- Page 4 and 5:

Contents FOREWORD (Jan Burnewicz)..

- Page 6 and 7:

9.4. Security of information.......

- Page 8 and 9:

20.3. Factors stimulating the devel

- Page 10 and 11:

great and has brought measurable ef

- Page 12 and 13:

The theory of innovation was introd

- Page 14 and 15:

According to Robert U. Ayres, who p

- Page 16 and 17:

tions may be of technological, orga

- Page 18 and 19:

1.2. Innovation features Innovation

- Page 20 and 21:

The sources of innovation embrace a

- Page 22 and 23:

Table 2. Innovation processes model

- Page 24 and 25:

of techniques. Strategic integratio

- Page 26 and 27:

32. Sudo³ S., Przedsiêbiorstwo pr

- Page 28 and 29:

land, attempts were made in the ear

- Page 30 and 31:

English 9 . As can be seen, the phr

- Page 32 and 33:

The European Union, being an area o

- Page 34 and 35:

tives of member states and associat

- Page 36 and 37:

- a direct result of research which

- Page 38 and 39:

is, in particular, the response to

- Page 40 and 41:

2.6. Bibliography 1. Blaug M., Teor

- Page 42 and 43:

stems from the economic policy 3 ,

- Page 44 and 45:

according to the linear innovation

- Page 46 and 47:

- the shaping and consolidation of

- Page 48 and 49:

Treaty of Amsterdam (“Research an

- Page 50 and 51:

Unfortunately, the first period of

- Page 52 and 53:

and technical subjects in several a

- Page 54 and 55:

Fig. 5), where growing competitiven

- Page 56 and 57:

Table 8. Innovation performance of

- Page 58 and 59:

0,700 0,600 0,500 0,400 0,300 0,200

- Page 60 and 61:

3.3. Polish innovation policy In Po

- Page 62 and 63:

lopment in the future, e.g. Turkey,

- Page 64 and 65:

1989 1990 1991 1992 1993 1994 1995

- Page 66 and 67:

- 6.4 billion euro to be provided b

- Page 68 and 69:

knowledge-based economy is the only

- Page 70 and 71:

- arising during business activity,

- Page 72 and 73:

- the use of advanced methods and t

- Page 74 and 75:

Chapter 4 A STUDY OF INNOVATIVE TRE

- Page 76 and 77:

In more recent centuries, though, t

- Page 78 and 79: economic development. In this diagn

- Page 80 and 81: placing private car use with public

- Page 82 and 83: The prime module of modern transpor

- Page 84 and 85: cialisation. 33 What this notion ac

- Page 86 and 87: era in technology, but had no comme

- Page 88 and 89: ecome a matter of honour for major

- Page 90 and 91: Fig. 14. A Toyota FT-EV at Detroit

- Page 92 and 93: Fuel Cell Vehicles - FCV) 75 are a

- Page 94 and 95: 94 - Toyota FCHV 81 is another of T

- Page 96 and 97: - Daimler Mercedes-Benz Citaro fuel

- Page 98 and 99: ange. The popularity of hybrid pass

- Page 100 and 101: X2000 116 , the Finnish S220 117 ,

- Page 102 and 103: •Commercial Turboprop Service •

- Page 105 and 106: dards 138 . Intense activity can al

- Page 107 and 108: - new technologies of winter inland

- Page 109 and 110: Fig.18.Vélib-abicycle rental syste

- Page 111 and 112: tional and EU authorities as well a

- Page 113 and 114: National Highway Research Laborator

- Page 115 and 116: innovation in terms of rail shape a

- Page 117 and 118: Infrastructural innovations aim at

- Page 119 and 120: 14. Konings R., ThijsR., Foldable C

- Page 121 and 122: tainable competitive advantage in t

- Page 123 and 124: ten years. Technological innovation

- Page 125 and 126: ticians, researchers and practition

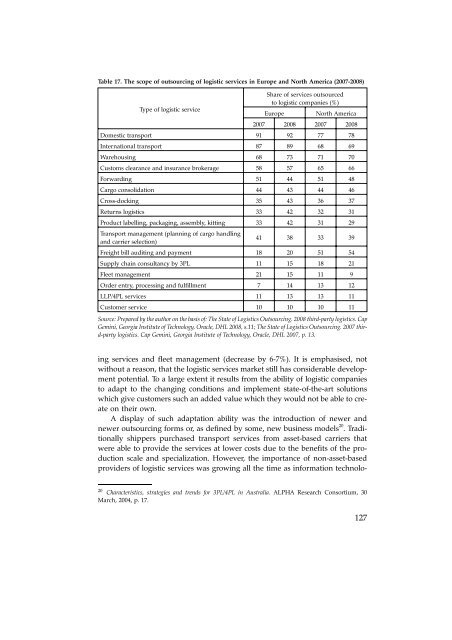

- Page 127: show that it is the time of respons

- Page 131 and 132: chain at a strategic level and focu

- Page 133 and 134: sary for company management and for

- Page 135 and 136: - Electronic Data Interchange (EDI)

