Comparison between U.S. GAAP and International ... - Grant Thornton

Comparison between U.S. GAAP and International ... - Grant Thornton

Comparison between U.S. GAAP and International ... - Grant Thornton

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Comparison</strong> <strong>between</strong> U.S. <strong>GAAP</strong> <strong>and</strong> <strong>International</strong> Financial Reporting St<strong>and</strong>ards 33<br />

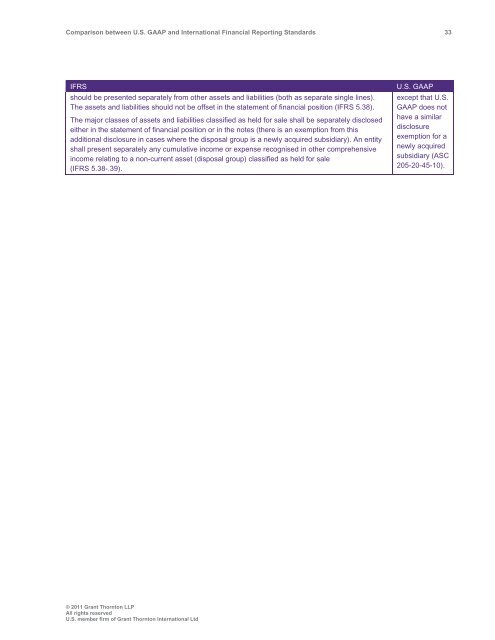

IFRS<br />

should be presented separately from other assets <strong>and</strong> liabilities (both as separate single lines).<br />

The assets <strong>and</strong> liabilities should not be offset in the statement of financial position (IFRS 5.38).<br />

The major classes of assets <strong>and</strong> liabilities classified as held for sale shall be separately disclosed<br />

either in the statement of financial position or in the notes (there is an exemption from this<br />

additional disclosure in cases where the disposal group is a newly acquired subsidiary). An entity<br />

shall present separately any cumulative income or expense recognised in other comprehensive<br />

income relating to a non-current asset (disposal group) classified as held for sale<br />

(IFRS 5.38-.39).<br />

U.S. <strong>GAAP</strong><br />

except that U.S.<br />

<strong>GAAP</strong> does not<br />

have a similar<br />

disclosure<br />

exemption for a<br />

newly acquired<br />

subsidiary (ASC<br />

205-20-45-10).<br />

© 2011 <strong>Grant</strong> <strong>Thornton</strong> LLP<br />

All rights reserved<br />

U.S. member firm of <strong>Grant</strong> <strong>Thornton</strong> <strong>International</strong> Ltd