Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

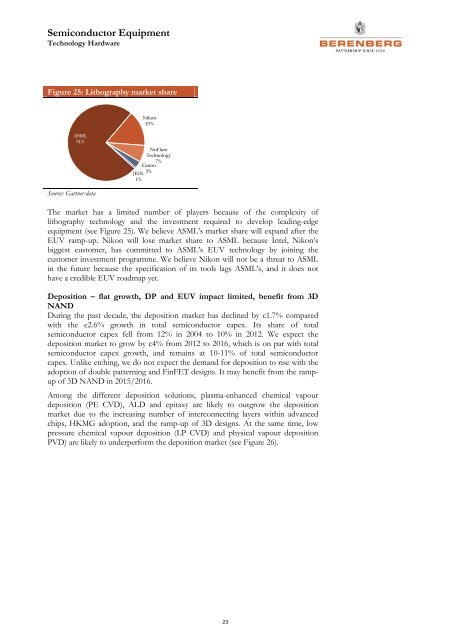

Figure 25: Lithography market share<br />

Nikon<br />

15%<br />

ASML<br />

74%<br />

NuFlare<br />

Technology<br />

7%<br />

Canon<br />

3%<br />

JEOL<br />

1%<br />

Source: Gartner data<br />

The market has a limited number of players because of the complexity of<br />

lithography technology and the investment required to develop leading-edge<br />

equipment (see Figure 25). We believe ASML’s market share will expand after the<br />

EUV ramp-up. Nikon will lose market share to ASML because Intel, Nikon’s<br />

biggest customer, has committed to ASML’s EUV technology by joining the<br />

customer investment programme. We believe Nikon will not be a threat to ASML<br />

in the future because the specification of its tools lags ASML’s, and it does not<br />

have a credible EUV roadmap yet.<br />

Deposition – flat growth, DP and EUV impact limited, benefit from 3D<br />

NAND<br />

During the past decade, the deposition market has declined by c1.7% compared<br />

with the c2.6% growth in total semiconductor capex. Its share of total<br />

semiconductor capex fell from 12% in 2004 to 10% in 2012. We expect the<br />

deposition market to grow by c4% from 2012 to 2016, which is on par with total<br />

semiconductor capex growth, and remains at 10-11% of total semiconductor<br />

capex. Unlike etching, we do not expect the demand for deposition to rise with the<br />

adoption of double patterning and FinFET designs. It may benefit from the rampup<br />

of 3D NAND in 2015/2016.<br />

Among the different deposition solutions, plasma-enhanced chemical vapour<br />

deposition (PE CVD), ALD and epitaxy are likely to outgrow the deposition<br />

market due to the increasing number of interconnecting layers within advanced<br />

chips, HKMG adoption, and the ramp-up of 3D designs. At the same time, low<br />

pressure chemical vapour deposition (LP CVD) and physical vapour deposition<br />

PVD) are likely to underperform the deposition market (see Figure 26).<br />

23