- Page 1:

2012 COMMISSION O N T H E REFORM O

- Page 4 and 5:

For electronic copies of this docum

- Page 6 and 7:

Chapter 4: Making Transformation Wo

- Page 8 and 9:

Chapter 9: Employment and Training

- Page 10 and 11:

Chapter 18: Revenue Integrity Incre

- Page 12 and 13:

This context lifts the task ahead w

- Page 14 and 15:

Action must begin very soon. The de

- Page 16 and 17:

xii Dominic Giroux, Commiss

- Page 18 and 19:

Photo Credit: Jovan Matic xiv Carol

- Page 20 and 21:

First, we assessed the 2011 Budget

- Page 22 and 23:

How did we get to this point? For m

- Page 24 and 25:

6 TABLE 1. Three Views of the Outlo

- Page 26 and 27:

This permits post-secondary educati

- Page 28 and 29:

How does our scenario for the perio

- Page 30 and 31:

The “don’ts” are proposals th

- Page 32 and 33:

Several measures would strengthen t

- Page 34 and 35:

Health care is the Ontario governme

- Page 36 and 37:

There are inefficiencies in the hea

- Page 38 and 39:

20 Service Delivery � Mostly publ

- Page 40 and 41:

Our first recommendation is that th

- Page 42 and 43:

Evidence should drive policy. Medic

- Page 44 and 45:

One potential way to reduce overall

- Page 46 and 47:

Elementary and Secondary Education

- Page 48 and 49:

Non-Teaching Staff: Since 2002-03,

- Page 50 and 51:

Delivering Services More Efficientl

- Page 52 and 53:

Simply maintaining the status quo r

- Page 54 and 55:

� Mandate agreements should inclu

- Page 56 and 57:

Benefit programs are delivered thro

- Page 58 and 59:

Child Welfare: In this case, as wit

- Page 60 and 61:

With so many services provided by s

- Page 62 and 63:

Over the past decade, the Ontario g

- Page 64 and 65:

Urban transportation is a particula

- Page 66 and 67:

Environment and Natural Resources R

- Page 68 and 69:

� Aging infrastructure is deterio

- Page 70 and 71:

Labour Relations and Compensation T

- Page 72 and 73:

Leaders in the OPS and BPS should b

- Page 74 and 75:

In a number of areas, efficiencies

- Page 76 and 77:

Revenue Integrity Across a range of

- Page 78 and 79:

Contraband tobacco is another issue

- Page 80 and 81:

Risks Posed by the Federal Governme

- Page 82 and 83:

� Long-term health costs outstrip

- Page 84 and 85:

Immigration settlement and integrat

- Page 87 and 88:

Chapter 1: The Need for Strong Fisc

- Page 89 and 90:

The Budget Scenario Chapter 1: The

- Page 91 and 92:

Chapter 1: The Need for Strong Fisc

- Page 93 and 94:

Chapter 1: The Need for Strong Fisc

- Page 95 and 96:

Chapter 1: The Need for Strong Fisc

- Page 97 and 98:

Chapter 1: The Need for Strong Fisc

- Page 99 and 100:

Chapter 1: The Need for Strong Fisc

- Page 101 and 102:

80 60 40 20 0 Rest of Canada Ontari

- Page 103 and 104:

Chapter 1: The Need for Strong Fisc

- Page 105 and 106:

Chapter 1: The Need for Strong Fisc

- Page 107 and 108:

Chapter 1: The Need for Strong Fisc

- Page 109 and 110:

Revenue Implications Chapter 1: The

- Page 111 and 112:

Chapter 1: The Need for Strong Fisc

- Page 113 and 114:

Chapter 1: The Need for Strong Fisc

- Page 115 and 116:

Chapter 1: The Need for Strong Fisc

- Page 117 and 118:

Chapter 1: The Need for Strong Fisc

- Page 119 and 120:

TABLE 1.1 Three Views of the Outloo

- Page 121 and 122:

Chapter 1: The Need for Strong Fisc

- Page 123 and 124:

Chapter 1: The Need for Strong Fisc

- Page 125 and 126:

