- Page 1 and 2:

General Relief Policy USER INFORMAT

- Page 3 and 4:

GR 40-100 DETERMINATION OF ELIGIBIL

- Page 5 and 6:

GR 40-110.2 GR 40-110.3 Release of

- Page 7 and 8:

GR 40-120.32 Compliance with Treatm

- Page 9 and 10:

full-time and expects to complete s

- Page 11 and 12:

person’s case EXCEPT as exempt in

- Page 13 and 14:

of grant. All pregnant women are co

- Page 15 and 16:

Supervised Release eligible for GR?

- Page 17 and 18:

GR 40-102 - Cash Assistance Program

- Page 19 and 20:

The Worker is responsible for ensur

- Page 21 and 22:

Complaint Procedures Denial/Penalti

- Page 23 and 24:

sanctionable occurrence within the

- Page 25 and 26:

A disabled 18-year old living with

- Page 27 and 28:

When a pregnant individual reaches

- Page 29 and 30:

Refer to GR 44-402 for details. GR

- Page 31 and 32:

The SAWS 2A, Rights and Responsibil

- Page 33 and 34:

esponsibilities and provided with i

- Page 35 and 36:

Orientation Appointment letter (a M

- Page 37 and 38:

determined mentally disabled (NSA)

- Page 39 and 40:

Indian Tribal Enrollment Card and/o

- Page 41 and 42:

GR 40-111.6 - PA 230 Required GR 40

- Page 43 and 44:

are no restrictions on the number o

- Page 45 and 46:

All individuals, including minor ch

- Page 47 and 48:

(and SW-434, if applicable), I-95A,

- Page 49 and 50:

The individual and DPSS have been u

- Page 51 and 52:

GR 40-117 - Medical Benefits GR 40-

- Page 53 and 54:

Yes, during intake and, if approved

- Page 55 and 56:

treatment 20 hours per week meets t

- Page 57 and 58:

As with employable sanctions, all i

- Page 59 and 60:

Appointment GR 40-120.25 - Assessme

- Page 61 and 62:

progress. The assessment center is

- Page 63 and 64:

Ensuring the DHS’ Contract Progra

- Page 65 and 66:

GR 40-121.2 - Time Limit Informatio

- Page 67 and 68:

The termination is rescinded effect

- Page 69 and 70:

Unemployable individuals who reappl

- Page 72 and 73:

GR 41-100 NEEDS SPECIAL ASSISTANCE

- Page 74 and 75:

GR 41-101 - What is NSA GR 41-100 N

- Page 76 and 77:

committing suicide. • Danger to o

- Page 78 and 79:

Workers must exercise judgment to d

- Page 80 and 81:

evaluation. GR 41-104.3 - DMH/APS N

- Page 82 and 83:

the requirements, some eligibility

- Page 84 and 85:

Responsibilities Following are resp

- Page 86 and 87:

the GR DDD’s approval. See GR 41-

- Page 88 and 89:

the NSA remains ineligible, the PA

- Page 90 and 91:

• The advocate’s disagreement w

- Page 92 and 93:

GR 41-112.2 - Failure to Keep SSI A

- Page 94 and 95:

GR 41-200 Administratively Unemploy

- Page 96 and 97:

NOTE: GR participant reaches age 59

- Page 98 and 99:

GR 41-301 - Definitions GR 41-300 U

- Page 100 and 101:

#10 Wilshire Special 1818 S. Wester

- Page 102 and 103:

employability status is confirmed.

- Page 104 and 105:

• If the individual contacts the

- Page 106 and 107:

• The individual is to be referre

- Page 108 and 109:

GR 41-409.2 GR 41-409.3 GR 41-409.4

- Page 110 and 111:

GR 41-400 Employable GR 41-401 - De

- Page 112 and 113:

GR 41-403 - Part-Time Employment De

- Page 114 and 115:

appointment cannot be made prior to

- Page 116 and 117:

Refer to GR 41-412 for details on g

- Page 118 and 119:

Yes, the ABP 85 is validated but on

- Page 120 and 121:

should not disclose the fact that h

- Page 122 and 123:

the first sanction. If denied, the

- Page 124 and 125:

Unemployable During a Penalty GR 41

- Page 126 and 127:

Screening/Application GR 41-412.3 -

- Page 128 and 129:

GR 41-412.6 - Illness/Absenteeism I

- Page 130 and 131:

The requirement conflicted with emp

- Page 132 and 133:

Individuals who express interest in

- Page 134 and 135:

compliance issues outstanding. If s

- Page 136 and 137:

obtain employment or for their rema

- Page 138 and 139:

GR 41-416 - GROW Services GR 41-416

- Page 140 and 141:

Employment Needs Evaluation, determ

- Page 142 and 143:

GR 42-210 - Real Property Held to P

- Page 144 and 145:

GR 42-200 Property GR 42-201 - Defi

- Page 146 and 147:

The individual owned a vehicle valu

- Page 148 and 149:

the district to be filed in the Mis

- Page 150 and 151:

determining eligibility for GR. Ref

- Page 152 and 153:

Property Services referrals should

- Page 154 and 155:

• On the specified control date,

- Page 156 and 157:

• That immediate steps must be ta

- Page 158 and 159:

institution. GR 42-211.3 - Property

- Page 160 and 161:

• In family cases (two or more pe

- Page 162 and 163:

with Determined Value If the indivi

- Page 164 and 165:

• Retirement System Funds Funds i

- Page 166 and 167:

Examples include: • Retroactive S

- Page 168 and 169:

A participant receives a lump sum p

- Page 170 and 171:

eferral to Property Services for in

- Page 172 and 173:

GR 42-218.3 - Written Property Serv

- Page 174 and 175:

GR 42-408.2 GR 42-408.3 GR 42-408.4

- Page 176 and 177:

Sponsored Alien/Immigrant Sponsored

- Page 178 and 179: case record or information received

- Page 180 and 181: Amerasian Asylee Battered/Violence

- Page 182 and 183: GR 42-405.2 - Verification Verifica

- Page 184 and 185: • Post Office Box, Commercial Mai

- Page 186 and 187: GR 42-408 - Eligible Immigrant What

- Page 188 and 189: and have maintained residency in th

- Page 190 and 191: GR 42-408.10 - USCIS Referrals for

- Page 192 and 193: • If a non-resident is physically

- Page 194 and 195: 8) Discuss with the nonresident the

- Page 196 and 197: GR 43-109 - Required Action GR 43-1

- Page 198 and 199: For purposes of determining support

- Page 200 and 201: • There has been a court order re

- Page 202 and 203: GR 43-105.2 - Responsible Relative

- Page 204 and 205: GR 43-106.2 - Parental Liability NO

- Page 206 and 207: Responsible Relative NOT in the Hom

- Page 208 and 209: from the individual the date of the

- Page 210 and 211: GR 43-110.6 - Payment to DPSS Proce

- Page 212 and 213: GR 43-201 - Definitions GR 43-200 S

- Page 214 and 215: • I-134 The old Affidavit (I-134)

- Page 216 and 217: • Sponsors who receive public ass

- Page 218 and 219: • The sponsor receives public ass

- Page 220 and 221: collection without regard to whethe

- Page 222 and 223: GR 44-106.2 Certified School Employ

- Page 224 and 225: GR 44-118.3 Refuses to Sign the PA

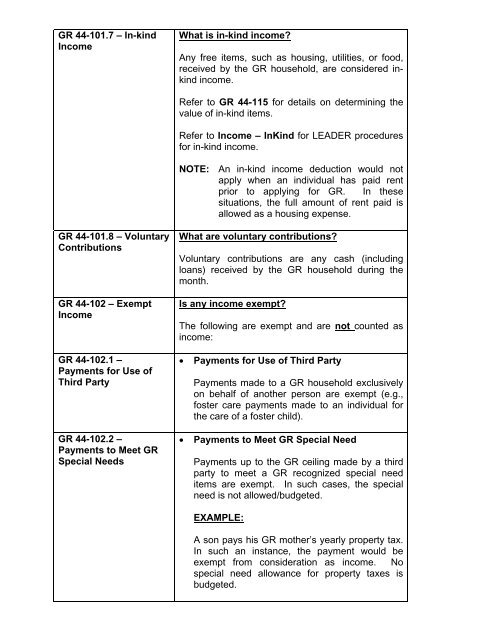

- Page 226 and 227: GR 44-100 Income GR 44-101 - Policy

- Page 230 and 231: ‣ Tools/equipment required by the

- Page 232 and 233: the food, housing, or personal care

- Page 234 and 235: Initiated - Create for LEADER instr

- Page 236 and 237: GR 44-103.1 - Quarterly Reporting C

- Page 238 and 239: A homeless person applies for GR on

- Page 240 and 241: • The “certificated” school e

- Page 242 and 243: GR 44-109.1 - Disability or Injury

- Page 244 and 245: ‣ The notification letter from th

- Page 246 and 247: terminating GR. GR 44-111.2 - Verif

- Page 248 and 249: months prior to the month of UIB ap

- Page 250 and 251: Mandarin 1-866-303-0706 Vietnamese

- Page 252 and 253: is denied or terminated. GR 44-112.

