ASi" kUCTURE FlOR DEVELOPMENT

ASi" kUCTURE FlOR DEVELOPMENT

ASi" kUCTURE FlOR DEVELOPMENT

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

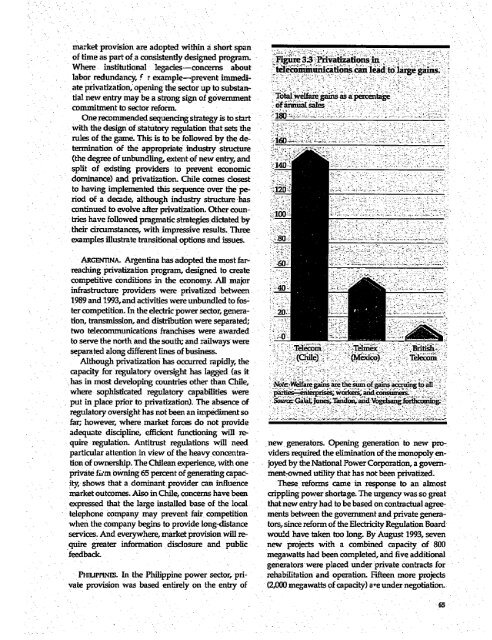

market provision are adopted witiin a short span<br />

of time as part of a consistently designed program. Fig- as,ji ta ''<br />

Where institutional legacies-concerns about - eommaiocleadto large g<br />

labor redundancy, F r example-prevent immediate<br />

privatization,' opening the sector up to substan- C<br />

tial new entry may be a strong sign of goverrunent ; T_otal welf ,gans as,a percen tag<br />

commitment to sector reform.<br />

o,fannual sales<br />

One recommended sequencing strategy is to start 180<br />

with the design of statutory regulation that sets the<br />

rules of the game. This is to be followed by the de- 160<br />

termination of the appropriate industry structure<br />

(the degree of unbundling, extent of new entry, and<br />

split of existing providers to prevent economic<br />

dominance) and privatization. Chile comes closest<br />

to having implemented this sequence over the pe- 120<br />

riod of a decade, although industry structure has<br />

continued to evolve after privatization. Other countries<br />

have folowed pragmatic strategies, dictated by<br />

their crumstances, with impressive results.. Three<br />

examples illustrate transional options and issues. 80<br />

ARGENTINA. Argentina has adopted the most farreaching<br />

privatization program, designed to create<br />

competitive conditions in the economy. -A major<br />

infrastructure providers were privatized between<br />

1989 and 1993, and activities were unbundled to foster<br />

competition. In the electric power sector, genera- 20<br />

dion, transmission, and distribution were separated;<br />

two telecommunications franchises were awarded<br />

to serve the north and the souti; and railways were<br />

separated along different lines of business. Tdecom T Br:T3sh<br />

Although privaization has occurred rapidly, the (Onle) -xi) Telecom<br />

capacity for regulatory oversight has lagged (as it<br />

has in most developing countries other than Chile, oe Wfre gans are the smof gasaing to<br />

where sophisticated regulatory capabilities were p p nsiLir, and-consumers:<br />

put in place prior to privatization). The absence of S GJ 4Oad lnfo<br />

regulatory oversight has not been an impediment so 4-<br />

far;, lowever, where market forces do not provide<br />

adequate discipline, efficient functioning will require<br />

regulation. Antitrust regulations will need new generators. Opening generation to new proparticular<br />

attention in view of the heavy concentra- viders required the elimination of the monopoly ention<br />

of ownership. The Chilean experience, with one joyed by the National Power Corporation, a governprivate<br />

firn owning 65 percent of generating capac- ment-owned utility that has not been privatized<br />

ity, shows that a dominant provider can influence These reforms came in response to an almost<br />

market outcomes. Also in Chile, concerns have been crippling power shortage. The urgency was so great<br />

expressed that the large installed base of the local that new entry had to be based on contractual agreetelephone<br />

company may prevent fair competition ments between the govermnent and private generawhlen<br />

the company begins to provide long-distance tors, since reform of the Electricity Regulation Board<br />

services. And everywhere, market provision will re- would have taken too long. By August 1993, seven<br />

quire greater information disclosure and public new projects with a combined capacity of 800<br />

feedback-<br />

megawatts had been completed, and five additional<br />

generators were placed under private contracts for<br />

PHIUPPINES. In the Philippine power sector, pri- rehabilitation and operation. Fifteen more projects<br />

vate provision was based entirely on the entry of (2,000 megawatts of capacity) are under negotiation.<br />

.65