Conclusion Chapter 1: The Need for

- Page 127 and 128:

Chapter 2: The Fiscal Challenge in

- Page 129 and 130:

Chapter 2: The Fiscal Challenge in

- Page 131 and 132:

Chapter 2: The Fiscal Challenge in

- Page 133 and 134:

Chapter 2: The Fiscal Challenge in

- Page 135 and 136:

Chapter 2: The Fiscal Challenge in

- Page 137 and 138:

Chapter 2: The Fiscal Challenge in

- Page 139 and 140:

The Challenge Chapter 2: The Fiscal

- Page 141 and 142:

Chapter 3: Our Mandate and Approach

- Page 143 and 144:

Chapter 3: Our Mandate and Approach

- Page 145 and 146:

Chapter 3: Our Mandate and Approach

- Page 147 and 148:

Chapter 3: Our Mandate and Approach

- Page 149 and 150:

Chapter 3: Our Mandate and Approach

- Page 151 and 152:

Chapter 3: Our Mandate and Approach

- Page 153 and 154:

Chapter 4: Making Transformation Wo

- Page 155 and 156:

Chapter 4: Making Transformation Wo

- Page 157 and 158:

Chapter 4: Making Transformation Wo

- Page 159 and 160:

Chapter 4: Making Transformation Wo

- Page 161 and 162:

Chapter 5: Health Chapter 5: Health

- Page 163 and 164:

Chapter 5: Health Indeed, quality a

- Page 165 and 166:

The Cost: Now and Ahead Chapter 5:

- Page 167 and 168:

Is the Health Care System Sustainab

- Page 169 and 170:

Chapter 5: Health In Ontario, a few

- Page 171 and 172:

Chapter 5: Health Case Study #1: A

- Page 173 and 174:

Chapter 5: Health Canada’s health

- Page 175 and 176:

Canada falls short on many measures

- Page 177 and 178:

There are inefficiencies in the hea

- Page 179 and 180:

Chapter 5: Health A broader perspec

- Page 181 and 182:

Chapter 5: Health However, this is

- Page 183 and 184:

Mental health and addiction issues

- Page 185 and 186:

Chapter 5: Health Today, however, t

- Page 187 and 188:

Service Delivery Chapter 5: Health

- Page 189 and 190:

Chapter 5: Health Medical schools p

- Page 191 and 192:

Chapter 5: Health There is much to

- Page 193 and 194:

Recommendation 5-2: Evaluate all pr

- Page 195 and 196:

Chapter 5: Health Several key princ

- Page 197 and 198:

Chapter 5: Health There are more th

- Page 199 and 200:

Optimize Human Resources Capacity C

- Page 201 and 202:

Chapter 5: Health The LHINs should

- Page 203 and 204:

Chapter 5: Health Recommendation 5-

- Page 205 and 206:

Chapter 5: Health Despite variation

- Page 207 and 208:

Chapter 5: Health Recommendation 5-

- Page 209 and 210:

Chapter 5: Health The ministry shou

- Page 211 and 212:

Chapter 5: Health � An “assess

- Page 213 and 214:

Chapter 5: Health Recommendation 5-

- Page 215 and 216:

Chapter 5: Health The Commi

- Page 217 and 218:

Cost Efficiencies Chapter 5: Health

- Page 219 and 220:

Chapter 5: Health The stakeholders

- Page 221 and 222:

Chapter 6: Elementary and Secondary

- Page 223 and 224:

Chapter 6: Elementary and Secondary

- Page 225 and 226:

Chapter 6: Elementary and Secondary

- Page 227 and 228:

Chapter 6: Elementary and Secondary

- Page 229 and 230:

Chapter 6: Elementary and Secondary

- Page 231 and 232:

Affordability of the Full-Day Kinde

- Page 233 and 234:

Class Sizes Chapter 6: Elementary a

- Page 235 and 236:

Chapter 6: Elementary and Secondary

- Page 237 and 238:

Chapter 6: Elementary and Secondary

- Page 239 and 240:

Chapter 6: Elementary and Secondary

- Page 241 and 242:

Chapter 6: Elementary and Secondary

- Page 243 and 244:

