Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

ASML Holding NV<br />

Technology Hardware<br />

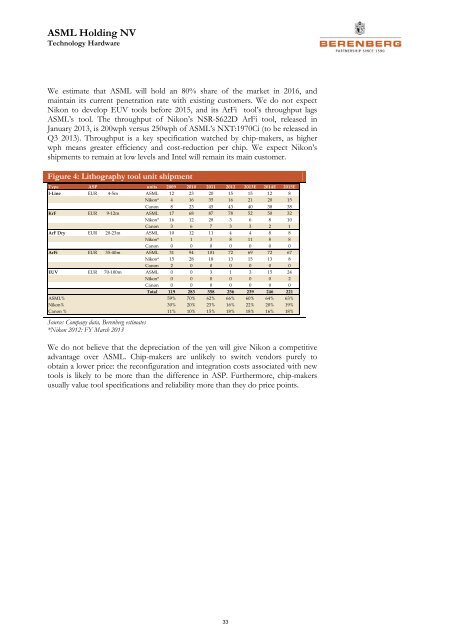

We estimate that ASML will hold an 80% share of the market in 2016, and<br />

maintain its current penetration rate with existing customers. We do not expect<br />

Nikon to develop EUV tools before 2015, and its ArFi tool’s throughput lags<br />

ASML’s tool. The throughput of Nikon’s NSR-S622D ArFi tool, released in<br />

January 2013, is 200wph versus 250wph of ASML’s NXT:1970Ci (to be released in<br />

Q3 2013). Throughput is a key specification watched by chip-makers, as higher<br />

wph means greater efficiency and cost-reduction per chip. We expect Nikon’s<br />

shipments to remain at low levels and Intel will remain its main customer.<br />

Figure 4: Lithography tool unit shipment<br />

Type ASP units 2009 2010 2011 2012 2013E 2014E 2015E<br />

I-Line EUR 4-5m ASML 12 23 20 15 15 12 8<br />

Nikon* 4 16 35 16 21 20 15<br />

Canon 8 23 45 43 40 38 38<br />

KrF EUR 9-12m ASML 17 68 87 78 52 50 32<br />

Nikon* 16 12 28 3 6 8 10<br />

Canon 3 6 7 3 3 2 1<br />

ArF Dry EUR 20-23m ASML 10 12 11 4 4 8 8<br />

Nikon* 1 1 3 8 11 8 8<br />

Canon 0 0 0 0 0 0 0<br />

ArFi EUR 35-40m ASML 31 94 101 72 69 72 67<br />

Nikon* 15 28 18 13 15 13 8<br />

Canon 2 0 0 0 0 0 0<br />

EUV EUR 70-100m ASML 0 0 3 1 3 15 24<br />

Nikon* 0 0 0 0 0 0 2<br />

Canon 0 0 0 0 0 0 0<br />

Total 119 283 358 256 239 246 221<br />

ASML% 59% 70% 62% 66% 60% 64% 63%<br />

Nikon% 30% 20% 23% 16% 22% 20% 19%<br />

Canon % 11% 10% 15% 18% 18% 16% 18%<br />

Source: Company data, <strong>Berenberg</strong> estimates<br />

*Nikon 2012: FY March 2013<br />

We do not believe that the depreciation of the yen will give Nikon a competitive<br />

advantage over ASML. Chip-makers are unlikely to switch vendors purely to<br />

obtain a lower price: the reconfiguration and integration costs associated with new<br />

tools is likely to be more than the difference in ASP. Furthermore, chip-makers<br />

usually value tool specifications and reliability more than they do price points.<br />

33