Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

Key debates<br />

Will the semiconductor space remain as cyclical as before?<br />

We believe the semiconductor cycle is going to remain cyclical, but less<br />

volatile compared to history. Over the past decade, we have seen cycle peaks in<br />

2000, 2007 and 2011, followed by a capacity digestion period, ie trough cycles in<br />

2002 and 2009, driven by different market trends. Memory was the main driver for<br />

the 2000 and 2008 cycle peak, and logic/foundry drove the peak cycle with<br />

memory in 2011.<br />

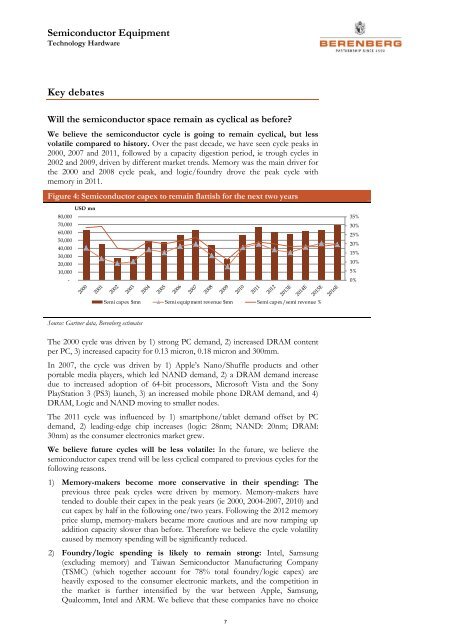

Figure 4: <strong>Semiconductor</strong> capex to remain flattish for the next two years<br />

USD mn<br />

80,000<br />

70,000<br />

60,000<br />

50,000<br />

40,000<br />

30,000<br />

20,000<br />

10,000<br />

-<br />

35%<br />

30%<br />

25%<br />

20%<br />

15%<br />

10%<br />

5%<br />

0%<br />

Semi capex $mn Semi equipment revenue $mn Semi capex/semi revenue %<br />

Source: Gartner data, <strong>Berenberg</strong> estimates<br />

The 2000 cycle was driven by 1) strong PC demand, 2) increased DRAM content<br />

per PC, 3) increased capacity for 0.13 micron, 0.18 micron and 300mm.<br />

In 2007, the cycle was driven by 1) Apple’s Nano/Shuffle products and other<br />

portable media players, which led NAND demand, 2) a DRAM demand increase<br />

due to increased adoption of 64-bit processors, Microsoft Vista and the Sony<br />

PlayStation 3 (PS3) launch, 3) an increased mobile phone DRAM demand, and 4)<br />

DRAM, Logic and NAND moving to smaller nodes.<br />

The 2011 cycle was influenced by 1) smartphone/tablet demand offset by PC<br />

demand, 2) leading-edge chip increases (logic: 28nm; NAND: 20nm; DRAM:<br />

30nm) as the consumer electronics market grew.<br />

We believe future cycles will be less volatile: In the future, we believe the<br />

semiconductor capex trend will be less cyclical compared to previous cycles for the<br />

following reasons.<br />

1) Memory-makers become more conservative in their spending: The<br />

previous three peak cycles were driven by memory. Memory-makers have<br />

tended to double their capex in the peak years (ie 2000, 2004-2007, 2010) and<br />

cut capex by half in the following one/two years. Following the 2012 memory<br />

price slump, memory-makers became more cautious and are now ramping up<br />

addition capacity slower than before. Therefore we believe the cycle volatility<br />

caused by memory spending will be significantly reduced.<br />

2) Foundry/logic spending is likely to remain strong: Intel, Samsung<br />

(excluding memory) and Taiwan <strong>Semiconductor</strong> Manufacturing Company<br />

(TSMC) (which together account for 78% total foundry/logic capex) are<br />

heavily exposed to the consumer electronic markets, and the competition in<br />

the market is further intensified by the war between Apple, Samsung,<br />

Qualcomm, Intel and ARM. We believe that these companies have no choice<br />

7