Biffi, Network di imprese a Malpensa.pdf - OsserVa

Biffi, Network di imprese a Malpensa.pdf - OsserVa

Biffi, Network di imprese a Malpensa.pdf - OsserVa

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Camera <strong>di</strong> Commercio <strong>di</strong> Varese<br />

115<br />

STUDI E RICERCHE<br />

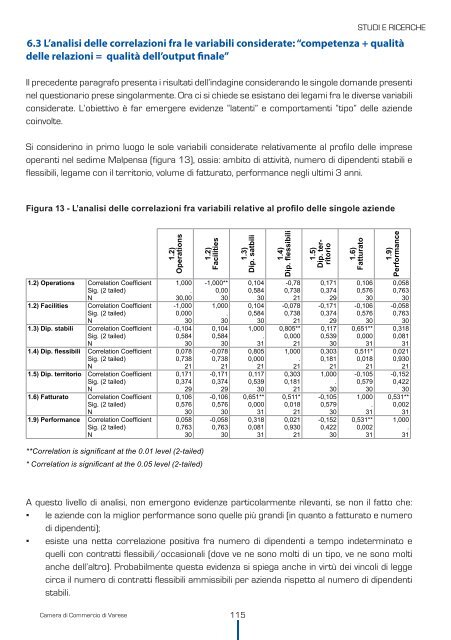

6.3 L’analisi delle correlazioni fra le variabili considerate: “competenza + qualità<br />

delle relazioni = qualità dell’output fi nale”<br />

Il precedente paragrafo presenta i risultati dell’indagine considerando le singole domande presenti<br />

nel questionario prese singolarmente. Ora ci si chiede se esistano dei legami fra le <strong>di</strong>verse variabili<br />

considerate. L’obiettivo è far emergere evidenze “latenti” e comportamenti “tipo” delle aziende<br />

coinvolte.<br />

Si considerino in primo luogo le sole variabili considerate relativamente al profilo delle <strong>imprese</strong><br />

operanti nel se<strong>di</strong>me <strong>Malpensa</strong> (figura 13), ossia: ambito <strong>di</strong> attività, numero <strong>di</strong> <strong>di</strong>pendenti stabili e<br />

flessibili, legame con il territorio, volume <strong>di</strong> fatturato, performance negli ultimi 3 anni.<br />

Figura 13 - L’analisi delle correlazioni fra variabili relative al profi lo delle singole aziende<br />

1.2) Operations Correlation Coeffi cient<br />

Sig. (2 tailed)<br />

N<br />

1.2) Facilities Correlation Coeffi cient<br />

Sig. (2 tailed)<br />

N<br />

1.3) Dip. stabili Correlation Coeffi cient<br />

Sig. (2 tailed)<br />

N<br />

1.4) Dip. fl essibili Correlation Coeffi cient<br />

Sig. (2 tailed)<br />

N<br />

1.5) Dip. territorio Correlation Coeffi cient<br />

Sig. (2 tailed)<br />

N<br />

1.6) Fatturato Correlation Coeffi cient<br />

Sig. (2 tailed)<br />

N<br />

1.9) Performance Correlation Coeffi cient<br />

Sig. (2 tailed)<br />

N<br />

1.2)<br />

Operations<br />

1,000<br />

.<br />

30,00<br />

-1,000<br />

0,000<br />

30<br />

-0,104<br />

0,584<br />

30<br />

0,078<br />

0,738<br />

21<br />

0,171<br />

0,374<br />

29<br />

0,106<br />

0,576<br />

30<br />

0,058<br />

0,763<br />

30<br />

**Correlation is signifi cant at the 0.01 level (2-tailed)<br />

* Correlation is signifi cant at the 0.05 level (2-tailed)<br />

1.2)<br />

Facilities<br />

-1,000**<br />

0,00<br />

30<br />

1,000<br />

.<br />

30<br />

0,104<br />

0,584<br />

30<br />

-0,078<br />

0,738<br />

21<br />

-0,171<br />

0,374<br />

29<br />

-0,106<br />

0,576<br />

30<br />

-0,058<br />

0,763<br />

30<br />

1.3)<br />

Dip. satbili<br />

0,104<br />

0,584<br />

30<br />

0,104<br />

0,584<br />

30<br />

1,000<br />

.<br />

31<br />

0,805<br />

0,000<br />

21<br />

0,117<br />

0,539<br />

30<br />

0,651**<br />

0,000<br />

31<br />

0,318<br />

0,081<br />

31<br />

1.4)<br />

Dip. fl essibili<br />

-0,78<br />

0,738<br />

21<br />

-0,078<br />

0,738<br />

21<br />

0,805**<br />

0,000<br />

21<br />

1,000<br />

.<br />

21<br />

0,303<br />

0,181<br />

21<br />

0,511*<br />

0,018<br />

21<br />

0,021<br />

0,930<br />

21<br />

1.5)<br />

Dip. territorio<br />

0,171<br />

0,374<br />

29<br />

-0,171<br />

0,374<br />

29<br />

0,117<br />

0,539<br />

30<br />

0,303<br />

0,181<br />

21<br />

1,000<br />

.<br />

30<br />

-0,105<br />

0,579<br />

30<br />

-0,152<br />

0,422<br />

30<br />

1.6)<br />

Fatturato<br />

0,106<br />

0,576<br />

30<br />

-0,106<br />

0,576<br />

30<br />

0,651**<br />

0,000<br />

31<br />

0,511*<br />

0,018<br />

21<br />

-0,105<br />

0,579<br />

30<br />

1,000<br />

.<br />

31<br />

0,531**<br />

0,002<br />

31<br />

1.9)<br />

Performance<br />

0,058<br />

0,763<br />

30<br />

-0,058<br />

0,763<br />

30<br />

0,318<br />

0,081<br />

31<br />

0,021<br />

0,930<br />

21<br />

-0,152<br />

0,422<br />

30<br />

0,531**<br />

0,002<br />

A questo livello <strong>di</strong> analisi, non emergono evidenze particolarmente rilevanti, se non il fatto che:<br />

▪ le aziende con la miglior performance sono quelle più gran<strong>di</strong> (in quanto a fatturato e numero<br />

<strong>di</strong> <strong>di</strong>pendenti);<br />

▪ esiste una netta correlazione positiva fra numero <strong>di</strong> <strong>di</strong>pendenti a tempo indeterminato e<br />

quelli con contratti flessibili/occasionali (dove ve ne sono molti <strong>di</strong> un tipo, ve ne sono molti<br />

anche dell’altro). Probabilmente questa evidenza si spiega anche in virtù dei vincoli <strong>di</strong> legge<br />

circa il numero <strong>di</strong> contratti flessibili ammissibili per azienda rispetto al numero <strong>di</strong> <strong>di</strong>pendenti<br />

stabili.<br />

31<br />

1,000<br />

.<br />

31