Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

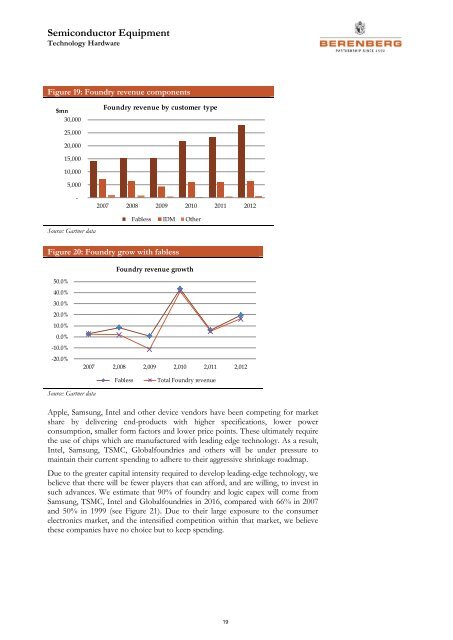

Figure 19: Foundry revenue components<br />

$mn<br />

30,000<br />

Foundry revenue by customer type<br />

25,000<br />

20,000<br />

15,000<br />

10,000<br />

5,000<br />

-<br />

2007 2008 2009 2010 2011 2012<br />

Fabless IDM Other<br />

Source: Gartner data<br />

Figure 20: Foundry grow with fabless<br />

Foundry revenue growth<br />

50.0%<br />

40.0%<br />

30.0%<br />

20.0%<br />

10.0%<br />

0.0%<br />

-10.0%<br />

-20.0%<br />

2007 2,008 2,009 2,010 2,011 2,012<br />

Fabless<br />

Total Foundry revenue<br />

Source: Gartner data<br />

Apple, Samsung, Intel and other device vendors have been competing for market<br />

share by delivering end-products with higher specifications, lower power<br />

consumption, smaller form factors and lower price points. These ultimately require<br />

the use of chips which are manufactured with leading edge technology. As a result,<br />

Intel, Samsung, TSMC, Globalfoundries and others will be under pressure to<br />

maintain their current spending to adhere to their aggressive shrinkage roadmap.<br />

Due to the greater capital intensity required to develop leading-edge technology, we<br />

believe that there will be fewer players that can afford, and are willing, to invest in<br />

such advances. We estimate that 90% of foundry and logic capex will come from<br />

Samsung, TSMC, Intel and Globalfoundries in 2016, compared with 66% in 2007<br />

and 50% in 1999 (see Figure 21). Due to their large exposure to the consumer<br />

electronics market, and the intensified competition within that market, we believe<br />

these companies have no choice but to keep spending.<br />

19