Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Applied Materials Inc<br />

Technology Hardware<br />

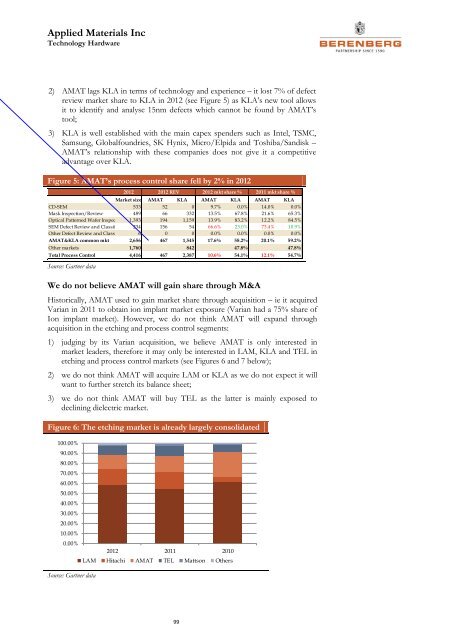

2) AMAT lags KLA in terms of technology and experience – it lost 7% of defect<br />

review market share to KLA in 2012 (see Figure 5) as KLA’s new tool allows<br />

it to identify and analyse 15nm defects which cannot be found by AMAT’s<br />

tool;<br />

3) KLA is well established with the main capex spenders such as Intel, TSMC,<br />

Samsung, Globalfoundries, SK Hynix, Micro/Elpida and Toshiba/Sandisk –<br />

AMAT’s relationship with these companies does not give it a competitive<br />

advantage over KLA.<br />

Figure 5: AMAT’s process control share fell by 2% in 2012<br />

2012<br />

2012 REV 2012 mkt share % 2011 mkt share %<br />

Market size AMAT KLA AMAT KLA AMAT KLA<br />

CD-SEM 533 52 0 9.7% 0.0% 14.0% 0.0%<br />

Mask Inspection/Review 489 66 332 13.5% 67.8% 21.6% 65.3%<br />

Optical Patterned Wafer Inspec 1,393 194 1,159 13.9% 83.2% 12.2% 84.5%<br />

SEM Defect Review and Classif 234 156 54 66.6% 23.0% 73.4% 10.9%<br />

Other Defect Review and Classi 6 0 0 0.0% 0.0% 0.0% 0.0%<br />

AMAT&KLA common mkt 2,656 467 1,545 17.6% 58.2% 20.1% 59.2%<br />

Other markets 1,760 842 47.8% 47.8%<br />

Total Process Control 4,416 467 2,387 10.6% 54.1% 12.1% 54.7%<br />

Source: Gartner data<br />

We do not believe AMAT will gain share through M&A<br />

Historically, AMAT used to gain market share through acquisition – ie it acquired<br />

Varian in 2011 to obtain ion implant market exposure (Varian had a 75% share of<br />

Ion implant market). However, we do not think AMAT will expand through<br />

acquisition in the etching and process control segments:<br />

1) judging by its Varian acquisition, we believe AMAT is only interested in<br />

market leaders, therefore it may only be interested in LAM, KLA and TEL in<br />

etching and process control markets (see Figures 6 and 7 below);<br />

2) we do not think AMAT will acquire LAM or KLA as we do not expect it will<br />

want to further stretch its balance sheet;<br />

3) we do not think AMAT will buy TEL as the latter is mainly exposed to<br />

declining dielectric market.<br />

Figure 6: The etching market is already largely consolidated<br />

100.00%<br />

90.00%<br />

80.00%<br />

70.00%<br />

60.00%<br />

50.00%<br />

40.00%<br />

30.00%<br />

20.00%<br />

10.00%<br />

0.00%<br />

Source: Gartner data<br />

2012 2011 2010<br />

LAM Hitachi AMAT TEL Mattson Others<br />

99