Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Suess Microtec AG<br />

Small/Mid-Cap: Technology Hardware<br />

Investment summary<br />

Our investment thesis on Buy-rated SUSS is predicated on four points.<br />

• Lithography can drive growth on its own, even without any contribution<br />

from the bonder and photomask divisions: We estimate group revenue and<br />

profit will grow at 14% and 58% respectively in 2015, with the lithography<br />

segment contributing 100% of group revenue growth and 83% of profit growth<br />

in 2015.<br />

The lithography segment is likely to show an organic growth rate similar to<br />

historical recovery cycle growth of ~15% in 2014 and 2015, and generate a<br />

~20% peak cycle margin. Tamarack’s contribution may triple to €30m by 2015,<br />

as SUSS is aiming to gain half of the back-end lithography market (a $60mn<br />

market). Along with Tamarack’s contribution, growth momentum from the<br />

semiconductor recovery cycle and strong growth in end-markets such as<br />

MEMS, we expect lithography to drive group revenue and profit growth on its<br />

own, without the company having to rely on significant improvements in other<br />

segments.<br />

• 3D bonder revenue may triple in 2016/17: Industry experts believe 3D<br />

integration could be one way to extend Moore’s law (ie that the number of<br />

components on integrated circuits doubles approximately every two years) once<br />

the physical shrinkage limit for chips is reached at ~5nm/3nm. Market<br />

researcher Yole Development expects the market to grow from $150m today to<br />

$500m-1bn in the next few years. In our opinion, even though we are not likely<br />

to see large order intakes before 2015/2016, the segment’s revenue could triple<br />

once volumes ramp up in 2016/2017. Our bull-case scenario for SUSS (seven<br />

tool shipments for 2014 and 2015 versus two tools by our estimates) suggests<br />

9% and 8% revenue upside and 42% and 18% operating profit upside for 2014<br />

and 2015 respectively compared to our current forecasts.<br />

• EUV photomask cleaning provides potential upside: SUSS holds a 100%<br />

share of the EUV photomask-cleaning tool market and an 80% share of the<br />

argon fluoride immersion (ArFi) photomask-cleaning tool market (combined<br />

market size: €50m-60m). We may see significant revenue upside in this segment<br />

once EUV volume shipments start in 2016, as EUV photomasks are likely to<br />

require more frequent cleaning than conventional photomasks as their structure<br />

is much more complex.<br />

• Valuation – at the middle of the range of historical multiples: Our price<br />

target of €9.4 is based on 14x P/E on 2014 adjusted EPS of €0.67, which is<br />

towards the middle of the historical 11-18x multiple range applied in the middle<br />

of the order recovery cycle.<br />

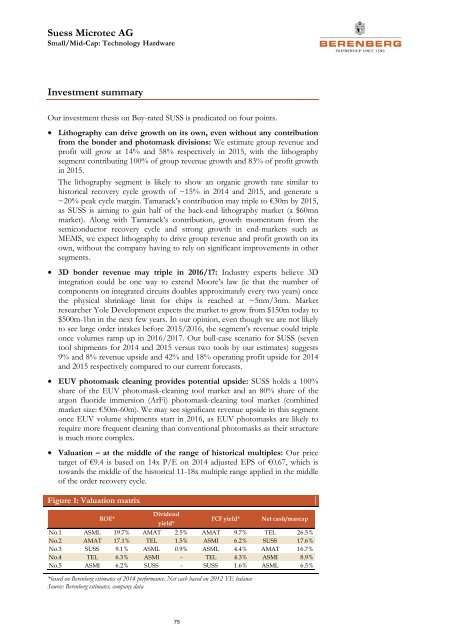

Figure 1: Valuation matrix<br />

ROE*<br />

Dividend<br />

yield*<br />

FCF yield* Net cash/marcap<br />

No.1 ASML 19.7% AMAT 2.5% AMAT 9.7% TEL 26.5%<br />

No.2 AMAT 17.1% TEL 1.5% ASMI 6.2% SUSS 17.6%<br />

No.3 SUSS 9.1% ASML 0.9% ASML 4.4% AMAT 16.7%<br />

No.4 TEL 6.3% ASMI - TEL 4.3% ASMI 8.9%<br />

No.5 ASMI 6.2% SUSS - SUSS 1.6% ASML 6.5%<br />

*based on <strong>Berenberg</strong> estimates of 2014 performance. Net cash based on 2012 YE balance<br />

Source: <strong>Berenberg</strong> estimates, company data<br />

75