DRAM content/box<br />

2010 2011 2012 2013E 2014E 2015E 2016E<br />

PC 2.8 3.5 4.2 4.6 5.0 5.7 6.4<br />

Growth 15% 25% 21% 10% 9% 13% 13%<br />

Tablet 0.3 0.5 0.6 0.9 1.5 2.2 2.7<br />

Growth - 81% 25% 60% 62% 43% 26%<br />

Smartphone 0.2 0.4 0.6 0.8 1.1 1.5 1.9<br />

Growth 19% 74% 72% 30% 33% 38% 29%<br />

Featrue phone 0.3 0.5 0.6 0.9 1.5 2.2 2.7<br />

Growth 1% 81% 25% 60% 62% 43% 26%<br />

Server 18.0 35.2 45.0 53.2 57.7 77.6 111.8<br />

Growth 43% 96% 28% 18% 8% 34% 44%<br />

Source: Gartner data, <strong>Berenberg</strong> estimates<br />

In previous years, there has been DRAM capex investment in both capacity<br />

expansion and technology migration. As per our conversations with various<br />

industry sources, the current level of DRAM capacity in place is sufficient to<br />

support annual bit growth of about 30% for the next five years. This level will,<br />

therefore, be sufficient to meet our demand forecast (30% growth rate) (see Figure<br />

15). Micron has even indicated that wafer capacity will decline in 2013 and 2014.<br />

Therefore, we are only going to see capex investment on shrinkage, instead of<br />

additional capacity building, apart from the remaining part of SK Hynix’s fab M12<br />

expansion, which is likely to be very little.<br />

Figure 17: DRAM shrinking roadmap<br />

DRAM<br />

Samsung<br />

Micron<br />

H1 2010 H2 2010 H1 2011 H2 2011 H1 2012 H2 2012 2013E 2014E 2015E<br />

- 40nm started H1 2010 -Started 28nm Q4 2011,<br />

-40nm/35nm/28nm.<br />

-32nm stated 2012 Q1,<br />

-50nm<br />

-42nm &32nm<br />

-25nm started<br />

2012 end,<br />

-23nm start in 2013<br />

- expand 2Y(23nm/25nm)/28nm<br />

-start and expand 24nm in 2013<br />

end/2014,<br />

-32nm &24nm , skip 28nm.<br />

-2Ynm & 2Znm<br />

(20nm/21nm).<br />

- 24nm/2Znm<br />

Elpida<br />

SK Hynix<br />

-44nm<br />

-42nm<br />

-38nm started Q1 2011,<br />

-40nm/38nm<br />

-32nm started Q1 2012,<br />

-42nm & 32nm.<br />

-plan to ramp up 25nm,<br />

- expand 30nm/2xnm.<br />

-3xnm account for 70%,<br />

-28nm mass production started 2012 end,<br />

-23nm start in 2013<br />

- expand 28nm/23nm<br />

-23nm & 2Znm<br />

(20nm/21nm).<br />

Others<br />

-45nm/42nm/30nm<br />

-30nm&2xnm start and expand<br />

-2Xnm/2Znm<br />

Source: Company data<br />

In 2011 and 2012, all DRAM suppliers actively migrated down from the<br />

50nm/40nm node to the 30nm/20nm node (see Figure 17). Process node<br />

migration has slowed down after the accelerated period following the industry’s<br />

adoption of ArF immersion stepper in 2009/10. Today, physical barriers and the<br />

delay of the introduction of extreme ultraviolet (EUV) lithography have raised<br />

technical hurdles for DRAM-makers, compared with the industry’s previous<br />

migration from 5Xnm to 3Xnm.<br />

All three of the main DRAM suppliers plan to expand their 20nm capacity over the<br />

next three years to 2016. Various DRAM vendors have told us that the node size<br />

for DRAM could fall to 12nm/8nm after the 20nm generation. We therefore<br />

estimate shrinkage-related capex will remain at a similar level for DRAM-makers<br />

from 2014 to 2016.<br />

17