Chapter 6: Elementary and Secondary

- Page 245 and 246:

Reform of Provincial Schools Chapte

- Page 247 and 248:

Chapter 6: Elementary and Secondary

- Page 249 and 250:

Chapter 6: Elementary and Secondary

- Page 251 and 252:

Chapter 6: Elementary and Secondary

- Page 253 and 254:

Chapter 6: Elementary and Secondary

- Page 255 and 256:

Chapter 6: Elementary and Secondary

- Page 257 and 258:

Chapter 7: Post-Secondary Education

- Page 259 and 260:

Need for Clear Objectives Chapter 7

- Page 261 and 262:

Chapter 7: Post-Secondary Education

- Page 263 and 264:

9,000 8,000 7,000 6,000 5,000 Unive

- Page 265 and 266:

Chapter 7: Post-Secondary Education

- Page 267 and 268:

Chapter 7: Post-Secondary Education

- Page 269 and 270:

Chapter 7: Post-Secondary Education

- Page 271 and 272: Chapter 7: Post-Secondary Education

- Page 273 and 274: Chapter 7: Post-Secondary Education

- Page 275 and 276: Chapter 7: Post-Secondary Education

- Page 277 and 278: Chapter 8: Social Programs Chapter

- Page 279 and 280: The Challenge Chapter 8: Social Pro

- Page 281 and 282: Chapter 8: Social Programs Recommen

- Page 283 and 284: Chapter 8: Social Programs In the a

- Page 285 and 286: Initial Assessment Chapter 8: Socia

- Page 287 and 288: Chapter 8: Social Programs To quali

- Page 289 and 290: Chapter 8: Social Programs While th

- Page 291 and 292: Youth Justice Chapter 8: Social Pro

- Page 293 and 294: General Approach � Transaction fo

- Page 295 and 296: Chapter 9: Employment and Training

- Page 297 and 298: Employment and Training Services Pr

- Page 299 and 300: Chapter 9: Employment and Training

- Page 301 and 302: Chapter 9: Employment and Training

- Page 303 and 304: Chapter 9: Employment and Training

- Page 305 and 306: Chapter 10: Immigration The Economi

- Page 307 and 308: TABLE 10.1 Permanent Residents Admi

- Page 309 and 310: Chapter 10: Immigration Recommendat

- Page 311 and 312: Other Integration Issues Chapter 10

- Page 313 and 314: TABLE 10.4 Integration Program Fund

- Page 315 and 316: Chapter 10: Immigration A new COIA

- Page 317 and 318: Chapter 11: Business Support Chapte

- Page 319 and 320: � Investment in post-secondary ed

- Page 321: TABLE 11.1 Total Business Tax Relie

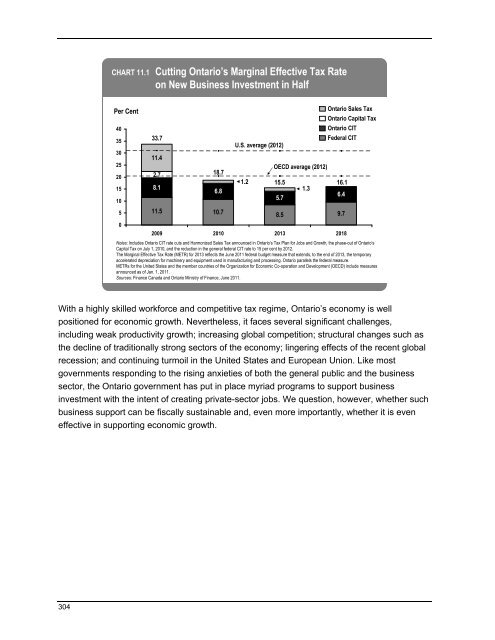

- Page 325 and 326: Chapter 11: Business Support The pr

- Page 327 and 328: Chapter 11: Business Support An Ill

- Page 329 and 330: Chapter 11: Business Support The pr

- Page 331 and 332: Chapter 11: Business Support To fun

- Page 333 and 334: Chapter 11: Business Support Tax ex

- Page 335 and 336: Chapter 11: Business Support For ex

- Page 337 and 338: Appendix 11.1 List of Business Supp

- Page 339 and 340: Chapter 12: Infrastructure, Real Es

- Page 341 and 342: Transportation Chapter 12: Infrastr

- Page 343 and 344: Chapter 12: Infrastructure, Real Es

- Page 345 and 346: Chapter 12: Infrastructure, Real Es

- Page 347 and 348: Chapter 12: Infrastructure, Real Es

