Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

How much are chip-makers spending?<br />

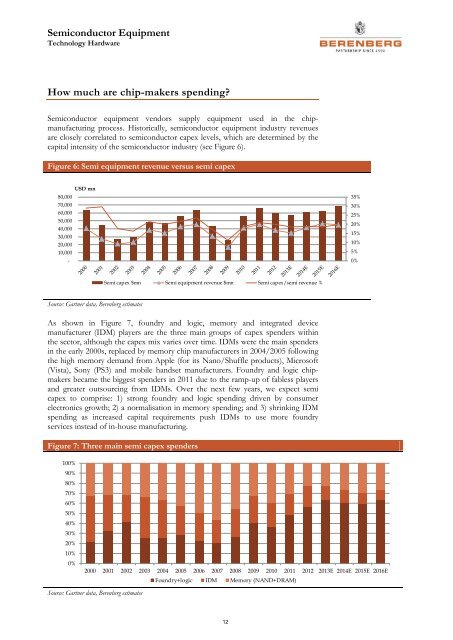

<strong>Semiconductor</strong> equipment vendors supply equipment used in the chipmanufacturing<br />

process. Historically, semiconductor equipment industry revenues<br />

are closely correlated to semiconductor capex levels, which are determined by the<br />

capital intensity of the semiconductor industry (see Figure 6).<br />

Figure 6: Semi equipment revenue versus semi capex<br />

USD mn<br />

80,000<br />

70,000<br />

60,000<br />

50,000<br />

40,000<br />

30,000<br />

20,000<br />

10,000<br />

-<br />

35%<br />

30%<br />

25%<br />

20%<br />

15%<br />

10%<br />

5%<br />

0%<br />

Semi capex $mn Semi equipment revenue $mn Semi capex/semi revenue %<br />

Source: Gartner data, <strong>Berenberg</strong> estimates<br />

As shown in Figure 7, foundry and logic, memory and integrated device<br />

manufacturer (IDM) players are the three main groups of capex spenders within<br />

the sector, although the capex mix varies over time. IDMs were the main spenders<br />

in the early 2000s, replaced by memory chip manufacturers in 2004/2005 following<br />

the high memory demand from Apple (for its Nano/Shuffle products), Microsoft<br />

(Vista), Sony (PS3) and mobile handset manufacturers. Foundry and logic chipmakers<br />

became the biggest spenders in 2011 due to the ramp-up of fabless players<br />

and greater outsourcing from IDMs. Over the next few years, we expect semi<br />

capex to comprise: 1) strong foundry and logic spending driven by consumer<br />

electronics growth; 2) a normalisation in memory spending; and 3) shrinking IDM<br />

spending as increased capital requirements push IDMs to use more foundry<br />

services instead of in-house manufacturing.<br />

Figure 7: Three main semi capex spenders<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E<br />

Foundry+logic IDM Memory (NAND+DRAM)<br />

Source: Gartner data, <strong>Berenberg</strong> estimates<br />

12