Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ASML Holding NV<br />

Technology Hardware<br />

technology or materials, could hamper further share price performance.<br />

AMAT said at the US Semicon West 2013 conference in July that<br />

semiconductor companies are currently focusing more on new materials than<br />

they are on lithography scaling, ie EUV should have a minimal impact on the<br />

industry. AMAT also quoted that a fabless company suggested that 90% of its<br />

performance improvement came from materials, and only 10% from<br />

lithography. In addition, the consumer electronics market is currently driven<br />

by demand for mid- to low-end products, which do not require the most<br />

advanced chips. The demand for leading-edge chips could, therefore, decline if<br />

demand for mid- to low-end products rises.<br />

5. Valuation: Our price target of €73.00 implies a 12x P/E based on EPS<br />

estimates of €7.4/share, discounted by a 10% WACC. We have adopted this<br />

EPS estimate because it reflects the earnings power that EUV will, in our<br />

opinion, realise in 2016. Our 12x P/E has assigned a 10% premium to<br />

ASML’s historical mid-recovery-cycle P/E (9x-13x) to reflect ASML’s more<br />

competitive position (market share: 80% by 2016 compared with the last<br />

recovery cycle of 2010, when it had a market share of 70%).<br />

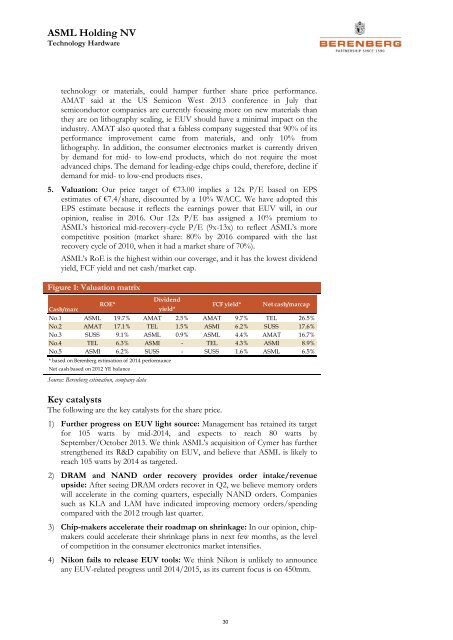

ASML’s RoE is the highest within our coverage, and it has the lowest dividend<br />

yield, FCF yield and net cash/market cap.<br />

Figure 1: Valuation matrix<br />

Dividend<br />

ROE*<br />

Cash/marc<br />

yield*<br />

FCF yield* Net cash/marcap<br />

No.1 ASML 19.7% AMAT 2.5% AMAT 9.7% TEL 26.5%<br />

No.2 AMAT 17.1% TEL 1.5% ASMI 6.2% SUSS 17.6%<br />

No.3 SUSS 9.1% ASML 0.9% ASML 4.4% AMAT 16.7%<br />

No.4 TEL 6.3% ASMI - TEL 4.3% ASMI 8.9%<br />

No.5 ASMI 6.2% SUSS - SUSS 1.6% ASML 6.5%<br />

* based on <strong>Berenberg</strong> estimation of 2014 performance<br />

Net cash based on 2012 YE balance<br />

Source: <strong>Berenberg</strong> estimation, company data<br />

Key catalysts<br />

The following are the key catalysts for the share price.<br />

1) Further progress on EUV light source: Management has retained its target<br />

for 105 watts by mid-2014, and expects to reach 80 watts by<br />

September/October 2013. We think ASML’s acquisition of Cymer has further<br />

strengthened its R&D capability on EUV, and believe that ASML is likely to<br />

reach 105 watts by 2014 as targeted.<br />

2) DRAM and NAND order recovery provides order intake/revenue<br />

upside: After seeing DRAM orders recover in Q2, we believe memory orders<br />

will accelerate in the coming quarters, especially NAND orders. Companies<br />

such as KLA and LAM have indicated improving memory orders/spending<br />

compared with the 2012 trough last quarter.<br />

3) Chip-makers accelerate their roadmap on shrinkage: In our opinion, chipmakers<br />

could accelerate their shrinkage plans in next few months, as the level<br />

of competition in the consumer electronics market intensifies.<br />

4) Nikon fails to release EUV tools: We think Nikon is unlikely to announce<br />

any EUV-related progress until 2014/2015, as its current focus is on 450mm.<br />

30