- Page 349 and 350: Chapter 12: Infrastructure, Real Es

- Page 351 and 352: Chapter 12: Infrastructure, Real Es

- Page 353 and 354: Chapter 13: Environment and Natural

- Page 355 and 356: Chapter 13: Environment and Natural

- Page 357 and 358: Reform the approvals process Chapte

- Page 359 and 360: Chapter 13: Environment and Natural

- Page 361 and 362: Chapter 13: Environment and Natural

- Page 363 and 364: Ring of Fire Chapter 13: Environmen

- Page 365 and 366: Chapter 14: Justice Sector 2010-11

- Page 367 and 368: Recent Expenditures Chapter 14: Jus

- Page 369 and 370: Chapter 14: Justice Sector Public E

- Page 371 and 372: Chapter 14: Justice Sector Continuo

- Page 373 and 374:

Chapter 14: Justice Sector Building

- Page 375 and 376:

Efficiencies Clustering OPS Adjudic

- Page 377 and 378:

Chapter 14: Justice Sector Analysis

- Page 379 and 380:

Chapter 14: Justice Sector Recommen

- Page 381 and 382:

Chapter 15: Labour Relations and Co

- Page 383 and 384:

Chapter 15: Labour Relations and Co

- Page 385 and 386:

Chapter 15: Labour Relations and Co

- Page 387 and 388:

A Balanced, Effective and Transpare

- Page 389 and 390:

Chapter 15: Labour Relations and Co

- Page 391 and 392:

Chapter 15: Labour Relations and Co

- Page 393 and 394:

Chapter 15: Labour Relations and Co

- Page 395 and 396:

Chapter 15: Labour Relations and Co

- Page 397 and 398:

Chapter 15: Labour Relations and Co

- Page 399 and 400:

Chapter 15: Labour Relations and Co

- Page 401 and 402:

Chapter 16: Operating and Back-Offi

- Page 403 and 404:

Chapter 16: Operating and Back-Offi

- Page 405 and 406:

ServiceOntario Transformation Chapt

- Page 407 and 408:

Chapter 16: Operating and Back-Offi

- Page 409 and 410:

Chapter 16: Operating and Back-Offi

- Page 411 and 412:

Chapter 16: Operating and Back-Offi

- Page 413 and 414:

Chapter 16: Operating and Back-Offi

- Page 415 and 416:

I&IT Transformation Chapter 16: Ope

- Page 417 and 418:

Back-Office Consolidation Chapter 1

- Page 419 and 420:

Chapter 16: Operating and Back-Offi

- Page 421 and 422:

Chapter 17: Government Business Ent

- Page 423 and 424:

Chapter 17: Government Business Ent

- Page 425 and 426:

Chapter 17: Government Business Ent

- Page 427 and 428:

Chapter 17: Government Business Ent

- Page 429 and 430:

Chapter 18: Revenue Integrity Chapt

- Page 431 and 432:

Chapter 18: Revenue Integrity Stati

- Page 433 and 434:

Uncollected Fines Chapter 18: Reven

- Page 435 and 436:

Chapter 18: Revenue Integrity The M

- Page 437 and 438:

Tax Revenue Chapter 18: Revenue Int

- Page 439 and 440:

CHART 18.2 Assessment and Tax Growt

- Page 441 and 442:

Chapter 18: Revenue Integrity The c

- Page 443 and 444:

Chapter 18: Revenue Integrity The t

- Page 445 and 446:

Chapter 18: Revenue Integrity Appen

- Page 447 and 448:

Chapter 19: Liability Management In

- Page 449 and 450:

Chapter 19: Liability Management To

- Page 451 and 452:

