Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ASM International NV<br />

Small/Mid-Cap: Technology Hardware<br />

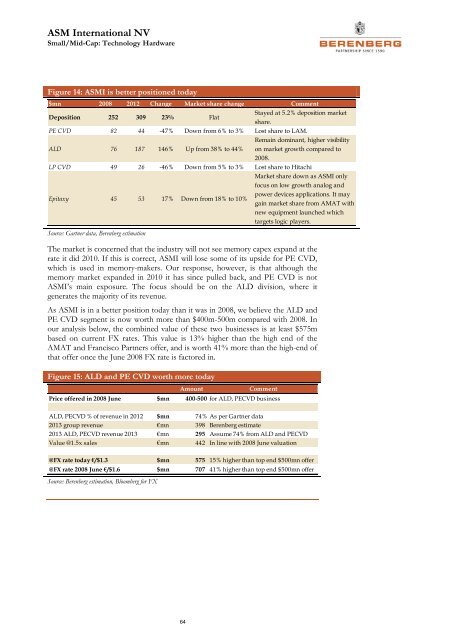

Figure 14: ASMI is better positioned today<br />

$mn 2008 2012 Change Market share change Comment<br />

Deposition 252 309 23% Flat<br />

Stayed at 5.2% deposition market<br />

share.<br />

PE CVD 82 44 -47% Down from 6% to 3% Lost share to LAM.<br />

ALD 76 187 146% Up from 38% to 44%<br />

Remain dominant, higher visibility<br />

on market growth compared to<br />

2008.<br />

LP CVD 49 26 -46% Down from 5% to 3% Lost share to Hitachi<br />

Epitaxy 45 53 17% Down from 18% to 10%<br />

Market share down as ASMI only<br />

focus on low growth analog and<br />

power devices applications. It may<br />

gain market share from AMAT with<br />

new equipment launched which<br />

targets logic players.<br />

Source: Gartner data, <strong>Berenberg</strong> estimation<br />

The market is concerned that the industry will not see memory capex expand at the<br />

rate it did 2010. If this is correct, ASMI will lose some of its upside for PE CVD,<br />

which is used in memory-makers. Our response, however, is that although the<br />

memory market expanded in 2010 it has since pulled back, and PE CVD is not<br />

ASMI’s main exposure. The focus should be on the ALD division, where it<br />

generates the majority of its revenue.<br />

As ASMI is in a better position today than it was in 2008, we believe the ALD and<br />

PE CVD segment is now worth more than $400m-500m compared with 2008. In<br />

our analysis below, the combined value of these two businesses is at least $575m<br />

based on current FX rates. This value is 13% higher than the high end of the<br />

AMAT and Francisco Partners offer, and is worth 41% more than the high-end of<br />

that offer once the June 2008 FX rate is factored in.<br />

Figure 15: ALD and PE CVD worth more today<br />

Amount<br />

Comment<br />

Price offered in 2008 June $mn 400-500 for ALD, PECVD business<br />

ALD, PECVD % of revenue in 2012 $mn 74% As per Gartner data<br />

2013 group revenue €mn 398 <strong>Berenberg</strong> estimate<br />

2013 ALD, PECVD revenue 2013 €mn 295 Assume 74% from ALD and PECVD<br />

Value @1.5x sales €mn 442 In line with 2008 June valuation<br />

@FX rate today €/$1.3 $mn 575 15% higher than top end $500mn offer<br />

@FX rate 2008 June €/$1.6 $mn 707 41% higher than top end $500mn offer<br />

Source: <strong>Berenberg</strong> estimation, Bloomberg for FX<br />

64