WSHPDR_2013_Final_Report-updated_version

WSHPDR_2013_Final_Report-updated_version

WSHPDR_2013_Final_Report-updated_version

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

4.3.5 Italy<br />

European Small Hydropower Association, Stream Map<br />

Key facts<br />

Population 61,261,254<br />

Area 301,340 km 2<br />

Climate<br />

Topography<br />

Rain<br />

pattern<br />

Predominantly Mediterranean;<br />

Alpine in far north; hot, dry in south<br />

Mostly rugged and mountainous;<br />

some plains, coastal lowland<br />

Mean annual rainfall varies from<br />

about 500 mm on the southeast<br />

coast and in Sicily and Sardinia, to<br />

over 2,000 mm, in the Alps and on<br />

some westerly slopes of the<br />

Apennines. 1<br />

Electricity sector overview<br />

In 2011, more than 86 per cent of electricity<br />

consumed in Italy was produced in the country<br />

(288,900 GWh) and 13.7 per cent (45,700 GWh) were<br />

imported (figure 1). 2<br />

Geothermal 1.57%<br />

Wind 2.89%<br />

PV 3.16%<br />

Imported Electricity 13.54%<br />

Hydro 14.13%<br />

Thermal<br />

64.70%<br />

0% 20% 40% 60% 80%<br />

Figure 1 Electricity generation in Italy<br />

Source: Terna 2<br />

The Authority for Electricity and Gas (AEEG) in Italy<br />

promotes the development of competition in the<br />

power market (Law n. 481/1995). Terna was created<br />

in 1999 as a separate company to own, develop and<br />

maintain more than 90 per cent of the National<br />

Electricity Transmission Network. Meanwhile<br />

management of the grid was entrusted to a public<br />

operator controlled by the Ministry of Finance called<br />

GRTN or Gestore della Rete di Trasmissione Nazionale<br />

(Independent System Operator Model). The electricity<br />

market was fully liberalized in 2007. 3<br />

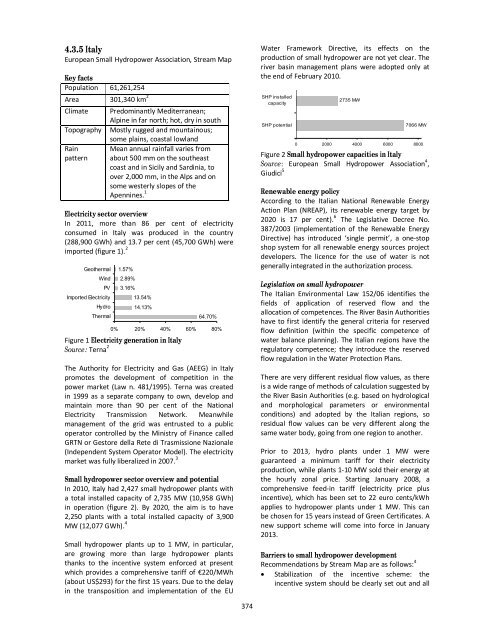

Small hydropower sector overview and potential<br />

In 2010, Italy had 2,427 small hydropower plants with<br />

a total installed capacity of 2,735 MW (10,958 GWh)<br />

in operation (figure 2). By 2020, the aim is to have<br />

2,250 plants with a total installed capacity of 3,900<br />

MW (12,077 GWh). 4<br />

Small hydropower plants up to 1 MW, in particular,<br />

are growing more than large hydropower plants<br />

thanks to the incentive system enforced at present<br />

which provides a comprehensive tariff of €220/MWh<br />

(about US$293) for the first 15 years. Due to the delay<br />

in the transposition and implementation of the EU<br />

Water Framework Directive, its effects on the<br />

production of small hydropower are not yet clear. The<br />

river basin management plans were adopted only at<br />

the end of February 2010.<br />

SHP installed<br />

capacity<br />

SHP potential<br />

2735 MW<br />

7066 MW<br />

0 2000 4000 6000 8000<br />

Figure 2 Small hydropower capacities in Italy<br />

Source: European Small Hydropower Association 4 ,<br />

Giudici 5<br />

Renewable energy policy<br />

According to the Italian National Renewable Energy<br />

Action Plan (NREAP), its renewable energy target by<br />

2020 is 17 per cent). 6 The Legislative Decree No.<br />

387/2003 (implementation of the Renewable Energy<br />

Directive) has introduced ‘single permit’, a one-stop<br />

shop system for all renewable energy sources project<br />

developers. The licence for the use of water is not<br />

generally integrated in the authorization process.<br />

Legislation on small hydropower<br />

The Italian Environmental Law 152/06 identifies the<br />

fields of application of reserved flow and the<br />

allocation of competences. The River Basin Authorities<br />

have to first identify the general criteria for reserved<br />

flow definition (within the specific competence of<br />

water balance planning). The Italian regions have the<br />

regulatory competence; they introduce the reserved<br />

flow regulation in the Water Protection Plans.<br />

There are very different residual flow values, as there<br />

is a wide range of methods of calculation suggested by<br />

the River Basin Authorities (e.g. based on hydrological<br />

and morphological parameters or environmental<br />

conditions) and adopted by the Italian regions, so<br />

residual flow values can be very different along the<br />

same water body, going from one region to another.<br />

Prior to <strong>2013</strong>, hydro plants under 1 MW were<br />

guaranteed a minimum tariff for their electricity<br />

production, while plants 1-10 MW sold their energy at<br />

the hourly zonal price. Starting January 2008, a<br />

comprehensive feed-in tariff (electricity price plus<br />

incentive), which has been set to 22 euro cents/kWh<br />

applies to hydropower plants under 1 MW. This can<br />

be chosen for 15 years instead of Green Certificates. A<br />

new support scheme will come into force in January<br />

<strong>2013</strong>.<br />

Barriers to small hydropower development<br />

Recommendations by Stream Map are as follows: 4<br />

Stabilization of the incentive scheme: the<br />

incentive system should be clearly set out and all<br />

374