- Page 254 and 255: Yes, individuals who are referred f

- Page 256 and 257: GR 44-113.9 - Failure to Appeal a D

- Page 258 and 259: GR 44-114.5 - Verification of Earni

- Page 260 and 261: divided by the total number of pers

- Page 262 and 263: GR 44-116.2 - Verification Verifica

- Page 264 and 265: 379, the Worker manually denies/ter

- Page 266 and 267: numbers of authorized VOLAG offices

- Page 268 and 269: Individuals who meet the above crit

- Page 270 and 271: appeal, request continued benefits,

- Page 272 and 273: • In “REMARKS” (Section 5), e

- Page 274 and 275: individual fails to do so, the case

- Page 276 and 277: Retired pay for servicemen is arran

- Page 278 and 279:

individual will travel by bus, the

- Page 280 and 281:

• Actual cost of essential repair

- Page 282 and 283:

GR 44-201 - Basic Budget Table #68

- Page 284 and 285:

GR 44-219.1 GR 44-219.2 GR 44-219.3

- Page 286 and 287:

GR 44-229.17 Verification GR 44-230

- Page 288 and 289:

GR 44-201 -Basic Budget Table #68 G

- Page 290 and 291:

Issued only in very limited situati

- Page 292 and 293:

Refer to GR 44-205 for details on l

- Page 294 and 295:

‣ All of the related persons livi

- Page 296 and 297:

the following formula: a. Number in

- Page 298 and 299:

housing cost and utility payment co

- Page 300 and 301:

General Relief Money Management Cas

- Page 302 and 303:

living arrangements for their resid

- Page 304 and 305:

No, there is no hearing requirement

- Page 306 and 307:

approval and/or the GR grant to be

- Page 308 and 309:

GR 44-221.6 Contracted Rooms Are Fu

- Page 310 and 311:

Canceling Vouchers GR 44-221.16 Ful

- Page 312 and 313:

Table, the full $100 is issued for

- Page 314 and 315:

No, aid may not be issued to cover

- Page 316 and 317:

e made by the ES. All emergency aid

- Page 318 and 319:

4 8 8 8.80 5 10 10 11.00 6 12 12 13

- Page 320 and 321:

emergency payment to a disable pers

- Page 322 and 323:

enefit is the maximum amount of SSA

- Page 324 and 325:

immediately. GR 44-229.4 Kinds of E

- Page 326 and 327:

due, deadline for payment, signatur

- Page 328 and 329:

Emergency aid for housing may be is

- Page 330 and 331:

Food Stamps may be issued if the pe

- Page 332 and 333:

High Caloric High Protein moderate

- Page 334 and 335:

approved by the Division Chief. GR

- Page 336 and 337:

9 175.00 $5.83 10 $175.00 $5.86 NOT

- Page 338 and 339:

monthly pass, which is currently $5

- Page 340 and 341:

specified in the issuance criteria

- Page 342 and 343:

Yes, if GR is approved, $5.00 is de

- Page 344 and 345:

following basis: • The case is co

- Page 346 and 347:

Services Section must designate, in

- Page 348 and 349:

GR 44-301 - Benefit Issuance GR 44-

- Page 350 and 351:

GR 44-300 Aid Payments GR 44-301 -

- Page 352 and 353:

• The individual understands the

- Page 354 and 355:

NOTE: The data on LEADER and IDDS o

- Page 356 and 357:

GR 44-303.14 - Entire Benefits Can

- Page 358 and 359:

GR 44-304.3 - Verification What ver

- Page 360 and 361:

GR 44-304.11 - Individual Receives

- Page 362 and 363:

April bringing the account balance

- Page 364 and 365:

GR 44-308.5 - Changes in In-kind an

- Page 366 and 367:

For administrative overpayments:

- Page 368 and 369:

September 1, the individual receive

- Page 370 and 371:

the responsibilities and, knowingly

- Page 372 and 373:

Project, and • GR that is repaid

- Page 374 and 375:

GR 44-400 NOTICES OF ACTION AND HEA

- Page 376 and 377:

GR 44-400 Notices of Action and Hea

- Page 378 and 379:

number. The period of ineligibility

- Page 380 and 381:

Benefits must be issued on-line the

- Page 382 and 383:

GR 44-404 Individual’s Rights GR

- Page 384 and 385:

Hearing Officers may not be involve

- Page 386 and 387:

sanction is imposed when the good c

- Page 388 and 389:

terminate is reversed and aid is re

- Page 390 and 391:

GR 44-407.2 Hearing How is the hear

- Page 392 and 393:

Issue incorrect, or Regulation misa

- Page 394 and 395:

GR 44-411.4 When to Rescind Aid GR

- Page 396 and 397:

GR 45-112 - Lump Sum UIB/DIB - Remo

- Page 398 and 399:

• An ABP 320-3, Certification of

- Page 400 and 401:

difference between the B&C and R&B

- Page 402 and 403:

June 11 requires a GR application.

- Page 404 and 405:

• The ABP 32-3 must be obtained w

- Page 406 and 407:

If the individual is not eligible f

- Page 408 and 409:

the month. SOS/VPU makes necessary

- Page 410 and 411:

An individual receives UIB that cau

- Page 412 and 413:

The interview or home call should n

- Page 414 and 415:

An individual leaves the B&C facili

- Page 416 and 417:

• The prorated GR grant for the r