- Page 2:

This page intentionally left blank

- Page 6:

Editorial Director: Sally Yagan Edi

- Page 10:

To Joy, Forest, Byron, and Meredith

- Page 14:

This page intentionally left blank

- Page 18:

This page intentionally left blank

- Page 22:

x CONTENTS Industry Analysis: The E

- Page 26:

xii CONTENTS Part 4 Strategy Evalua

- Page 30:

xiv CONTENTS Cases HOSPITALITY/ENTE

- Page 34:

This page intentionally left blank

- Page 38:

xviii PREFACE issues and concerns.

- Page 42:

xx PREFACE current strategic-manage

- Page 46:

This page intentionally left blank

- Page 50:

xxiv ACKNOWLEDGMENTS with overly ag

- Page 54:

This page intentionally left blank

- Page 58:

xxviii CASE COMPANY INFORMATION MAT

- Page 62:

xxx CASE COMPANY INFORMATION MATRIX

- Page 66:

This page intentionally left blank

- Page 70:

PART 1 Overview of Strategic Manage

- Page 74:

4 PART 1 • OVERVIEW OF STRATEGIC

- Page 78:

6 PART 1 • OVERVIEW OF STRATEGIC

- Page 82:

8 PART 1 • OVERVIEW OF STRATEGIC

- Page 86:

10 PART 1 • OVERVIEW OF STRATEGIC

- Page 90:

12 PART 1 • OVERVIEW OF STRATEGIC

- Page 94:

14 PART 1 • OVERVIEW OF STRATEGIC

- Page 98:

16 PART 1 • OVERVIEW OF STRATEGIC

- Page 102:

18 PART 1 • OVERVIEW OF STRATEGIC

- Page 106:

20 PART 1 • OVERVIEW OF STRATEGIC

- Page 110:

22 PART 1 • OVERVIEW OF STRATEGIC

- Page 114:

24 PART 1 • OVERVIEW OF STRATEGIC

- Page 118:

26 PART 1 • OVERVIEW OF STRATEGIC

- Page 122:

28 PART 1 • OVERVIEW OF STRATEGIC

- Page 126:

30 PART 1 • OVERVIEW OF STRATEGIC

- Page 130:

32 PART 1 • OVERVIEW OF STRATEGIC

- Page 134:

34 PART 1 • OVERVIEW OF STRATEGIC

- Page 138:

36 PART 1 • OVERVIEW OF STRATEGIC

- Page 142:

38 PART 1 • OVERVIEW OF STRATEGIC

- Page 146:

PART 2 Strategy Formulation CHAPTER

- Page 150:

42 PART 2 • STRATEGY FORMULATION

- Page 154:

44 PART 2 • STRATEGY FORMULATION

- Page 158:

46 PART 2 • STRATEGY FORMULATION

- Page 162:

48 PART 2 • STRATEGY FORMULATION

- Page 166:

50 PART 2 • STRATEGY FORMULATION

- Page 170:

52 PART 2 • STRATEGY FORMULATION

- Page 174:

54 PART 2 • STRATEGY FORMULATION

- Page 178:

56 PART 2 • STRATEGY FORMULATION

- Page 182:

CHAPTER 3 The External Assessment C

- Page 186:

60 PART 2 • STRATEGY FORMULATION

- Page 190:

62 PART 2 • STRATEGY FORMULATION

- Page 194:

64 PART 2 • STRATEGY FORMULATION

- Page 198:

66 PART 2 • STRATEGY FORMULATION

- Page 202:

68 PART 2 • STRATEGY FORMULATION

- Page 206:

70 PART 2 • STRATEGY FORMULATION

- Page 210:

72 PART 2 • STRATEGY FORMULATION

- Page 214:

74 PART 2 • STRATEGY FORMULATION

- Page 218:

76 PART 2 • STRATEGY FORMULATION

- Page 222:

78 PART 2 • STRATEGY FORMULATION

- Page 226:

80 PART 2 • STRATEGY FORMULATION

- Page 230:

82 PART 2 • STRATEGY FORMULATION

- Page 234:

84 PART 2 • STRATEGY FORMULATION

- Page 238:

86 PART 2 • STRATEGY FORMULATION

- Page 242:

88 PART 2 • STRATEGY FORMULATION

- Page 246:

CHAPTER 4 The Internal Assessment C

- Page 250:

92 PART 2 • STRATEGY FORMULATION

- Page 254:

94 PART 2 • STRATEGY FORMULATION

- Page 258:

96 PART 2 • STRATEGY FORMULATION

- Page 262:

98 PART 2 • STRATEGY FORMULATION

- Page 266:

100 PART 2 • STRATEGY FORMULATION

- Page 270:

102 PART 2 • STRATEGY FORMULATION

- Page 274:

104 PART 2 • STRATEGY FORMULATION

- Page 278:

106 PART 2 • STRATEGY FORMULATION

- Page 282:

108 PART 2 • STRATEGY FORMULATION

- Page 286:

110 PART 2 • STRATEGY FORMULATION

- Page 290:

112 PART 2 • STRATEGY FORMULATION

- Page 294:

114 PART 2 • STRATEGY FORMULATION

- Page 298:

116 PART 2 • STRATEGY FORMULATION

- Page 302:

118 PART 2 • STRATEGY FORMULATION

- Page 306:

120 PART 2 • STRATEGY FORMULATION

- Page 310:

122 PART 2 • STRATEGY FORMULATION

- Page 314:

124 PART 2 • STRATEGY FORMULATION

- Page 318:

126 PART 2 • STRATEGY FORMULATION

- Page 322:

128 PART 2 • STRATEGY FORMULATION

- Page 326:

CHAPTER 5 Strategies in Action CHAP

- Page 330:

132 PART 2 • STRATEGY FORMULATION

- Page 334:

134 PART 2 • STRATEGY FORMULATION

- Page 338:

136 PART 2 • STRATEGY FORMULATION

- Page 342:

138 PART 2 • STRATEGY FORMULATION

- Page 346:

140 PART 2 • STRATEGY FORMULATION

- Page 350:

142 PART 2 • STRATEGY FORMULATION

- Page 354:

144 PART 2 • STRATEGY FORMULATION

- Page 358:

146 PART 2 • STRATEGY FORMULATION

- Page 362:

148 PART 2 • STRATEGY FORMULATION

- Page 366:

150 PART 2 • STRATEGY FORMULATION

- Page 370:

152 PART 2 • STRATEGY FORMULATION

- Page 374:

154 PART 2 • STRATEGY FORMULATION

- Page 378:

156 PART 2 • STRATEGY FORMULATION

- Page 382:

158 PART 2 • STRATEGY FORMULATION

- Page 386:

160 PART 2 • STRATEGY FORMULATION

- Page 390:

162 PART 2 • STRATEGY FORMULATION

- Page 394:

164 PART 2 • STRATEGY FORMULATION

- Page 398:

166 PART 2 • STRATEGY FORMULATION

- Page 402:

168 PART 2 • STRATEGY FORMULATION

- Page 406:

170 PART 2 • STRATEGY FORMULATION

- Page 410:

CHAPTER 6 Strategy Analysis and Cho

- Page 414:

174 PART 2 • STRATEGY FORMULATION

- Page 418:

176 PART 2 • STRATEGY FORMULATION

- Page 422:

178 PART 2 • STRATEGY FORMULATION

- Page 426:

180 PART 2 • STRATEGY FORMULATION

- Page 430:

182 PART 2 • STRATEGY FORMULATION

- Page 434:

184 PART 2 • STRATEGY FORMULATION

- Page 438:

186 PART 2 • STRATEGY FORMULATION

- Page 442:

188 PART 2 • STRATEGY FORMULATION

- Page 446:

190 PART 2 • STRATEGY FORMULATION

- Page 450:

192 PART 2 • STRATEGY FORMULATION

- Page 454:

194 PART 2 • STRATEGY FORMULATION

- Page 458:

196 PART 2 • STRATEGY FORMULATION

- Page 462:

198 PART 2 • STRATEGY FORMULATION

- Page 466:

200 PART 2 • STRATEGY FORMULATION

- Page 470:

202 PART 2 • STRATEGY FORMULATION

- Page 474:

204 PART 2 • STRATEGY FORMULATION

- Page 478:

206 PART 2 • STRATEGY FORMULATION

- Page 482:

208 PART 2 • STRATEGY FORMULATION

- Page 486:

PART 3 Strategy Implementation CHAP

- Page 490:

212 PART 3 • STRATEGY IMPLEMENTAT

- Page 494:

214 PART 3 • STRATEGY IMPLEMENTAT

- Page 498:

216 PART 3 • STRATEGY IMPLEMENTAT

- Page 502:

218 PART 3 • STRATEGY IMPLEMENTAT

- Page 506:

220 PART 3 • STRATEGY IMPLEMENTAT

- Page 510:

222 PART 3 • STRATEGY IMPLEMENTAT

- Page 514:

224 PART 3 • STRATEGY IMPLEMENTAT

- Page 518:

226 PART 3 • STRATEGY IMPLEMENTAT

- Page 522:

228 PART 3 • STRATEGY IMPLEMENTAT

- Page 526:

230 PART 3 • STRATEGY IMPLEMENTAT

- Page 530:

232 PART 3 • STRATEGY IMPLEMENTAT

- Page 534:

234 PART 3 • STRATEGY IMPLEMENTAT

- Page 538:

236 PART 3 • STRATEGY IMPLEMENTAT

- Page 542:

238 PART 3 • STRATEGY IMPLEMENTAT

- Page 546:

240 PART 3 • STRATEGY IMPLEMENTAT

- Page 550:

242 PART 3 • STRATEGY IMPLEMENTAT

- Page 554:

244 PART 3 • STRATEGY IMPLEMENTAT

- Page 558:

246 PART 3 • STRATEGY IMPLEMENTAT

- Page 562:

248 PART 3 • STRATEGY IMPLEMENTAT

- Page 566:

CHAPTER 8 Implementing Strategies:

- Page 570:

252 PART 3 • STRATEGY IMPLEMENTAT

- Page 574:

254 PART 3 • STRATEGY IMPLEMENTAT

- Page 578:

256 PART 3 • STRATEGY IMPLEMENTAT

- Page 582:

258 PART 3 • STRATEGY IMPLEMENTAT

- Page 586:

260 PART 3 • STRATEGY IMPLEMENTAT

- Page 590:

262 PART 3 • STRATEGY IMPLEMENTAT

- Page 594:

264 PART 3 • STRATEGY IMPLEMENTAT

- Page 598:

266 PART 3 • STRATEGY IMPLEMENTAT

- Page 602:

268 PART 3 • STRATEGY IMPLEMENTAT

- Page 606:

270 PART 3 • STRATEGY IMPLEMENTAT

- Page 610:

272 PART 3 • STRATEGY IMPLEMENTAT

- Page 614:

274 PART 3 • STRATEGY IMPLEMENTAT

- Page 618:

276 PART 3 • STRATEGY IMPLEMENTAT

- Page 622:

278 PART 3 • STRATEGY IMPLEMENTAT

- Page 626:

280 PART 3 • STRATEGY IMPLEMENTAT

- Page 630:

282 PART 3 • STRATEGY IMPLEMENTAT

- Page 634:

PART 4 Strategy Evaluation CHAPTER

- Page 638:

286 PART 4 • STRATEGY EVALUATION

- Page 642:

288 PART 4 • STRATEGY EVALUATION

- Page 646:

290 PART 4 • STRATEGY EVALUATION

- Page 650:

292 PART 4 • STRATEGY EVALUATION

- Page 654:

294 PART 4 • STRATEGY EVALUATION

- Page 658:

296 PART 4 • STRATEGY EVALUATION

- Page 662:

298 PART 4 • STRATEGY EVALUATION

- Page 666:

300 PART 4 • STRATEGY EVALUATION

- Page 670:

302 PART 4 • STRATEGY EVALUATION

- Page 674:

304 PART 4 • STRATEGY EVALUATION

- Page 678:

306 PART 4 • STRATEGY EVALUATION

- Page 682:

PART 5 Key Strategic-Management Top

- Page 686:

310 PART 5 • KEY STRATEGIC-MANAGE

- Page 690:

312 PART 5 • KEY STRATEGIC-MANAGE

- Page 694:

314 PART 5 • KEY STRATEGIC-MANAGE

- Page 698:

316 PART 5 • KEY STRATEGIC-MANAGE

- Page 702:

318 PART 5 • KEY STRATEGIC-MANAGE

- Page 706:

320 PART 5 • KEY STRATEGIC-MANAGE

- Page 710:

322 PART 5 • KEY STRATEGIC-MANAGE

- Page 714:

324 PART 5 • KEY STRATEGIC-MANAGE

- Page 718:

326 PART 5 • KEY STRATEGIC-MANAGE

- Page 722:

CHAPTER 11 Global/International Iss

- Page 726:

330 PART 5 • KEY STRATEGIC-MANAGE

- Page 730:

332 PART 5 • KEY STRATEGIC-MANAGE

- Page 734:

334 PART 5 • KEY STRATEGIC-MANAGE

- Page 738:

336 PART 5 • KEY STRATEGIC-MANAGE

- Page 742:

338 PART 5 • KEY STRATEGIC-MANAGE

- Page 746:

340 PART 5 • KEY STRATEGIC-MANAGE

- Page 750:

342 PART 5 • KEY STRATEGIC-MANAGE

- Page 754:

344 PART 5 • KEY STRATEGIC-MANAGE

- Page 758:

PART 6 Strategic-Management Case An

- Page 762:

348 PART 6 • STRATEGIC-MANAGEMENT

- Page 766:

350 PART 6 • STRATEGIC-MANAGEMENT

- Page 770:

352 PART 6 • STRATEGIC-MANAGEMENT

- Page 774:

354 PART 6 • STRATEGIC-MANAGEMENT

- Page 778:

356 PART 6 • STRATEGIC-MANAGEMENT

- Page 782:

358 PART 6 • STRATEGIC-MANAGEMENT

- Page 786:

360 INDEX Finkelstein, Sydney, 167

- Page 790:

362 INDEX Thai, Kim, 167, 280 Thomp

- Page 794:

364 INDEX E Economic forces, 63, 33

- Page 798:

366 INDEX Q OSPM, 192-196 Quality (

- Page 802:

This page intentionally left blank

- Page 806:

This page intentionally left blank

- Page 810:

2 MERNOUSH BANTON Disney Consumer P

- Page 814:

4 MERNOUSH BANTON EXHIBIT 3 Consoli

- Page 818:

6 MERNOUSH BANTON Entertainment Ser

- Page 822:

8 MERNOUSH BANTON EXHIBIT 9 Disney

- Page 826:

10 MERNOUSH BANTON EXHIBIT 11 Disne

- Page 830:

12 MERNOUSH BANTON The second large

- Page 834:

2 Merryland Amusement Park — 2009

- Page 838:

16 GREGORY STONE place for area fam

- Page 842:

18 GREGORY STONE EXHIBIT 4 Missouri

- Page 846:

20 GREGORY STONE Tony explored opti

- Page 850:

22 GREGORY STONE EXHIBIT 5 2008 Gen

- Page 854:

24 GREGORY STONE EXHIBIT 6 2008 Kan

- Page 858:

3 JetBlue Airways Corporation — 2

- Page 862:

28 MERNOUSH BANTON hub (Terminal 5

- Page 866:

30 MERNOUSH BANTON EXHIBIT 3 JetBlu

- Page 870:

32 MERNOUSH BANTON expenses rose 8.

- Page 874:

34 MERNOUSH BANTON EXHIBIT 7 Airlin

- Page 878:

36 MERNOUSH BANTON EXHIBIT 12 Airli

- Page 882:

38 CHARLES M. BYLES as a safe airli

- Page 886:

40 CHARLES M. BYLES in a number of

- Page 890:

42 CHARLES M. BYLES EXHIBIT 4 AirTr

- Page 894:

44 CHARLES M. BYLES EXHIBIT 6 Balan

- Page 898:

46 CHARLES M. BYLES shows that labo

- Page 902:

48 CHARLES M. BYLES EXHIBIT 12 JetB

- Page 906:

5 Family Dollar Stores, Inc. — 20

- Page 910:

52 JOSEPH W. LEONARD EXHIBIT 2 Fami

- Page 914:

54 JOSEPH W. LEONARD To support its

- Page 918:

56 JOSEPH W. LEONARD Beyond the fou

- Page 922:

58 JOSEPH W. LEONARD EXHIBIT 8 Fami

- Page 926:

60 AMIT J. SHAH AND MICHAEL L. MONA

- Page 930:

62 AMIT J. SHAH AND MICHAEL L. MONA

- Page 934:

64 AMIT J. SHAH AND MICHAEL L. MONA

- Page 938:

66 AMIT J. SHAH AND MICHAEL L. MONA

- Page 942:

68 AMIT J. SHAH AND MICHAEL L. MONA

- Page 946:

70 AMIT J. SHAH AND MICHAEL L. MONA

- Page 950:

72 AMIT J. SHAH AND MICHAEL L. MONA

- Page 954:

74 JAMES L. HARBIN AND PATRICIA HUM

- Page 958:

76 JAMES L. HARBIN AND PATRICIA HUM

- Page 962:

78 JAMES L. HARBIN AND PATRICIA HUM

- Page 966:

80 JAMES L. HARBIN AND PATRICIA HUM

- Page 970:

82 JAMES L. HARBIN AND PATRICIA HUM

- Page 974:

84 ROCHELLE R. BRUNSON AND MARLENE

- Page 978:

86 ROCHELLE R. BRUNSON AND MARLENE

- Page 982:

88 ROCHELLE R. BRUNSON AND MARLENE

- Page 986:

90 ROCHELLE R. BRUNSON AND MARLENE

- Page 990:

92 HAMID KAZEROONY The Web site sta

- Page 994:

94 HAMID KAZEROONY EXHIBIT 2 Consol

- Page 998:

96 HAMID KAZEROONY EXHIBIT 6 Search

- Page 1002:

98 HAMID KAZEROONY EXHIBIT 8 Top 25

- Page 1006:

100 LORI RADULOVICH EBay Inc. encom

- Page 1010:

102 LORI RADULOVICH A Trusted Onlin

- Page 1014:

104 LORI RADULOVICH The success of

- Page 1018:

106 LORI RADULOVICH ruled that eBay

- Page 1022:

108 LORI RADULOVICH EXHIBIT 4 eBay

- Page 1026:

110 LORI RADULOVICH EXHIBIT 7 eBay

- Page 1030:

112 DONALD L. CROOKS, ROBERT S. GOO

- Page 1034:

114 DONALD L. CROOKS, ROBERT S. GOO

- Page 1038:

116 DONALD L. CROOKS, ROBERT S. GOO

- Page 1042:

118 DONALD L. CROOKS, ROBERT S. GOO

- Page 1046:

12 Krispy Kreme Doughnuts (KKD) —

- Page 1050:

122 JOHN BURBRIDGE AND COLEMAN RICH

- Page 1054:

124 JOHN BURBRIDGE AND COLEMAN RICH

- Page 1058:

126 JOHN BURBRIDGE AND COLEMAN RICH

- Page 1062:

128 JOHN BURBRIDGE AND COLEMAN RICH

- Page 1066:

130 SHARYNN TOMLIN 30,000 worldwide

- Page 1070:

132 SHARYNN TOMLIN EXHIBIT 2 Starbu

- Page 1074:

134 SHARYNN TOMLIN For the second q

- Page 1078:

136 SHARYNN TOMLIN Albertson’s, R

- Page 1082:

14 The United States Postal Service

- Page 1086:

140 FRED AND FOREST DAVID spanned t

- Page 1090:

142 FRED AND FOREST DAVID EXHIBIT 4

- Page 1094:

144 FRED AND FOREST DAVID package d

- Page 1098:

146 FRED AND FOREST DAVID EXHIBIT 1

- Page 1102:

148 FRED AND FOREST DAVID EXHIBIT 1

- Page 1106:

15 National Railroad Passenger Corp

- Page 1110:

152 KRISTOPHER J. BLANCHARD Company

- Page 1114:

154 KRISTOPHER J. BLANCHARD EXHIBIT

- Page 1118:

156 KRISTOPHER J. BLANCHARD EXHIBIT

- Page 1122:

16 Goodwill of San Francisco, San M

- Page 1126:

160 MARY E. VRADELIS operations, it

- Page 1130:

162 MARY E. VRADELIS EXHIBIT 3 Good

- Page 1134:

164 MARY E. VRADELIS EXHIBIT 5 Fina

- Page 1138:

17 Harley-Davidson, Inc. — 2009 C

- Page 1142:

168 CAROL POPE AND JOANNE MACK EXHI

- Page 1146:

170 CAROL POPE AND JOANNE MACK EXHI

- Page 1150:

172 CAROL POPE AND JOANNE MACK whic

- Page 1154:

174 CAROL POPE AND JOANNE MACK EXHI

- Page 1158:

18 Ford Motor Company — 2009 Alen

- Page 1162:

178 ALEN BADAL Company Brands Ford

- Page 1166:

180 ALEN BADAL EXHIBIT 6 Ford’s B

- Page 1170:

182 ALEN BADAL Toyota operates in t

- Page 1174:

