Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

ASM International NV<br />

Small/Mid-Cap: Technology Hardware<br />

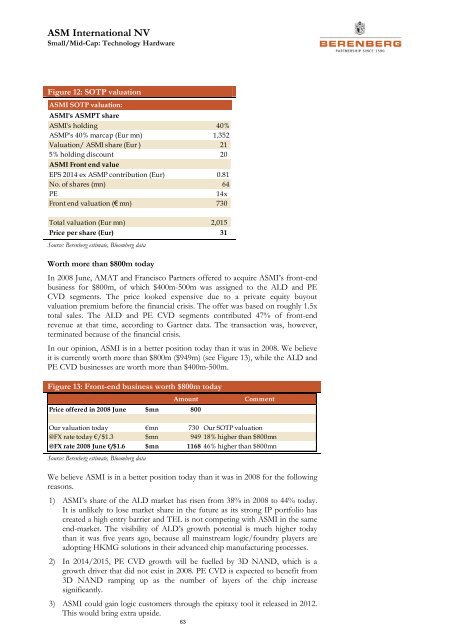

Figure 12: SOTP valuation<br />

ASMI SOTP valuation:<br />

ASMI's ASMPT share<br />

ASMI's holding 40%<br />

ASMP's 40% marcap (Eur mn) 1,352<br />

Valuation/ ASMI share (Eur ) 21<br />

5% holding discount 20<br />

ASMI Front end value<br />

EPS 2014 ex ASMP contribution (Eur) 0.81<br />

No. of shares (mn) 64<br />

PE<br />

14x<br />

Front end valuation (€ mn) 730<br />

Total valuation (Eur mn) 2,015<br />

Price per share (Eur) 31<br />

Source: <strong>Berenberg</strong> estimate, Bloomberg data<br />

Worth more than $800m today<br />

In 2008 June, AMAT and Francisco Partners offered to acquire ASMI’s front-end<br />

business for $800m, of which $400m-500m was assigned to the ALD and PE<br />

CVD segments. The price looked expensive due to a private equity buyout<br />

valuation premium before the financial crisis. The offer was based on roughly 1.5x<br />

total sales. The ALD and PE CVD segments contributed 47% of front-end<br />

revenue at that time, according to Gartner data. The transaction was, however,<br />

terminated because of the financial crisis.<br />

In our opinion, ASMI is in a better position today than it was in 2008. We believe<br />

it is currently worth more than $800m ($949m) (see Figure 13), while the ALD and<br />

PE CVD businesses are worth more than $400m-500m.<br />

Figure 13: Front-end business worth $800m today<br />

Amount<br />

Price offered in 2008 June $mn 800<br />

Comment<br />

Our valuation today €mn 730 Our SOTP valuation<br />

@FX rate today €/$1.3 $mn 949 18% higher than $800mn<br />

@FX rate 2008 June €/$1.6 $mn 1168 46% higher than $800mn<br />

Source: <strong>Berenberg</strong> estimate, Bloomberg data<br />

We believe ASMI is in a better position today than it was in 2008 for the following<br />

reasons.<br />

1) ASMI’s share of the ALD market has risen from 38% in 2008 to 44% today.<br />

It is unlikely to lose market share in the future as its strong IP portfolio has<br />

created a high entry barrier and TEL is not competing with ASMI in the same<br />

end-market. The visibility of ALD’s growth potential is much higher today<br />

than it was five years ago, because all mainstream logic/foundry players are<br />

adopting HKMG solutions in their advanced chip manufacturing processes.<br />

2) In 2014/2015, PE CVD growth will be fuelled by 3D NAND, which is a<br />

growth driver that did not exist in 2008. PE CVD is expected to benefit from<br />

3D NAND ramping up as the number of layers of the chip increase<br />

significantly.<br />

3) ASMI could gain logic customers through the epitaxy tool it released in 2012.<br />

This would bring extra upside.<br />

63