sectoral economic costs and benefits of ghg mitigation - IPCC

sectoral economic costs and benefits of ghg mitigation - IPCC

sectoral economic costs and benefits of ghg mitigation - IPCC

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Fossil Fuels<br />

A second issue that must also be considered in this discussion is whether, even absent climate<br />

<strong>mitigation</strong> policies, current energy <strong>and</strong> energy related activities would be unchanged. This is a<br />

question that is seldom raised in the context <strong>of</strong> examining impacts on fossil fuel exporters –<br />

although, in theory, the “business-as-usual” case defines the trend that analysts think may obtain<br />

without climate policies. Here too, some assessment <strong>of</strong> possible energy trends suggests that<br />

rethinking may be required to accurately assess the “reference” case against which any impacts<br />

might need to be measured. For example, in coal-based power generation, efforts to reduce<br />

emissions <strong>of</strong> sulfur, particulates <strong>and</strong> oxides <strong>of</strong> nitrogen are already having a significant effect on<br />

coal use <strong>and</strong> operating <strong>costs</strong>; will future power be produced without coal, or will technology<br />

evolve to eliminate emissions <strong>of</strong> these criteria pollutants?<br />

In both the discussion <strong>of</strong> policy choices <strong>and</strong> the “no-climate-policy” case, there will clearly be<br />

different implications for each <strong>of</strong> the fossil fuels. For example, coal use in the future can be<br />

expected to follow a different path than oil or gas whether climate <strong>mitigation</strong> measures are taken<br />

or not. To help draw out these fuel-specific issues, the discussion <strong>of</strong> these questions in Section 2<br />

below has thus been divided, <strong>and</strong> looks separately at coal, <strong>and</strong> at oil & gas.<br />

Finally, a number <strong>of</strong> countries have already begun to face the prospects <strong>of</strong> reduced revenues from<br />

export <strong>of</strong> fossil fuels – <strong>and</strong> have begun to take actions to <strong>of</strong>fset some <strong>of</strong> the possible impacts <strong>of</strong><br />

these declining revenues. Considering their situations may provide a useful model that could<br />

apply more broadly should global climate <strong>mitigation</strong> efforts indeed prove detrimental to fossil<br />

fuel exporting countries. In addition, some <strong>of</strong> the <strong>mitigation</strong> policies that countries might adopt<br />

could be less “damaging” than others. These issues are broadly addressed in Part 3 <strong>of</strong> this paper.<br />

2 Fossil Fuels: Supply, Dem<strong>and</strong> <strong>and</strong> Emission Mitigation Options<br />

Approximately 85% <strong>of</strong> the world’s emissions <strong>of</strong> greenhouse gases come from the energy sector,<br />

<strong>and</strong> within this sector, almost all the emissions are from the combustion <strong>of</strong> fossil fuels. The 3,387<br />

million metric tons <strong>of</strong> crude oil, 2,296,152 million cubic meters <strong>of</strong> gas, <strong>and</strong> 3,796 million tons <strong>of</strong><br />

coal burned in 1997 accounted for 43%, 19% <strong>and</strong> 38% percent respectively, <strong>of</strong> the contribution<br />

to global carbon dioxide emissions.<br />

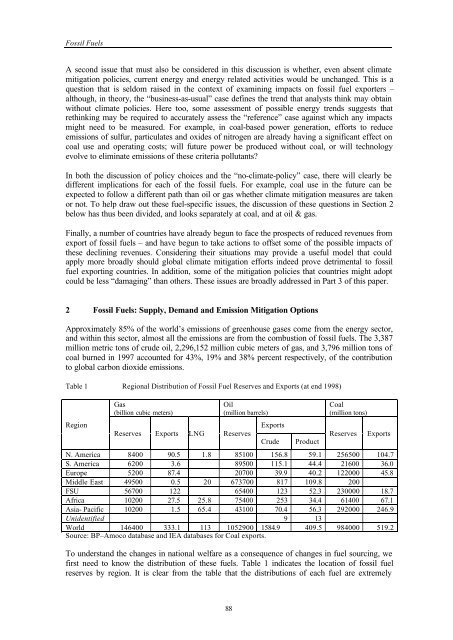

Table 1 Regional Distribution <strong>of</strong> Fossil Fuel Reserves <strong>and</strong> Exports (at end 1998)<br />

Region<br />

Gas<br />

(billion cubic meters)<br />

Oil<br />

(million barrels)<br />

Reserves Exports LNG Reserves<br />

Exports<br />

Crude<br />

Product<br />

Coal<br />

(million tons)<br />

Reserves<br />

Exports<br />

N. America 8400 90.5 1.8 85100 156.8 59.1 256500 104.7<br />

S. America 6200 3.6 89500 115.1 44.4 21600 36.0<br />

Europe 5200 87.4 20700 39.9 40.2 122000 45.8<br />

Middle East 49500 0.5 20 673700 817 109.8 200<br />

FSU 56700 122 65400 123 52.3 230000 18.7<br />

Africa 10200 27.5 25.8 75400 253 34.4 61400 67.1<br />

Asia- Pacific 10200 1.5 65.4 43100 70.4 56.3 292000 246.9<br />

Unidentified 9 13<br />

World 146400 333.1 113 1052900 1584.9 409.5 984000 519.2<br />

Source: BP–Amoco database <strong>and</strong> IEA databases for Coal exports.<br />

To underst<strong>and</strong> the changes in national welfare as a consequence <strong>of</strong> changes in fuel sourcing, we<br />

first need to know the distribution <strong>of</strong> these fuels. Table 1 indicates the location <strong>of</strong> fossil fuel<br />

reserves by region. It is clear from the table that the distributions <strong>of</strong> each fuel are extremely<br />

88