Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ASM International NV<br />

Small/Mid-Cap: Technology Hardware<br />

Financials<br />

ASMI has historically consolidated its ASMP results. However, following the<br />

disposal of 12% of its ASMP shares on 15 March 2013, it has deconsolidated<br />

these.<br />

ASMI’s revenue model<br />

We model ASMI’s revenue base on the front-end order intake trend.<br />

Figure 16: Revenue model<br />

Eur mn 2011 2012 2013E 2014E 2015E<br />

Revenue 1,634 1,418 559 477 499<br />

ASMI (front end) revenue 456 370 398 477 499<br />

ASMP (back end) revenue 1,178 1,048 160 - -<br />

Total New Orders 1,370 1,377 725 515 531<br />

ASMI (front end) new orders 398 360 491 515 531<br />

ASMI (front end) new orders yoy -2.2% -9.6% 36.3% 5.0% 3.0%<br />

ASMP (back end) new orders 971 1,017 234 - -<br />

Source: <strong>Berenberg</strong> estimates<br />

We estimate that ASMI’s underlying revenue will reach €559m in 2013, €160m of<br />

which will come from ASMP, and that the front-end operation’s revenue will grow<br />

to €467m in 2014. This top-line growth will be driven by the rising demand for<br />

ASMI’s equipment. With the increased adoption of HKMG in advanced chip<br />

manufacturing processes and ASMI’s strong share of the ALD market, we expect<br />

ALD equipment to increase its revenue contribution.<br />

We also expect its epitaxy revenue to grow as it may receive Intel orders for its<br />

new epitaxy tools. PE CVD is also contributing to revenue growth, but to a lesser<br />

extent because ASMI’s share of the market is minor compared with AMAT’s and<br />

LAM/Novellas’.<br />

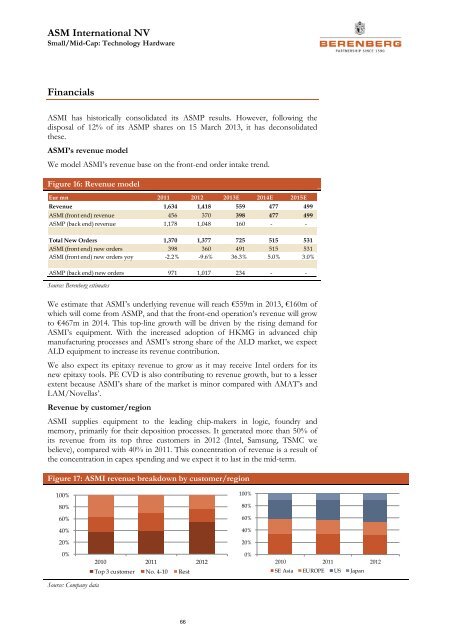

Revenue by customer/region<br />

ASMI supplies equipment to the leading chip-makers in logic, foundry and<br />

memory, primarily for their deposition processes. It generated more than 50% of<br />

its revenue from its top three customers in 2012 (Intel, Samsung, TSMC we<br />

believe), compared with 40% in 2011. This concentration of revenue is a result of<br />

the concentration in capex spending and we expect it to last in the mid-term.<br />

Figure 17: ASMI revenue breakdown by customer/region<br />

100%<br />

100%<br />

80%<br />

80%<br />

60%<br />

60%<br />

40%<br />

40%<br />

20%<br />

20%<br />

0%<br />

2010 2011 2012<br />

Top 3 customer No. 4-10 Rest<br />

0%<br />

2010 2011 2012<br />

SE Asia EUROPE US Japan<br />

Source: Company data<br />

66