- Page 137 and 138: effective solution of logistic task

- Page 139 and 140: - thermostat warehouse. Automation

- Page 141 and 142: assess the productivity of the rend

- Page 143 and 144: 15. Follow the leaders. Scoring hig

- Page 145 and 146: Chapter 6 NEW-GENERATION TRANSPORT

- Page 147 and 148: 1. The Panama Canal bridge 2. The B

- Page 149 and 150: Among intercontinental crossings is

- Page 151 and 152: Each human action has an effect on

- Page 153 and 154: monious effect remains ingrained de

- Page 155 and 156: Regrettably, the project was not co

- Page 157 and 158: 6.7. Bibliography 1. Brown D. J., M

- Page 159 and 160: The purpose of this chapter is not

- Page 161 and 162: 7 8 9 10 11 12 Improving road safet

- Page 163 and 164: Table 20. Satellite navigation in t

- Page 165 and 166: predict a traffic jam on a specific

- Page 167 and 168: of rail tracks, inspections and tes

- Page 169 and 170: 9. Roads. Galileo Application Sheet

- Page 171 and 172: transport modes, infrastructure and

- Page 173 and 174: - plan the routes and optimize park

- Page 175 and 176: ies. In modern logistics systems, t

- Page 177 and 178: Fig. 33. Option II of vehicle route

- Page 179 and 180:

Optimization of route selection dep

- Page 181 and 182:

Chapter 9 NEW INFORMATION TECHNOLOG

- Page 183 and 184:

uilding. The competitive advantage

- Page 185 and 186:

- systems for planning and optimiza

- Page 187 and 188:

and consist of defining information

- Page 189 and 190:

2. Naporowska E., Warunki rozwoju e

- Page 191 and 192:

10.2. Factors causing changes in ur

- Page 193 and 194:

10.3. Model description of modern u

- Page 195 and 196:

The French urban transport organiza

- Page 197 and 198:

petitiveness of urban transport wit

- Page 199 and 200:

a system of rewards and penalties b

- Page 201 and 202:

sales of tickets received on the ba

- Page 203 and 204:

Chapter 11 SUSTAINABLE URBAN MOBILI

- Page 205 and 206:

einstate the proper role of environ

- Page 207 and 208:

European cities had already been af

- Page 209 and 210:

limiting car use, especially in cit

- Page 211 and 212:

- support instruments for measures

- Page 213 and 214:

City-wide Campaigns Innovative dema

- Page 215 and 216:

ture, of consistent cycle-promoting

- Page 217 and 218:

should be treated preferentially in

- Page 219 and 220:

is that the bicycle is quite simply

- Page 221 and 222:

Fig. 40. Comparison of various tran

- Page 223 and 224:

struggle with inappropriate pavemen

- Page 225 and 226:

Bicycle racks Other amenities They

- Page 227 and 228:

Table 30. Comparison of percentage

- Page 229 and 230:

12.8. Bibliography 1. Cycling: the

- Page 231 and 232:

and using nuclear, solar, water or

- Page 233 and 234:

methods of performance enhancement

- Page 235 and 236:

Table 31. Timeline of Euro standard

- Page 237 and 238:

10. Smalko Z., Sznytko J., Kierunki

- Page 239 and 240:

Transport activity, a complementary

- Page 241 and 242:

sis for making them more dynamic. I

- Page 243 and 244:

The literature of the subject menti

- Page 245 and 246:

specific nature of new markets and

- Page 247 and 248:

In this context, the operation of T

- Page 249 and 250:

Chapter 15 FACTORS INFLUENCING MODA

- Page 251 and 252:

- to improve the understanding of u

- Page 253 and 254:

The fiscal function of the charges

- Page 255 and 256:

15.3. Examples of How Differentiate

- Page 257 and 258:

- increasing the accepted weight of

- Page 259 and 260:

Still, from a technological viewpoi

- Page 261 and 262:

At last, one notices that the natur

- Page 263 and 264:

operation it results from, whereas

- Page 265 and 266:

16.6. New qualitative preference of

- Page 267 and 268:

The importance of quality of servic

- Page 269 and 270:

Chapter 17 TRENDS IN WORLD SHIPPING

- Page 271 and 272:

17.2. World seaborne trade and the

- Page 273 and 274:

Table 37. World fleet size in the 1

- Page 275 and 276:

day in 2011, compared with 83.3 mil

- Page 277 and 278:

hicles at the end of 2005 to 168 ca

- Page 279 and 280:

ate of BSR countries is higher than

- Page 281 and 282:

In the BSR, as well as the entire E

- Page 283 and 284:

2005, the volume of cargo handled i

- Page 285 and 286:

Among the trends of the EU transpor

- Page 287 and 288:

enlarge loading capacity at minimum

- Page 289 and 290:

18.5. Port business diversification

- Page 291 and 292:

18.6. Relations with port cities, r

- Page 293 and 294:

Chapter 19 MODERN ENVIRONMENTAL MAN

- Page 295 and 296:

Green Paper on the Impact of Transp

- Page 297 and 298:

- new tasks have appeared in connec

- Page 299 and 300:

this area resulted in the Greening

- Page 301 and 302:

activities aimed at separating dema

- Page 303 and 304:

It is also worth noting that energy

- Page 305 and 306:

Table 41. The most likely growth sc

- Page 307 and 308:

Table 42. Towards sustainable trans

- Page 309 and 310:

such. The use of the existing infra

- Page 311 and 312:

Chapter 20 DEVELOPEMNT OF INTERNATI

- Page 313 and 314:

tional logistics strengthened, and

- Page 315 and 316:

Paradoxically, we can say that the

- Page 317 and 318:

their financial resources (by 2008)

- Page 319 and 320:

At present, there are 15 Euroregion

- Page 321 and 322:

4) international financial relation

- Page 323 and 324:

Where: F= number of trips between t

- Page 325 and 326:

6. Logistyka w internacjonalizacjio

- Page 327 and 328:

prastructure and logistics services

- Page 329 and 330:

In the 1980s, more factors appeared

- Page 331 and 332:

which plans to cover the whole coun

- Page 333 and 334:

and Eastern Europe, it is only a lo

- Page 335 and 336:

to open for market economy. It led

- Page 337 and 338:

used and where the full range of co

- Page 339 and 340:

of intralogistics (see Fig. 68). Th

- Page 341 and 342:

sulting in the creation of new of s

- Page 343 and 344:

changes refers mainly to these sect

- Page 345 and 346:

costs. Because of the “bypassing

- Page 347 and 348:

5. Bogaschewsky R., Globale Beschaf

- Page 349 and 350:

this theory, a natural course of de

- Page 351 and 352:

On the other hand, the company’s

- Page 353 and 354:

a basis, particularly the evaluatio

- Page 355 and 356:

The ‘list of risks’ method cons

- Page 357 and 358:

the success of this risk descriptio

- Page 359 and 360:

It must be stressed that what is at

- Page 361 and 362:

Partial formalization in the proces

- Page 363 and 364:

etween those types of investments c

- Page 365 and 366:

other sectors of the economy. Such

- Page 367 and 368:

Comparative analysis of innovative

- Page 369 and 370:

on presenting periodical payment in

- Page 371 and 372:

time) of a new solution that has no

- Page 373 and 374:

12. Pietrzyka B., Klasyfikacja prze

- Page 375 and 376:

activities more attractive (quads 1

- Page 377 and 378:

interdisciplinary, although individ

- Page 379 and 380:

tem and modal deficiencies of conte

- Page 381 and 382:

Hydrogen propulsion is becoming ano

- Page 383 and 384:

can be regarded as the most importa

- Page 385 and 386:

lift-sharing, also called car-pooli

- Page 387 and 388:

A large group of technologies, give

- Page 389 and 390:

Every human activity has an impact

- Page 391 and 392:

The most useful function of road ca

- Page 393 and 394:

a growing number of inhabitants liv

- Page 395 and 396:

nation-wide promotional campaigns a

- Page 397 and 398:

As for innovations aimed at using a

- Page 399 and 400:

of freight on a given route, shapin

- Page 401 and 402:

and development of ports as land-se

- Page 403 and 404:

of economy: they are high in consum

- Page 405 and 406:

than potential profits the innovati

- Page 407 and 408:

PODSUMOWANIE I WNIOSKI (Jan Burnewi

- Page 409 and 410:

nia od podstaw w wybranych regionac

- Page 411 and 412:

ski. Strategicznym (nadrzêdnym) ce

- Page 413 and 414:

struktorów samochodów elektryczny

- Page 415 and 416:

opracowan¹ z myœl¹ o ograniczeni

- Page 417 and 418:

acji lotniska i l¹dowiska. Wœród

- Page 419 and 420:

w¹tpliwych efektów wdra¿ania now

- Page 421 and 422:

œwiecie koncepcji i nowych rozwi¹

- Page 423 and 424:

nologie budownictwa infrastruktural

- Page 425 and 426:

TEN wpisany zosta³ projekt europej

- Page 427 and 428:

staw/ w ramach sieci dostaw (certyf

- Page 429 and 430:

nych), takich jak wprowadzanie ró

- Page 431 and 432:

obytu ludzie staj¹ siê coraz bard

- Page 433 and 434:

Trzy pierwsze typy procesów innowa

- Page 435 and 436:

który musi opracowywaæ nowatorski

- Page 437 and 438:

Przemiany technologiczne i innowacy

- Page 439 and 440:

ne uwidoczni³a siê ju¿ pod konie

- Page 441 and 442:

nia logistycznego, • stosowanie f

- Page 443 and 444:

Formalizacja oceny ryzyka w innowac

- Page 445 and 446:

List of tables Table 1. Innovation

- Page 447 and 448:

Table 50. Time horizon of risk fact

- Page 449 and 450:

Fig. 24. Strategic crossings within

- Page 451 and 452:

About Authors El¿bieta Adamowicz:

- Page 453:

Michel Savy: Professor in the Unive