Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Semiconductor</strong> <strong>Equipment</strong><br />

Technology Hardware<br />

Figure 26: Deposition solutions: PE CVD/ALD/epitaxy to<br />

outperform<br />

Deposition market by Solution<br />

30%<br />

25%<br />

20%<br />

15%<br />

10%<br />

5%<br />

0%<br />

2008 2009 2010 2011 2012<br />

LP CVD PE CVD ALD APCVD/SACVD<br />

PVD MO CVD Epitaxy<br />

Source: Gartner data<br />

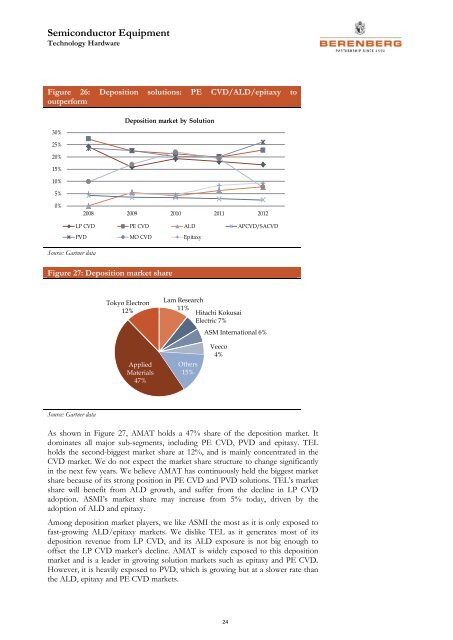

Figure 27: Deposition market share<br />

Tokyo Electron<br />

12%<br />

Lam Research<br />

11%<br />

Hitachi Kokusai<br />

Electric 7%<br />

ASM International 6%<br />

Applied<br />

Materials<br />

47%<br />

Others<br />

15%<br />

Veeco<br />

4%<br />

Source: Gartner data<br />

As shown in Figure 27, AMAT holds a 47% share of the deposition market. It<br />

dominates all major sub-segments, including PE CVD, PVD and epitaxy. TEL<br />

holds the second-biggest market share at 12%, and is mainly concentrated in the<br />

CVD market. We do not expect the market share structure to change significantly<br />

in the next few years. We believe AMAT has continuously held the biggest market<br />

share because of its strong position in PE CVD and PVD solutions. TEL’s market<br />

share will benefit from ALD growth, and suffer from the decline in LP CVD<br />

adoption. ASMI’s market share may increase from 5% today, driven by the<br />

adoption of ALD and epitaxy.<br />

Among deposition market players, we like ASMI the most as it is only exposed to<br />

fast-growing ALD/epitaxy markets. We dislike TEL as it generates most of its<br />

deposition revenue from LP CVD, and its ALD exposure is not big enough to<br />

offset the LP CVD market’s decline. AMAT is widely exposed to this deposition<br />

market and is a leader in growing solution markets such as epitaxy and PE CVD.<br />

However, it is heavily exposed to PVD, which is growing but at a slower rate than<br />

the ALD, epitaxy and PE CVD markets.<br />

24