19 Kraft Foods Inc. — 2009 Kristo

- Page 1178:

186 KRISTOPHER J. BLANCHARD EXHIBIT

- Page 1182:

188 KRISTOPHER J. BLANCHARD EXHIBIT

- Page 1186:

190 KRISTOPHER J. BLANCHARD Custome

- Page 1190:

20 Hershey Company — 2009 Anne Wa

- Page 1194:

194 ANNE WALSH AND ELLEN MANSFIELD

- Page 1198:

196 ANNE WALSH AND ELLEN MANSFIELD

- Page 1202:

198 ANNE WALSH AND ELLEN MANSFIELD

- Page 1206:

200 ANNE WALSH AND ELLEN MANSFIELD

- Page 1210:

202 TOMLIN, MILHAUSER, GIERKE, LEFE

- Page 1214:

204 TOMLIN, MILHAUSER, GIERKE, LEFE

- Page 1218:

206 TOMLIN, MILHAUSER, GIERKE, LEFE

- Page 1222:

208 TOMLIN, MILHAUSER, GIERKE, LEFE

- Page 1226:

210 TOMLIN, MILHAUSER, GIERKE, LEFE

- Page 1230:

22 Avon Products Inc. — 2009 Roch

- Page 1234: 214 ROCHELLE R. BRUNSON AND MARLENE

- Page 1238: 216 ROCHELLE R. BRUNSON AND MARLENE

- Page 1242: 218 ROCHELLE R. BRUNSON AND MARLENE

- Page 1246: 23 Molson Coors — 2009 Amit J. Sh

- Page 1250: 222 AMIT J. SHAH According to Molso

- Page 1254: 224 AMIT J. SHAH EXHIBIT 2 Molson C

- Page 1258: 226 AMIT J. SHAH EXHIBIT 3 Molson C

- Page 1262: 228 AMIT J. SHAH aims to help paren

- Page 1266: 230 AMIT J. SHAH liquors can take s

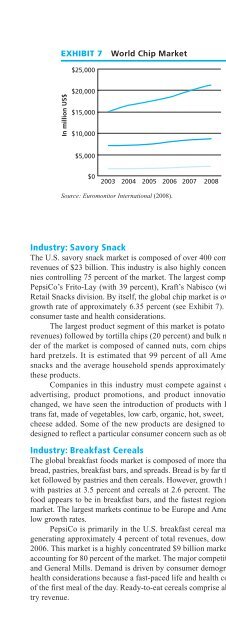

- Page 1270: 24 PepsiCo — 2009 John and Sherry

- Page 1274: 234 JOHN AND SHERRY ROSS EXHIBIT 1

- Page 1278: 236 JOHN AND SHERRY ROSS EXHIBIT 3

- Page 1282: 238 JOHN AND SHERRY ROSS Our approa

- Page 1288: Coca-Cola will continue to concentr

- Page 1292: 25 Pfizer, Inc. — 2009 Vijaya Nar

- Page 1296: EXHIBIT 1 Revenues by Key Products

- Page 1300: Pfizer’s consolidated Balance She

- Page 1304: EXHIBIT 7 Overview of Direct Compet

- Page 1308: number should reach $265 billion in

- Page 1312: EXHIBIT 1 Merck’s Recent Acquisit

- Page 1316: EXHIBIT 3 Merck’s Sales by Produc

- Page 1320: Industry Issues, Facts, and Figures

- Page 1324: prescriptions. Because the price of

- Page 1328: 27 Nike, Inc. — 2010 1 Randy Harr

- Page 1332: The company has set a strategic goa

- Page 1336:

EXHIBIT 5 Nike’s Income Before Ta

- Page 1340:

Nike Customers and Price Points Bec

- Page 1344:

Competition Competition in the athl

- Page 1348:

eliminate quotas and tariff barrier

- Page 1352:

The company acquired FrogTrader to

- Page 1356:

CASE 28 • CALLAWAY GOLF COMPANY

- Page 1360:

Pacific PTY Ltd., Callaway Golf (Sh

- Page 1364:

3.5 percent for the first quarter o

- Page 1368:

public and private golf clubs are e

- Page 1372:

Standard Oil and created Standard o

- Page 1376:

EXHIBIT 3 Statement of Income (mill

- Page 1380:

Marketing Marketing in an energy co

- Page 1384:

company in the world in 2007. The 2