Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

Semiconductor Equipment - Berenberg Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ASM International NV<br />

Small/Mid-Cap: Technology Hardware<br />

Strong fundamentals unrecognised<br />

Consensus focus on front-end implied valuation<br />

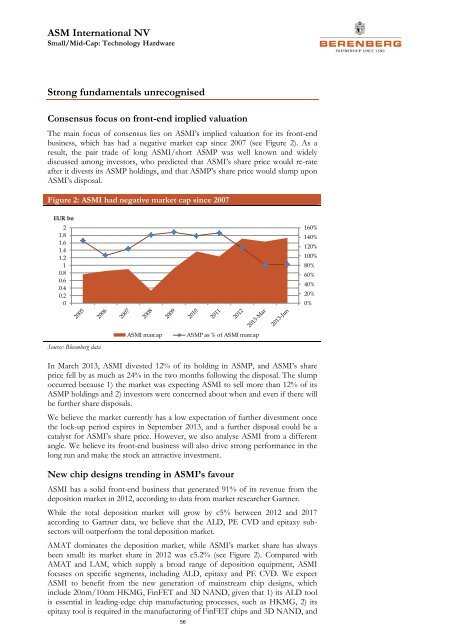

The main focus of consensus lies on ASMI’s implied valuation for its front-end<br />

business, which has had a negative market cap since 2007 (see Figure 2). As a<br />

result, the pair trade of long ASMI/short ASMP was well known and widely<br />

discussed among investors, who predicted that ASMI’s share price would re-rate<br />

after it divests its ASMP holdings, and that ASMP’s share price would slump upon<br />

ASMI’s disposal.<br />

Figure 2: ASMI had negative market cap since 2007<br />

EUR bn<br />

2<br />

1.8<br />

1.6<br />

1.4<br />

1.2<br />

1<br />

0.8<br />

0.6<br />

0.4<br />

0.2<br />

0<br />

160%<br />

140%<br />

120%<br />

100%<br />

80%<br />

60%<br />

40%<br />

20%<br />

0%<br />

Source: Bloomberg data<br />

ASMI marcap<br />

ASMP as % of ASMI marcap<br />

In March 2013, ASMI divested 12% of its holding in ASMP, and ASMI’s share<br />

price fell by as much as 24% in the two months following the disposal. The slump<br />

occurred because 1) the market was expecting ASMI to sell more than 12% of its<br />

ASMP holdings and 2) investors were concerned about when and even if there will<br />

be further share disposals.<br />

We believe the market currently has a low expectation of further divestment once<br />

the lock-up period expires in September 2013, and a further disposal could be a<br />

catalyst for ASMI’s share price. However, we also analyse ASMI from a different<br />

angle. We believe its front-end business will also drive strong performance in the<br />

long run and make the stock an attractive investment.<br />

New chip designs trending in ASMI’s favour<br />

ASMI has a solid front-end business that generated 91% of its revenue from the<br />

deposition market in 2012, according to data from market researcher Gartner.<br />

While the total deposition market will grow by c5% between 2012 and 2017<br />

according to Gartner data, we believe that the ALD, PE CVD and epitaxy subsectors<br />

will outperform the total deposition market.<br />

AMAT dominates the deposition market, while ASMI’s market share has always<br />

been small: its market share in 2012 was c5.2% (see Figure 2). Compared with<br />

AMAT and LAM, which supply a broad range of deposition equipment, ASMI<br />

focuses on specific segments, including ALD, epitaxy and PE CVD. We expect<br />

ASMI to benefit from the new generation of mainstream chip designs, which<br />

include 20nm/10nm HKMG, FinFET and 3D NAND, given that 1) its ALD tool<br />

is essential in leading-edge chip manufacturing processes, such as HKMG, 2) its<br />

epitaxy tool is required in the manufacturing of FinFET chips and 3D NAND, and<br />

56