Chapter 19: Liability Management Th

- Page 453 and 454:

Chapter 19: Liability Management Bo

- Page 455 and 456:

TABLE 19.2 Historical and Projected

- Page 457 and 458:

Chapter 19: Liability Management Re

- Page 459 and 460:

Chapter 19: Liability Management Re

- Page 461 and 462:

Social Housing Chapter 19: Liabilit

- Page 463 and 464:

Chapter 19: Liability Management Fo

- Page 465 and 466:

Chapter 19: Liability Management Fo

- Page 467 and 468:

Chapter 20: Intergovernmental Relat

- Page 469 and 470:

CHART 20.1 Ontario’s Share of Fed

- Page 471 and 472:

CHART 20.3 Ontario’s Fiscal Gap 1

- Page 473 and 474:

Chapter 20: Intergovernmental Relat

- Page 475 and 476:

Potential Federal Impacts on Ontari

- Page 477 and 478:

Long-Term Health Costs Likely Outpa

- Page 479 and 480:

TABLE 20.2 Selected Examples of Tra

- Page 481 and 482:

CHART 20.7 2011-12 Equalization Ent

- Page 483 and 484:

Canada Social Transfer Chapter 20:

- Page 485 and 486:

Chart 20.10 Employment Outcomes for

- Page 487 and 488:

Green Energy Chapter 20: Intergover

- Page 489 and 490:

Chapter 20: Intergovernmental Relat

- Page 491 and 492:

Chapter 20: Intergovernmental Relat

- Page 493 and 494:

Environmental Protection and Regula

- Page 495 and 496:

CHART 20.11 2009 Municipal Revenues

- Page 497 and 498:

Infrastructure, Real Estate and Ele

- Page 499 and 500:

Chapter 20: Intergovernmental Relat

- Page 501 and 502:

Chapter 20: Intergovernmental Relat

- Page 503 and 504:

Chapter 20: Intergovernmental Relat

- Page 505 and 506:

Appendix 1: Commission</str

- Page 507 and 508:

Chapter 1: The Need for Strong Fisc

- Page 509 and 510:

Appendix: Commission</stron

- Page 511 and 512:

Appendix: Commission</stron

- Page 513 and 514:

Appendix: Commission</stron

- Page 515 and 516:

Appendix: Commission</stron

- Page 517 and 518:

Appendix: Commission</stron

- Page 519 and 520:

Appendix: Commission</stron

- Page 521 and 522:

Appendix: Commission</stron

- Page 523 and 524:

Appendix: Commission</stron

- Page 525 and 526:

Appendix: Commission</stron

- Page 527 and 528:

Appendix: Commission</stron

- Page 529 and 530:

Chapter 7: Post-Secondary Education

- Page 531 and 532:

Appendix: Commission</stron

- Page 533 and 534:

Recommendation 8-9: Advocate for fe

- Page 535 and 536:

Chapter 9: Employment and Training

- Page 537 and 538:

Chapter 11: Business Support Append

- Page 539 and 540:

Chapter 12: Infrastructure, Real Es

- Page 541 and 542:

Chapter 13: Environment and Natural

- Page 543 and 544:

Chapter 15: Labour Relations and Co

- Page 545 and 546:

Chapter 16: Operating and Back-Offi

- Page 547 and 548:

Chapter 17: Government Business Ent

- Page 549 and 550:

Chapter 18: Revenue Integrity Appen

- Page 551 and 552:

Appendix: Commission</stron

- Page 553 and 554:

Appendix: Commission</stron

- Page 555 and 556:

Appendix 2: List of Acronyms ABCs a

- Page 557 and 558:

FIT feed-in tariff FSCO Financial S

- Page 559 and 560:

MTCU Ministry of Training, Colleges

- Page 561 and 562:

REA Renewable Energy Approval RFP r

![Demande d'inscription en vertu de l'IFTA - IFTA 401 [ PDF - 795 KO ]](https://img.yumpu.com/15864716/1/190x245/demande-dinscription-en-vertu-de-lifta-ifta-401-pdf-795-ko-.jpg?quality=85)