Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Suess Microtec AG<br />

Small/Mid-Cap: Technology Hardware<br />

Small, but active in growing markets<br />

• We initiate on Suess Microtec (SUSS) with a Buy<br />

recommendation and a price target of €9.4. SUSS supplies<br />

equipment used for chip packaging, photomask cleaning, and 3D<br />

integration, which will drive smaller chip sizes once shrinkage stops.<br />

Our Buy rating is based on the following: 1) the lithography segment’s<br />

strong performance (69% of SUSS’s revenue, and 100% of its profit),<br />

which is sufficient to drive group revenue growth; 2) Tamarack<br />

Scientific’s (acquired in 2012) margin may gradually converge to an<br />

average lithography margin of 20%; 3) bonder segment revenue is<br />

likely to triple in 2016/2017 once 3D bonder starts to ship in volume,<br />

driven by chip-makers expanding their 3D packaging capacity; and 4)<br />

the option value of more frequent cleaning for EUV photomasks as<br />

the move to EUV is made – the photomask segment’s revenue could<br />

double from the current €20m-40m level in 2015/2016.<br />

• Key debates: 1) How will the company’s “bread-and-butter”<br />

lithography segment perform in the future? 2) When will 3D bonding<br />

tools show significant growth? 3) Could SUSS become an acquisition<br />

target given its 3D bonding speciality?<br />

1. We expect the lithography segment to grow at 22% in 2014 and<br />

24% in 2015. With Tamarack’s contribution, semiconductor cycle<br />

recovery momentum and its high-growth end-market exposure,<br />

lithography is expected to contribute 100% of group revenue<br />

growth and 95% of group profit growth in 2015. It can therefore<br />

drive group growth even in the absence of a significant<br />

improvement in the other segments.<br />

2. 3D bonder volume shipments may not start before 2016/17, and<br />

some chip-makers may start building pilot lines in 2014/15; our<br />

bull-case assumption gives 9% and 8% revenue upside to our<br />

current group revenue estimates in 2014 and 2015 respectively.<br />

3. We think that an acquisition of SUSS’s 3D bonding business is<br />

unlikely given that: a) AMAT has used EV Group since 2009,<br />

and b) TEL may not have any further acquisition plans in the<br />

near term after acquiring Oerlikon and FSI in 2012.<br />

• Our EPS forecasts are 8% and 11% above consensus for 2014 and<br />

2015. We believe that the lithography segment will be able to drive<br />

total revenue and profit growth even without a material improvement<br />

from the bonder and photomask divisions. We estimate the<br />

lithography operating margin will slowly normalise to 20% after<br />

Tamarack’s integration.<br />

• Our €9.4 price target is based on 14x P/E on 2014 adjusted EPS of<br />

€0.67. The 14x P/E is at the mid of the historical 11-18x multiple<br />

applied in the middle of the order recovery cycle.<br />

Y/E 31.12., EUR m 2011 2012 2013E 2014E 2015E<br />

Sales 175 164 153 188 215<br />

EBIT 19 12 -8 19 29<br />

Net profit 15 8 -8 13 20<br />

Y/E net debt (net cash) -46 -26 -5 -7 -21<br />

EPS (reported) 0.77 0.49 -0.40 0.67 1.04<br />

EPS (Proforma) 0.77 0.41 -0.04 0.67 1.04<br />

CPS 2.43 1.34 0.26 0.38 1.09<br />

DPS 0.00 0.00 0.00 0.00 0.00<br />

Gross margin 37.8% 35.0% 30.0% 36.5% 38.8%<br />

EBIT margin 10.6% 7.2% -5.5% 9.9% 13.7%<br />

Dividend yield 0.0% 0.0% 0.0% 0.0% 0.0%<br />

ROCE 12.9% 7.5% -6.0% 9.6% 13.1%<br />

EV/sales 0.6 0.7 0.9 0.7 0.6<br />

EV/EBIT 5.4 10.4 -17.0 7.5 4.3<br />

P/E 10.0 15.8 -19.3 11.4 7.4<br />

Source: Company data, <strong>Berenberg</strong><br />

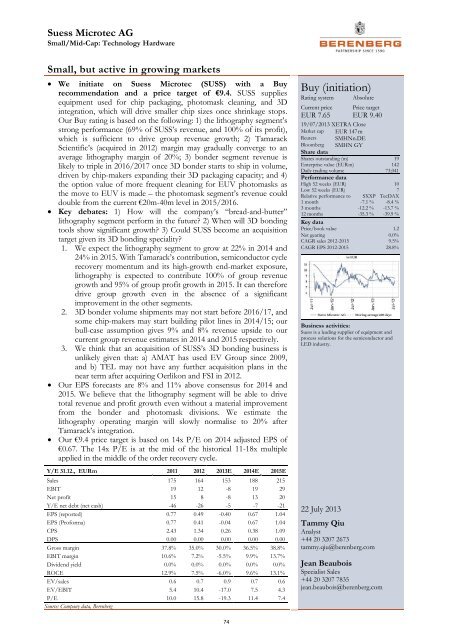

Buy (initiation)<br />

Rating system<br />

Current price<br />

EUR 7.65<br />

Absolute<br />

Price target<br />

EUR 9.40<br />

19/07/2013 XETRA Close<br />

Market cap EUR 147 m<br />

Reuters SMHNn.DE<br />

Bloomberg SMHN GY<br />

Share data<br />

Shares outstanding (m) 19<br />

Enterprise value (EUR m) 142<br />

Daily trading volume 73,041<br />

Performance data<br />

High 52 weeks (EUR) 10<br />

Low 52 weeks (EUR) 7<br />

Relative performance to SXXP TecDAX<br />

1 month -7.1 % -8.4 %<br />

3 months -12.2 % -13.7 %<br />

12 months -35.3 % -39.9 %<br />

Key data<br />

Price/book value 1.2<br />

Net gearing 0.0%<br />

CAGR sales 2012-2015 9.5%<br />

CAGR EPS 2012-2015 28.8%<br />

Business activities:<br />

Suess is a leading supplier of equipment and<br />

process solutions for the semiconductor and<br />

LED industry.<br />

22 July 2013<br />

Tammy Qiu<br />

Analyst<br />

+44 20 3207 2673<br />

tammy.qiu@berenberg.com<br />

Jean Beaubois<br />

Specialist Sales<br />

+44 20 3207 7835<br />

jean.beaubois@berenberg.com<br />

74